Collateral

In doing research on blended finance and especially Debt-for-Nature Swaps, one question has come up repeatedly.

In the event of bankruptcy - who ends up owning the collateral?

And this is a really, really important question, because those blended finance constructs are similar in creation to those CDOs crashing in 2008, taking out all mezzanine investments. Except, of course, this time with public finance (ie, taxpayer funds) on the mezzanine chopping board, should things (as intended) not work out.

I’ve covered Debt-for-Nature Swaps over several posts. Apparently, this particular one takes 28 minutes to read, per my Substack app! Apologies, but I do believe extraordinary claims demand extraordinary levels of evidence.

Regardless, on my travels I found a number of documents which all appear to - in one way or another - confirm my worst fears. And they also confirm the confidentiality agreements, the collaboration with finance ministers, and the explicit engagement of the United Nations itself. Here’s the first such document -

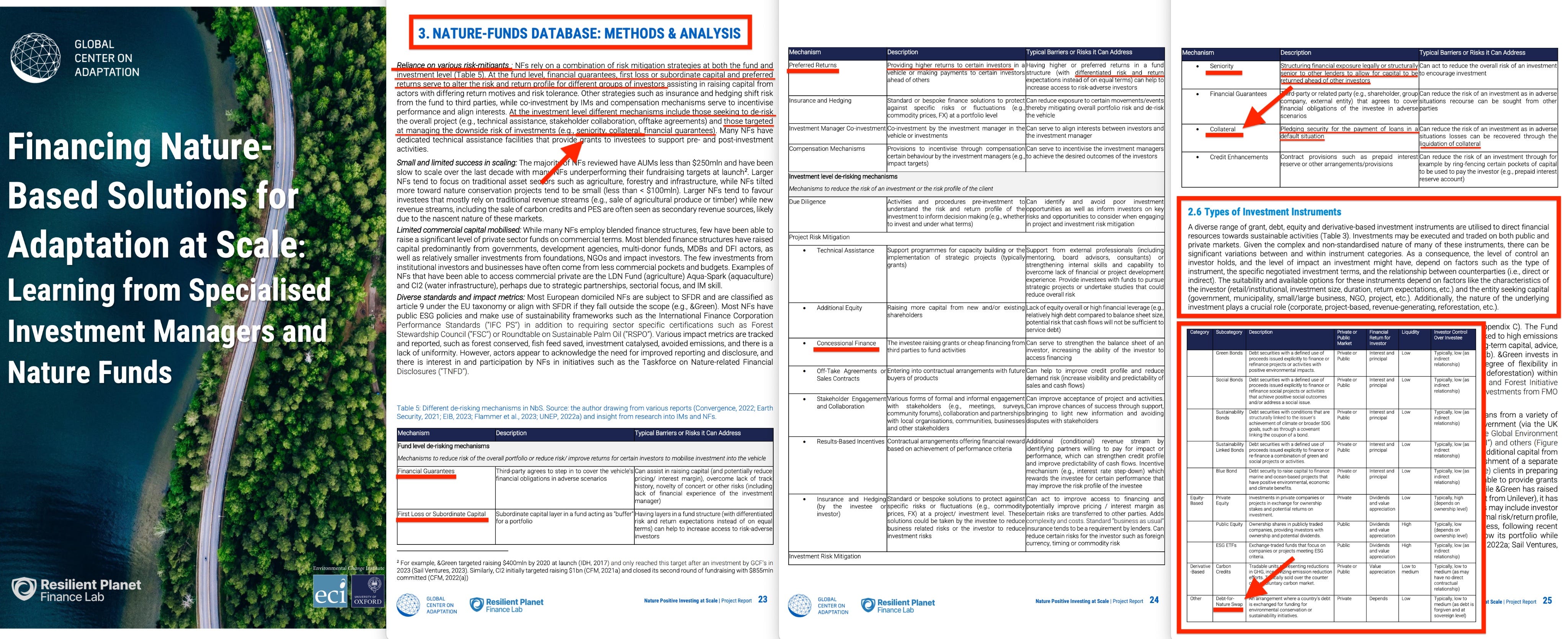

'Financing Nature Based Solutions for Adaptation at Scale'1, which outlines not just Debt-for-Nature type Swaps, but in fact a whole range of different types of investment instruments, along with the various options for de-risking these, one of which is express about collateral.

And just to get a few things out of the way - when third world nations agree to Debt-for-Nature swaps, the collateral in question will be those lands, pledged to the UNESCO Biosphere Reserves, and in the event of default (which eventually will happen), those lands will now be in the hands of... well, certainly not the host nations, or those 'indigenous peoples' they claim to care about.

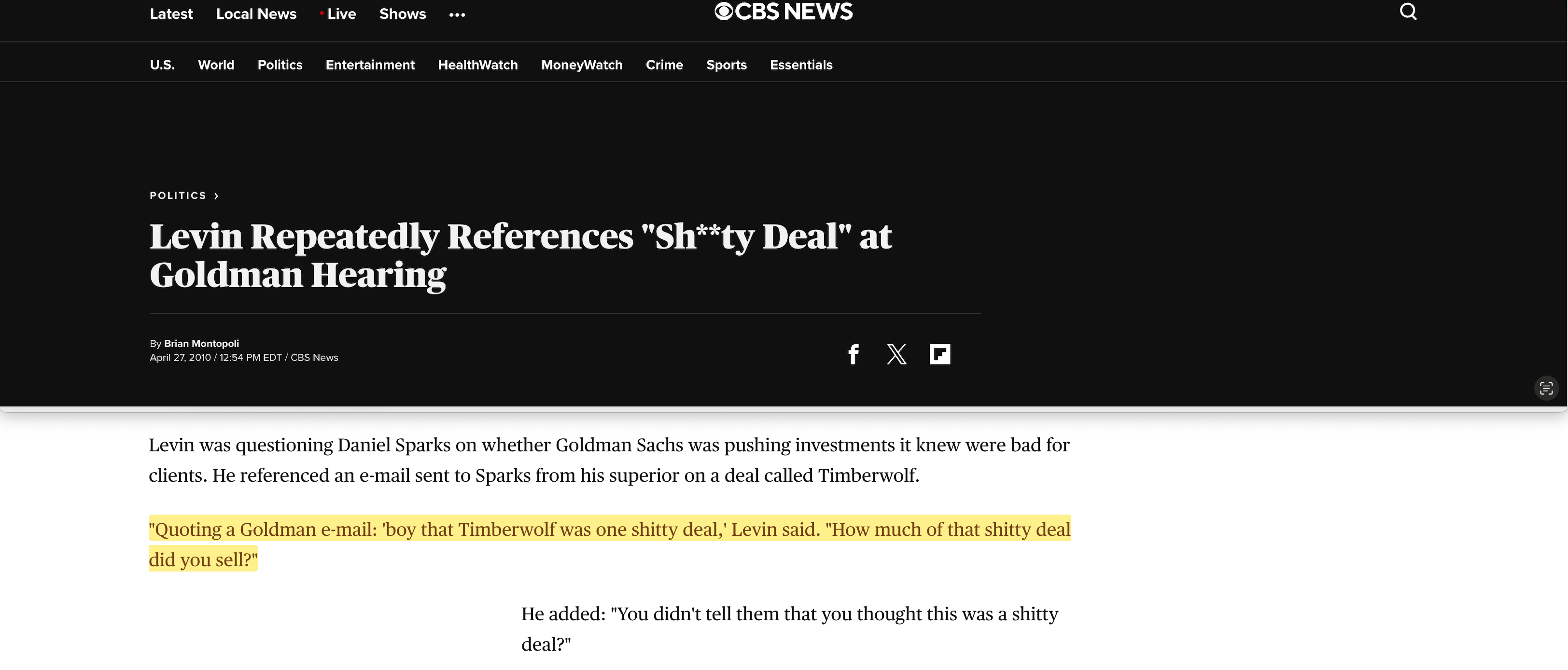

Incidentally, back in 2010, Goldman Sachs were in the firing line due to internal emails revealing what traders really thought of their ‘Timberwolf’ ‘investment opportunity’ as opposed to what the marketing material stated2. This is - kind of - the same thing, except this time, instead of taking out pension savings accounts, they are taking out 3rd world nations.

Having said all that, there’s a large emphasis on sovereign rights in general, so it is indeed possible - potentially even likely - that the collateral in question is not the land itself, but rather the exploitation rights, or leases thereof, which would technically circumvent the claim that associated lands being dispossessed, and hence there would - technically - be no loss of sovereign rights. This, however, would merely be a technicality, because what matters in this regard is the right of administration, including resource exploitation.

But, alas, impossible to state with certainty without access to project and financing agreements. But what this document does, is outline the possibility. Which, frankly, means that it almost certainly is the case, given this document being a compilation of learned lessons from professionals.

Regardless, it's a pretty good document, which also outlines a range of the other issues I highlighted in the past, including 3rd party financial guarantees (ie, public has to compensate for loss of interest payments), first loss (always on the public), preferred returns (always private), along with concessional capital (again, always public), where the latter relates to offering loans much cheaper than the going market rate, or even grants. A yet third way of putting it is ‘indirect subsidy’.

And to re-iterate, all this blended finance malarky is deliberately setup to almost exclusively benefit the minority private investor - while the majority public investor (who could easily go it alone), receives said 'Timberwolf' treatment outlined above. And Debt-for-Nature swaps will lead to the indebted nation losing rights over their own sovereign territory for almost certain.

Alternatively, the Global Environment Facility, the World Bank, and the various finance ministries can prove me wrong by releasing all project documentation in full - without redactions. But that won’t happen, and for obvious reasons.

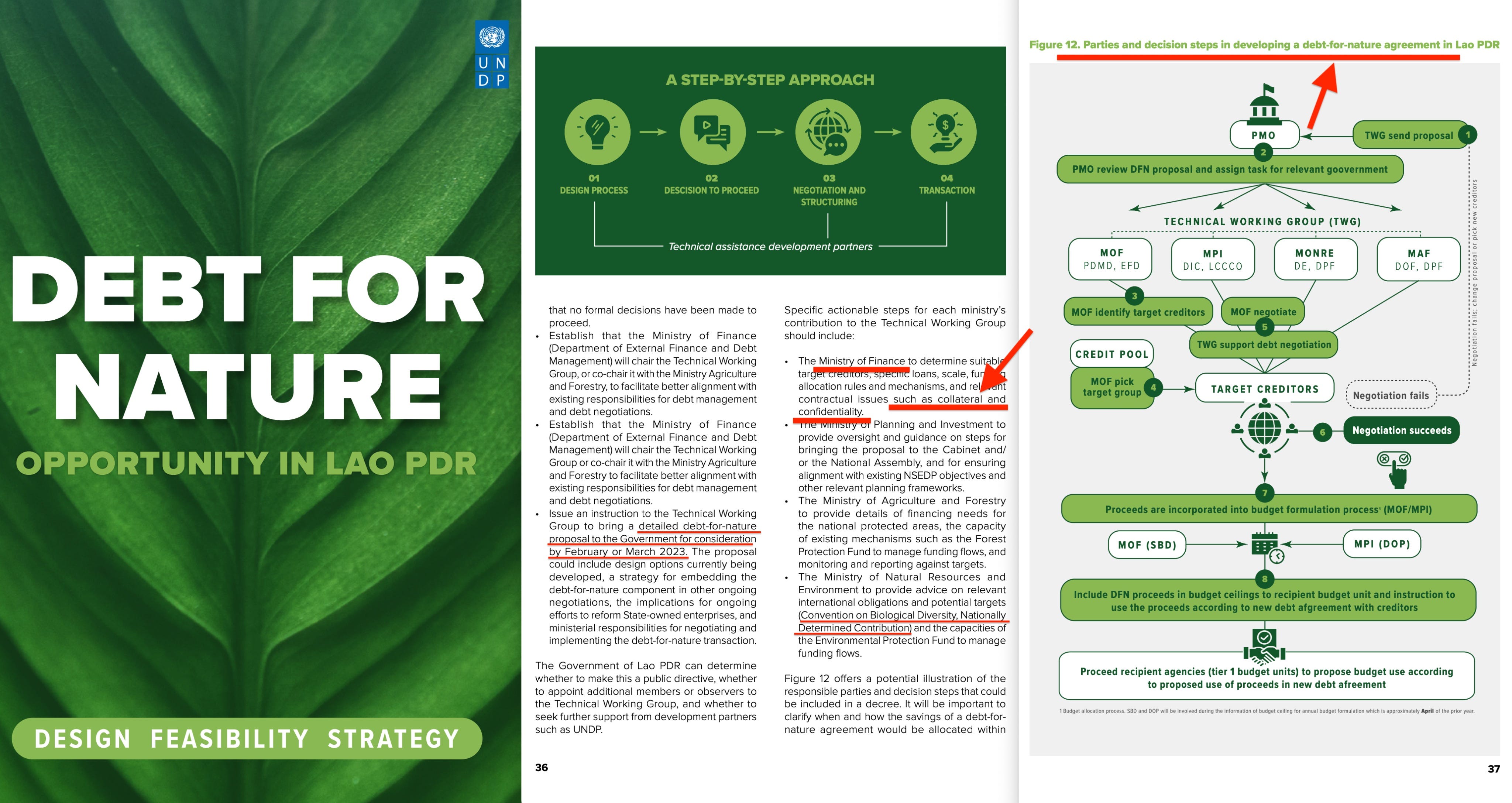

The next document comes courtesy of the United Nations Development Programme website, and it’s titled ‘Debt for Nature’3. It’s not the most exciting document, so let’s wrap that it quickly - 'The Ministry of Finance to determine ... relevant contractual issues such as collateral and confidentiality'

Yes, confidentiality. It’s a contractual issue. Ie - it won’t be released.

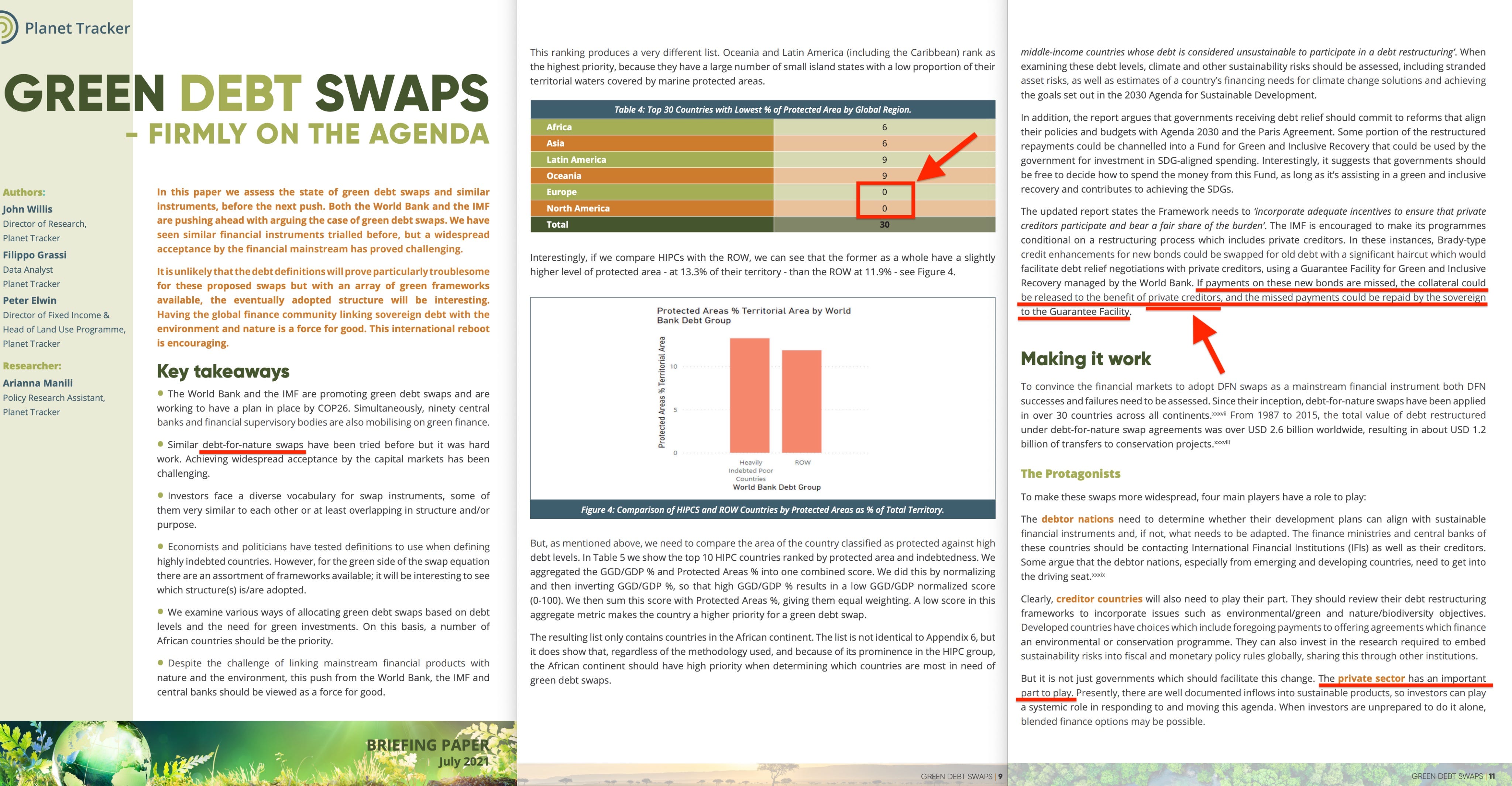

Next up is ‘Green Debt Swaps‘4, courtesy of ‘Planet Tracker’, and the key revelations in this document can be located on pages 9 and 11. Because on page 11, it outright states whom the collateral release will benefit - yes, the private investor -

'If payments on these new bonds are missed, the collateral could be released to the benefit of private creditors, and the missed payments could be repaid by the sovereign to the Guarantee Facility'.

But page 9 is further of interest, because Europe and North America are revealed to have set aside precisely no reserves for conservation. And that does, admittedly, look terrible from our perspective - but keep in mind that these are the same forces, currently attempting to destroy the West, financially, militarily, and by allowing anyone to walk across the border with complete impunity.

Rest assured these atrocities will not benefit anyone but the 0.001%, and their bought-and-paid-for politicians.

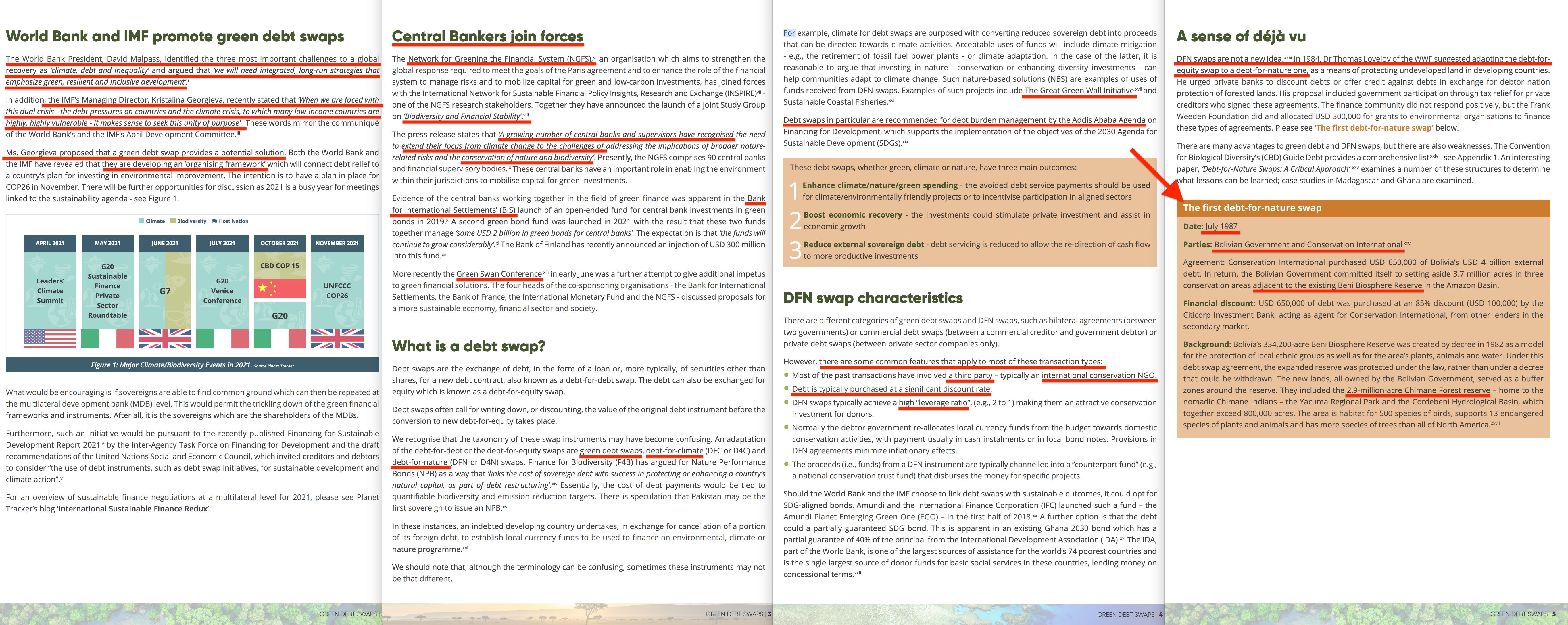

But there are more interesting parts to the document, and not just the strategic avoidance of discussion of the collateral itself. It drags in the central banks through the Network for Greening the Financial System (launched at the One Planet Summit in 2017), as well as the Bretton Woods institutions - the World Bank and the IMF. In other words, the entire banking system is ‘in’ on this, as well as a large part of the finance industry, and of course the United Nations.

Finally, it also refers to the first example of a Debt-for-Nature Swap, that of Bolivia and the Conservation International which we’ve repeatedly seen referred to (whilst ignoring the cases of Ecuador and Costa Rica, also finalised around the same time - for obvious reasons).

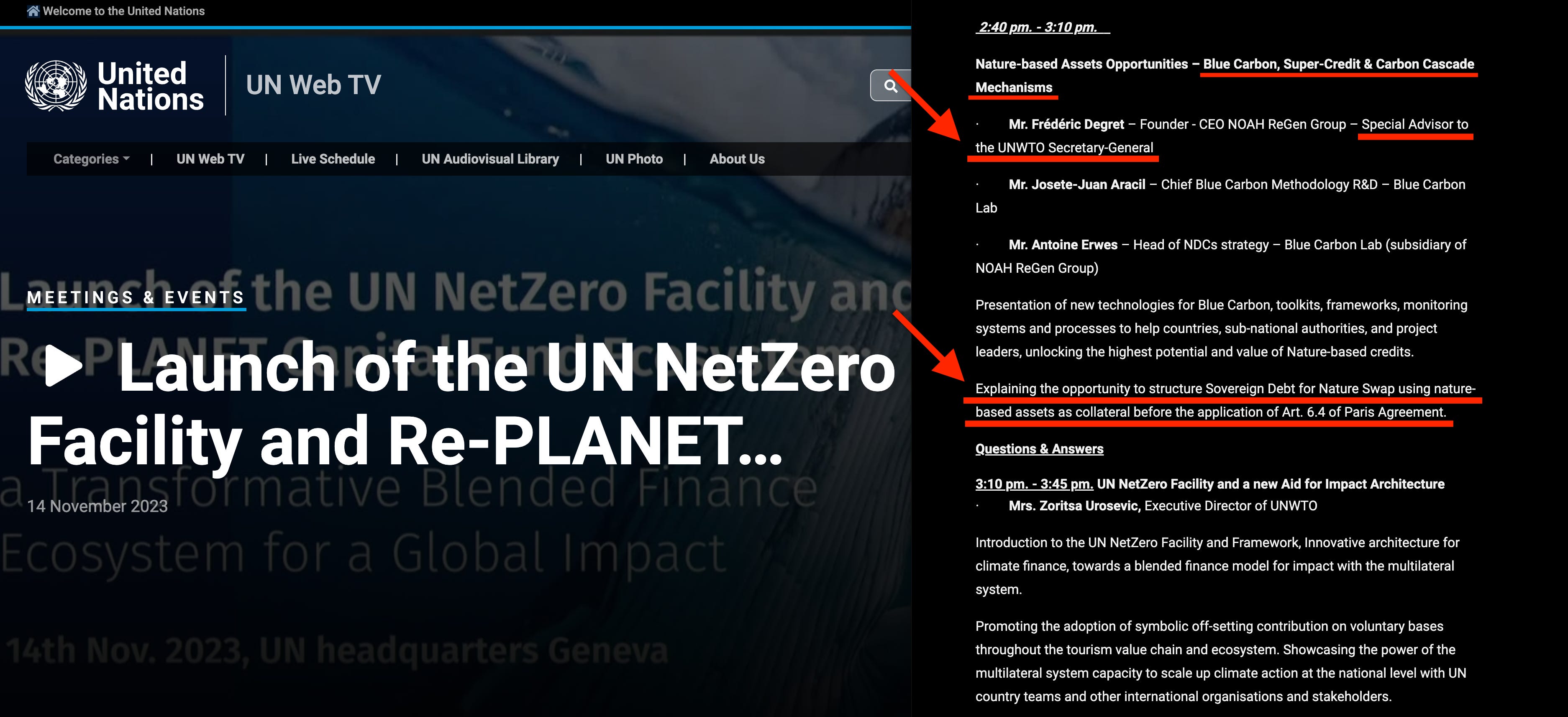

Next, let’s head over to the mothership itself, and the ‘Launch of the UN NetZero Facility and Re-PLANET‘5. During the 2:40-3:10 session, including some corporate CEO who apparently acts as an advisor to the World Trade Organisation in a manner, which I’m sure does not reflect any level of self-interest at all… or rather, goes to expressly outline the through and through corruption…

Not that this is unexpected, of course. The phrase of interest is this one -

‘Explaining the opportunity to structure Sovereign Debt for Nature Swap using nature-based assets as collateral before the application of Art. 6.4 of Paris Agreement.‘

In the event you don’t know what a ‘nature-based asset’ is, let me clear that up for you6. Yeah, it’s those forests, mangroves and so forth, which the Convention on Biological Diversity has determined we need to restore. Primarily for ‘Ecosystem Service’ monetisation purposes of the billionaire class, of course.

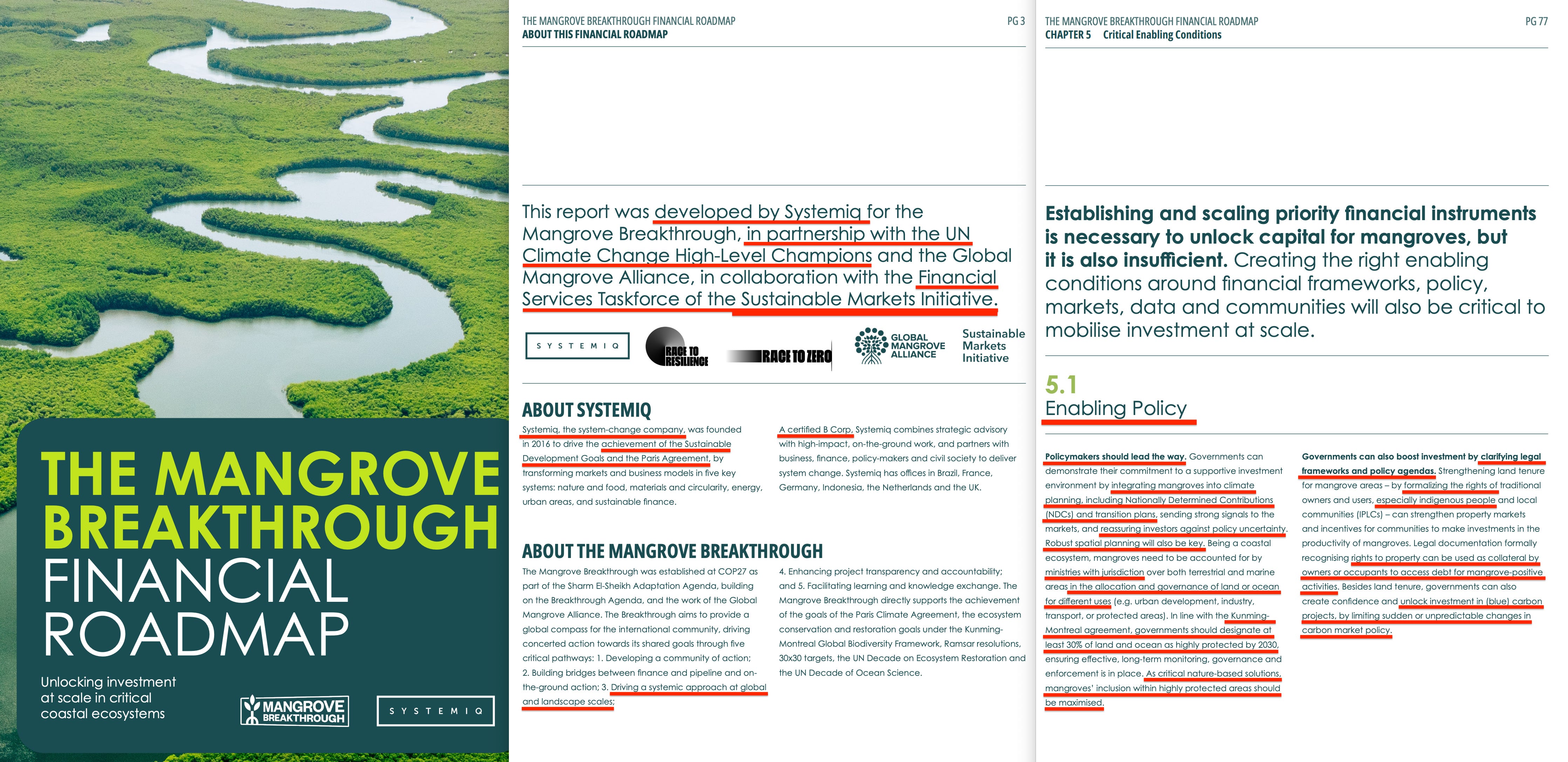

The fifth and final document will be ‘The Mangrove Breakthrough’7. And it’s penned by Systemiq, who ‘enable systems change’ - whether you like it or not. It’s furthermore sourced via the UNFCCC’s own website. It’s legit.

Let’s zip down to chapter 5.1; ‘Enabling Policy’ -

‘Policymakers should lead the way. Governments can demonstrate their commitment to a supportive investment environment by integrating mangroves into climate planning, including Nationally Determined Contributions (NDCs) and transition plans, sending strong signals to the markets, and reassuring investors against policy uncertainty‘

… quite frankly, the way this comes across…. this is only about making money, and ensuring a safe environment for those investors. Which, then again, is about making money.

‘Robust spatial planning will also be key. Being a coastal ecosystem, mangroves need to be accounted for by ministries with jurisdiction over both terrestrial and marine areas in the allocation and governance of land or ocean for different uses (e.g. urban development, industry, transport, or protected areas). In line with the Kunming- Montreal agreement, governments should designate at least 30% of land and ocean as highly protected by 2030, ensuring effective, long-term monitoring, governance and enforcement is in place. As critical nature-based solutions, mangroves’ inclusion within highly protected areas should be maximised.‘

I stand corrected. It’s also about changing policy to accomodate those goals, especially in terms of those super-monetisable carbon sinks; mangroves. Oh wait. That’s still just about making money.

‘Governments can also boost investment by clarifying legal frameworks and policy agendas. Strengthening land tenure for mangrove areas – by formalizing the rights of traditional owners and users, especially indigenous people and local communities (IPLCs) – can strengthen property markets and incentives for communities to make investments in the productivity of mangroves‘

Through single-handed, non-verbal gestures, they emphatically explain that those ‘indigenous peoples’ they care about deeply are given their rights… only to reveal why they carry that dagger in their other hand -

‘Legal documentation formally recognising rights to property can be used as collateral by owners or occupants to access debt for mangrove-positive activities. Besides land tenure, governments can also create confidence and unlock investment in (blue) carbon projects, by limiting sudden or unpredictable changes in carbon market policy.‘

… and that’s where the knife goes in. Yeah, said ‘indigenous peoples’ should definitely pledge those lands as collateral in exchange for usurious debt-for-nature swaps, which are designed never be to be repaid, ultimately leading to those deeds being transferred, after many fruitless - and (intentionally) progressively worse - attempts to refinance.

And that’s how they plan to reach 30% by 2030. Through outright exploitation. But it also shines a light on Systemiq, and what purpose they have in the greatest, currently ongoing scam of all time.