47%

In late 2021, the V-20 released the ‘V20 Statement on Debt Restructuring Option for Climate-Vulnerable Nations‘1.

I’m not sure who told them this would be in their interest. Because it really isn’t.

It’s the same old story. Third world nation is struggling under colossal loads of debt. It’s a matter of when - not if - they will go bankrupt. Naturally, we can’t have that, because think of the poor, starving ‘indigenous peoples’, who live on lands which can be monetised for timber and carbon credits ecosystem services.

Regardless, as debt loads increase, so does likelihood of default. To compensate, a higher risk premium is added - ie, a higher interest rate. There is absolutely nothing new about this dynamic, and this should serve as a very general and basic rule, leading to responsible fiscal policies in the first place.

Except, of course, in a world of make-believe climate change, which tends to impact primarily those third-world nations struggling to pay (but incidentally also generally have much higher levels of population growth), these are suddenly caught under said debt levels not for classic reasons, but because of alleged climate change which - assuming said is true, which it is not - they a) couldn’t possible have predicted 3 decades ago when the Earth Summit in Rio took place, and b) their high population growth rates have absolutely nothing to do with, no, rather it’s those darn western nations, polluting mah biosphere (and never mind China).

It’s the same old script, rehashed yet again. And never mind them richly detailing Covid-19 and its impact on debt which could never, ever have taken place, had it not been for fully complicit central banks. And also not forgetting that said nations largely didn’t care about the scamdemic, in fact saw very low levels of vaccination uptake, yet the argument is then further pushed, as debt servicing now tracks higher than healthcare spending.

Now, golly whiz, I don’t recall large death counts in said nations in spite of low uptake of Pfizer magic juice, but then I haven’t received fat stacks for voicing that opinion either. Regardless, what I say is that already at this stage, they appear to smear it on a bit thick. Yet, it continues -

‘Many V20 countries have insufficient fiscal resources to finance much-needed responses to the health and social crises caused by the pandemic, as well as crucial investments in climate adaptation‘

Yeah, we all need money, and debt foregiveness, flexibility, and…. swaps.

Sure, these are ‘Debt-for-Climate’ swaps, but it’s the same thing, ultimately. Regardless, a ‘major debt restructuring initiative for countries overburdened by debt is needed‘.

I have a number of reasons to object already, but let them finish the thought -

‘We suggest a concerted effort by multilateral agencies such as the World Bank Group and regional multilateral development banks to act as guarantors of restructured debt through guarantee facilities for inclusive, sustainable, and resilient recovery efforts. An example of such a proposal includes the Guarantee Facility for Green and Inclusive Recovery managed by the World Bank‘

MDBs, the World Bank Group, guarantee facilities…….. now I have even more reasons to object. But let’s give them a bit more rope -

‘The debt restructuring framework needs to incorporate adequate incentives to ensure private creditors participate and bear a fair share of the burden‘

These are debts, typically trading at deep discounts. These are debts, which could be weeks, days from defaulting. Yet, somehow - somehow - the private investor needs to be dragged to the table, to ‘accept a fair share of the burden’?

Also, buy my Brooklyn Bridge.

‘If a country is found to have unsustainable public debt, it should be eligible for debt relief involving both public and private creditors, with equal treatment of public and private creditors. The debt restructuring framework needs to incorporate adequate incentives to ensure that private creditors participate and bear a fair share of the burden.‘

Right, so the private investor needs to be treated the same as the public investor, yet should also receive ‘adequate incentives’??? Horse manure, quite frankly.

‘Those countries needing relief would be supported by multilateral agencies through guarantee facilities that would facilitate debt relief negotiations with private creditors‘

More on that in a minute.

‘… a guarantee facility could provide credit enhancements for new bonds that would be swapped for old debt with a significant haircut. A guarantee facility could ensure that commercial actors (whether bondholders or commercial banks) will receive up to 18 months’ worth of interest payments in the case that the sovereign misses a payment, and provide a guarantee of the value of the new bonds‘

And who do you think will pay for said ‘guarantees’? Yes, the World Bank, sure, but whose money do they spend? Why, ours, of course. That of the Western taxpayer.

‘Moreover, the financial authorities of the jurisdictions in which the major private creditors reside should use strong moral suasion…‘

Oh right, a strongly worded letter in other words, ie, do literally nothing, because would they, Goldman Sachs wouldn’t ever hire them, and a regulator with integrity… clearly doesn’t exist.

The rest of the document is somewhat predictable, let’s race through it -

‘Natural climate solutions – the protection and enhancement of forests, mangroves and coral reefs – should be a central aspect of adaptation and resilience planning‘

In other words - areas suitable for carbon credit monetisation.

‘This would support governments in regaining access to international capital markets and help address their deep-rooted reluctance to restructure unsustainable debt out of fear that a debt restructuring – and the concomitant declaration of a technical default by the rating agencies – would reduce their access to capital markets for extended periods of time.‘

Sure, if a nation declares bankruptcy, they’ll lose access to capital markets until their economies are worth investing in, again. But what sort of ‘access’ is a 25% interest rate, when global average is… 3%?

‘Evidence and ample precedent suggest that a restructuring would improve sovereigns’ balance sheets and medium term creditworthiness, and therefore allow them to access capital markets in better conditions. In any case, a credit enhancement would facilitate the issuance of new debt‘

The key word here is ‘medium-term’. Because short-term is… problematic, regardless. And long term likely is… much, much worse. At least if they go through with said Debt-For-Whatever swap restructuring.

There are a few points the declaration does not touch upon, one of which is collateral. Exactly what is pledged as collateral, doing said Debt-for-Whatever swaps? Because there will be collateral demand, especially when dealing with nations not exactly known for fiscal prudence.

The collateral will likely be the carbon credit generating lands identified above, submitted to the UNESCO Biosphere Reserves, from where the billionaire class will monetise them through odious GEF blended finance deals, only to stick these leases into holding companies, floated on stock markets in the form of ‘Natural Asset Companies’, from where they will ensure carbon offsetting becomes far more expensive, and thus your energy and food prices skyrocket through cost-push inflation.

And it will happen; they’ve spent decades pushing this plan through in slow motion, hoping you wouldn’t notice. A temporary setback on those Natural Asset Companies will not deter, they’ll just wait for the next disaster sure to distract. Or if one doesn’t come soon enough, hey, perhaps they’ll (partially) crash the stock markets, threatening to wipe out your retirement account.

In 2022, another article hit the web, titled ‘A green strategy to defuse the “debt bomb”‘2. As I’m sure you can work out, it’s… more of the same. So why include it, you may ask. For a number of reasons, the first being this -

‘Since the start of the pandemic, financial support provided by the IMF and multilateral development banks has provided a lifeline to many governments in the Global South. However, those large portions of these public transfers have been used by debtor governments to pay debt service to external private creditors‘

See, whatever we do here in the west - it’s NEVER enough. You could donate the left shoe of your grandmother, and they’d be right back, demanding the right. Regardless of what you’re ready to sacrifice, IT WILL NEVER, EVER END.

Much like the message out of that iconic 80’s movie… the only winning move is not to play. To tell them to F- RIGHT OFF, quite frankly. When is enough enough? When you’re not allowed to heat your home in the winter? When you’re not allowed to walk outside for more than 20 minutes per day? When your kids are forced to eat insect protein, while indoctrinated with values in school at odds with reality?

‘The measures taken by the international community to date have not sufficiently addressed the worsening debt sustainability problem‘

It’s never enough. Never, never, ever enough.

‘The G20’s Debt Service Suspension Initiative (DSSI), which ended in December 2021, provided a mere USD 13 billion in temporary relief to 48 low-income countries through a suspension of debt-service payments owed to their official bilateral creditors. Private creditors, who hold the biggest share of developing country debt, did not participate at all.‘

… oh really? That’s very interesting. More on that in a minute.

‘To bring private creditors to the negotiation table, a carrots-and-sticks-approach is needed, that is, a combination of positive incentives (“carrots”) and pressure (“sticks”).’

All that should be required is said nations threatening with default. Because if they declare so, said private creditors will lose every penny.

’With colleagues, I have put forward a proposal for debt relief for a green and inclusive recovery. In terms of incentives, we propose the creation of a new Facility for Green and Inclusive Recovery administered by the World Bank that is designed to entice the commercial sector to engage in debt restructurings.‘

First off, if you trust the World Bank, then I suggest you read up on the World Bank, because you clearly don’t know them. Second, the World Bank - as outlined above - spend our taxes, through our governments. Consequently, you will pay.

‘The Facility, which could be established relatively quickly, would back the payments of newly issued sovereign bonds that would be swapped with a significant haircut for old and unsustainable, privately held debt‘

… that might well be, but that’s not the full story here. Because said debts will be sold back to the indebted government at a higher price, often in fact near 100% face value, meaning there won’t be a loss involved from the perspective of the private investor, whatsoever. Or the loss will be, say, 5%, rather than the 75% priced in by the market.

That’s how those Debt-for-Whatever swaps work. A middle-man - Conservation International, for instance - will make a tidy profit, however. And who will swallow those loss? Well, that’s typically the job of the MDB, and thus in turn, you - through your taxes.

‘In terms of pressure, the financial authorities of the jurisdictions in which the major private creditors (both banks and asset managers) reside and that govern the majority of sovereign debt contracts – most importantly the United States, the United Kingdom, and China – could use strong moral suasion…‘

They even use the exact same phrasing. That’s no coincidence.

‘Debt relief should not only provide temporary breathing space‘

But that’s exactly what they’re designed to do. Because down the line, the ‘medium term’ fix will - per design - threaten to derail once again, necessitating an even worse refinancing ‘deal’, … which eventually will send those pristine mangroves or forests to the UNESCO Biosphere Reserves for good.

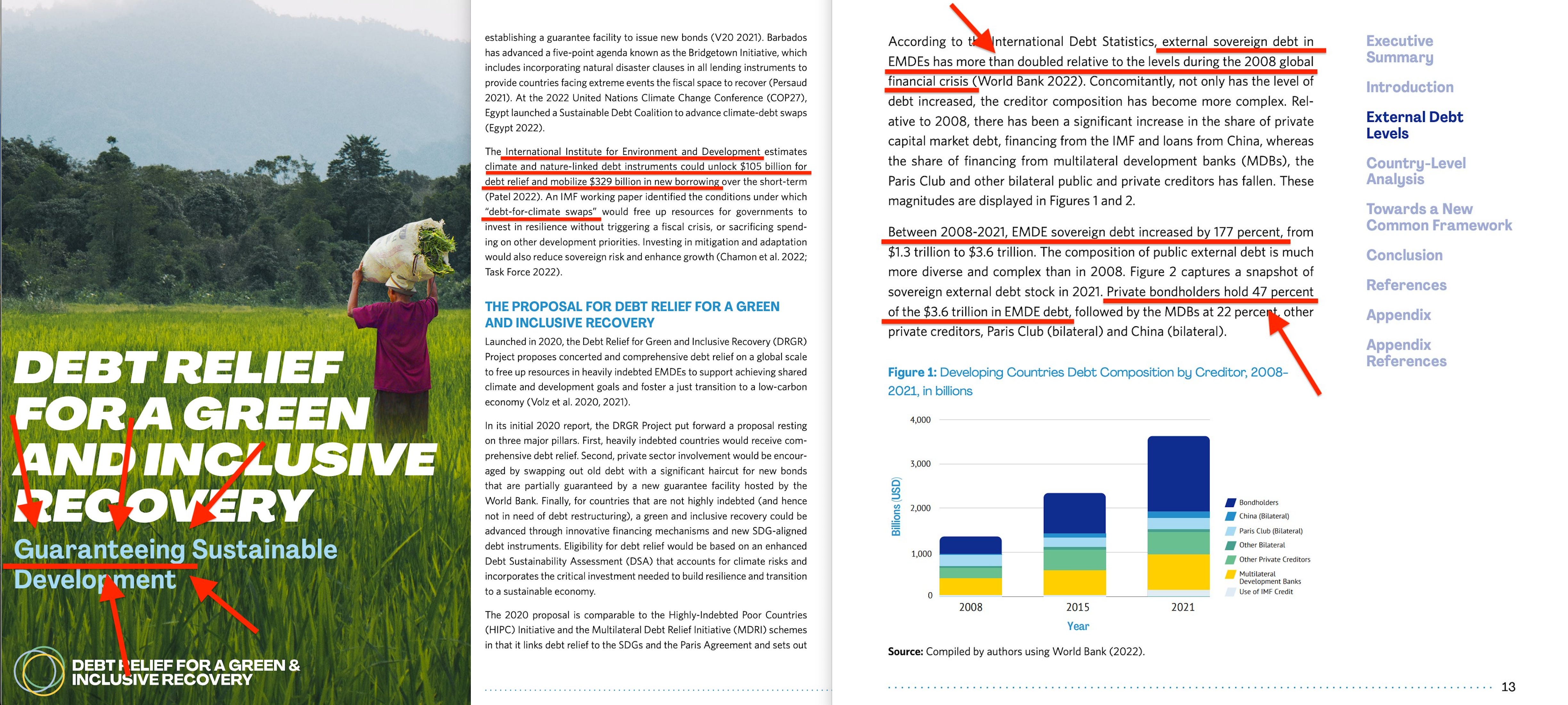

So with that in mind, let’s pop over to the next document, titled ‘Debt Relief for a Green and Inclusive Recovery - Guaranteeing Sustainable Development‘3. Because this includes further, somewhat damning detail. On page 9 we find -

‘The International Institute for Environment and Development estimates climate and nature-linked debt instruments could unlock $105 billion for debt relief and mobilize $329 billion in new borrowing over the short-term (Patel 2022).’

The IIED - of course - is Barbara Ward’s, known not only for ‘Spaceship Earth’, but also for speaking of ‘Sustainable Development’ before it was titled such.

And $105bn? $329bn? Really? That’s amazing.

’An IMF working paper identified the conditions under which “debt-for-climate swaps” would free up resources for governments to invest in resilience without triggering a fiscal crisis, or sacrificing spending on other development priorities‘

I can tell you right now that this is 100% concentrated horse manure, through and through. Why? Because why do said debts need restructuring? Because of existing excessive debts.

But it gets worse. Page 10 reveals -

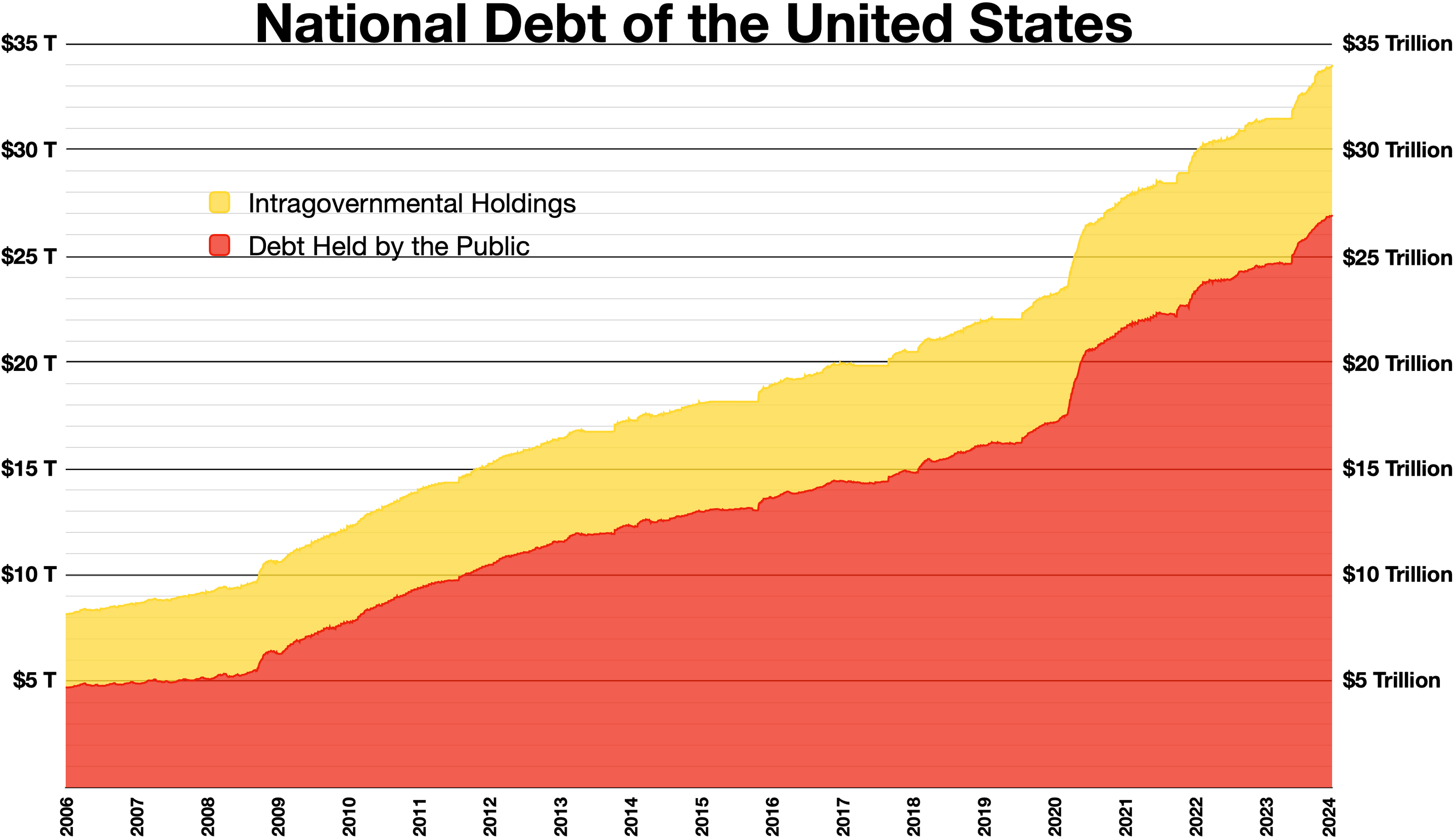

‘To preview main findings, we find that external debt levels and service payments have more than doubled since the 2008 global financial crisis, with climate vulnerable nations among the most exposed. External public and publicly guaranteed (PPG) debt has jumped from $1.3 trillion in 2008, to $3.6 trillion in 2021.‘

So debt levels have - roughly - tripled in 13 years, in spite of ‘expect’ advice courtesy of the likes of the International Monetary Fund and the World Bank. They’re either incompetent, or lying about their purpose.

We continue on page 13 -

‘According to the International Debt Statistics, external sovereign debt in EMDEs has more than doubled relative to the levels during the 2008 global financial crisis (World Bank 2022).‘

Yeah, almost tripled, but -

‘Between 2008-2021, EMDE sovereign debt increased by 177 percent, from $1.3 trillion to $3.6 trillion. The composition of public external debt is much more diverse and complex than in 2008. Figure 2 captures a snapshot of sovereign external debt stock in 2021. Private bondholders hold 47 percent of the $3.6 trillion in EMDE debt, followed by the MDBs at 22 percent, other private creditors, Paris Club (bilateral) and China (bilateral).‘

…. aaaaaaaaaaaaand CUT!

The private bondholders own 47% of $3.6tn of (very likely) underperforming debt - $1.7tn!!!

Should we accept an across-the-board 30% haircut, that amount to just short of $510bn of losses for the private investor, of which a large part will be held by the commercial banks - just as they did back in 1982, when we saw the exact same scenatio unfold as Mexico failed to refinance, triggering the debt crisis.

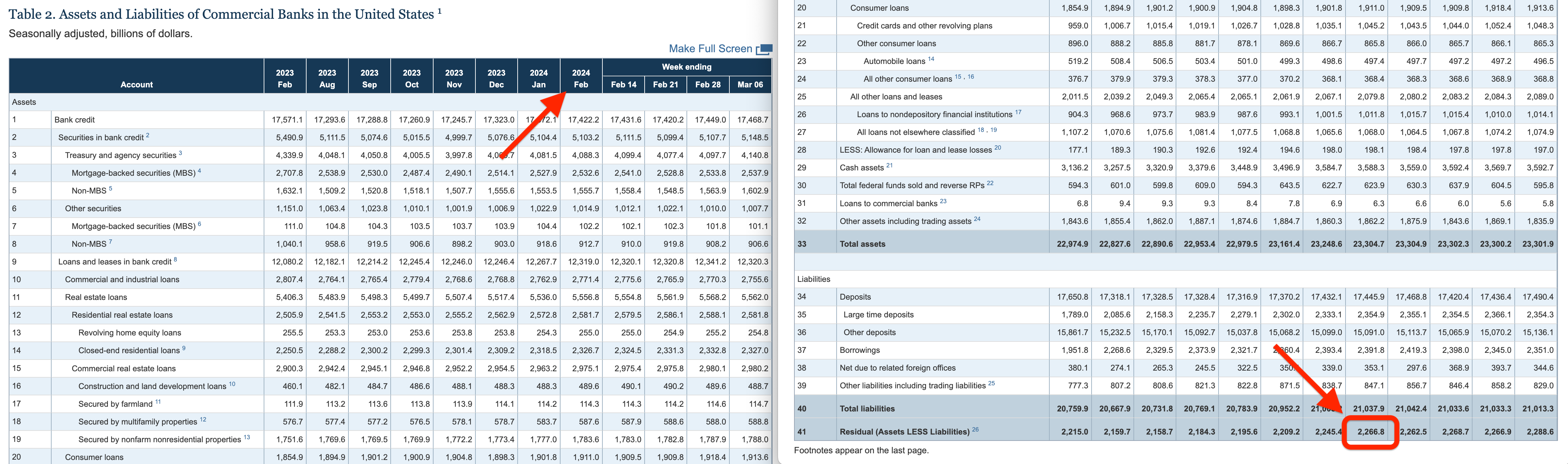

Back then, a 30% haircut would have led to $150bn of losses, which would pretty much have entirely wiped out Wall Street… but how bad is it this time around? Well, to find out, let’s head over to the Federal Reserve4.

Well, as of February, 2024, in a market which has defied… gravity… for years, with completely made-up job reports released by the most corrupt American Administration in recorded history, $500bn amounts to 22.5% of equity.

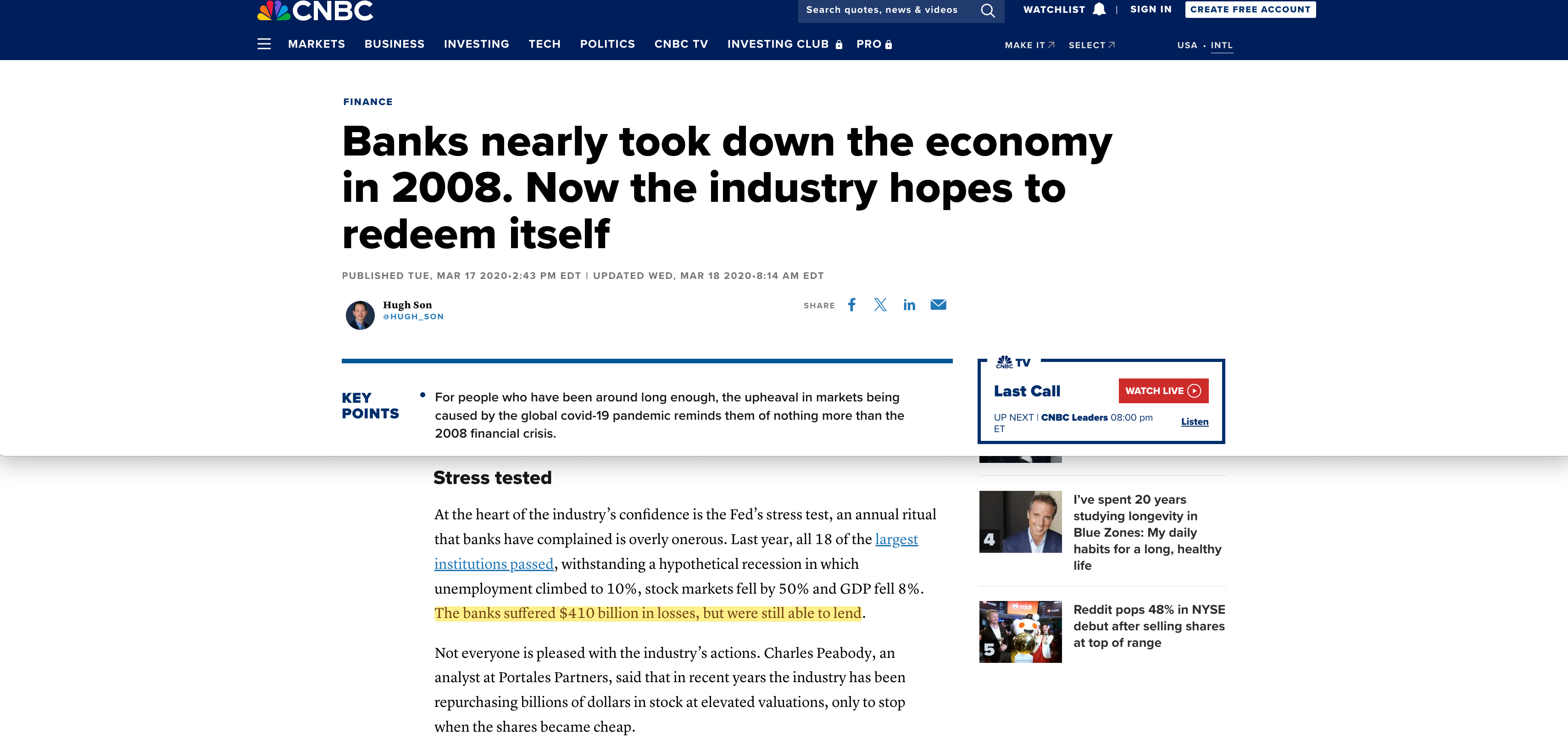

Sure, sure, they can stomach that, you say. Oh btw, the equivalent number for 2008 you ask5? $1.2tn at the time of Lehman collapse. And bank losses? $410bn6.

However, the only reason why 2008 didn’t lead to a total crash, was because the world’s central banks started printing, in fact, and never stopped7.

But we’re veering somewhat off the original purpose here. The point I make is that restructuring said debts won’t benefit those indebted nations one bit, long-term. What they should do - much like Greece should have done back in 2012 rather than refinance - is declare bankruptcy, because it’ll happen regardless.

But if they do it voluntarily, the big banks won’t be given the chance to steal every pristine carbon credit sink through forests and mangroves. And while there will be times of hardship, postponing it will only make it worse.

Because after all - in spite of the ‘best available economic advice’ courtesy of the World Bank and the IMF… the debt burden has nearly tripled since 2008.

What makes you think this time is different?