A General Theory

Pull out just about any economic textbook, and it will tell you that Keynes’s General Theory (1936) was revolutionary—that the integration of countercyclical fiscal and monetary policies to smooth out boom and bust cycles was unique.

But… reality is that it wasn’t. In fact, it was a natural extension of discussions held by the Royal Institute of International Affairs in 1931, 1933, and 1935.

And this not only challenges the conventional narrative of economic history, but it also forces us to question how modern monetary policies—and the power these vest with central banks—have been quietly engineered over decades.

This is a continuation of not only The Origin of Global Governance, but further Crisis Economics, published in January, 2025. And it’s been a somewhat crazy journey, because when I originally penned the latter, I did not expect to find evidence, strongly suggesting that my interpretation was correct.

But that belief was partially shattered when covering Dumbarton Oaks. Because during this investigation, I located three reports which challenged the established narrative. These reports were The International Currency Experience, Economic Stability in a Post-War World, and The Trade of Nations. And let’s do a quick recap.

The International Currency Experience (1944) considers the interwar period, analysing how currencies were both stabilised and destabilised during the 1920s and 1930s, pinpointing the failures of the gold exchange standard as central to these fluctuations, while highlighting that effective central bank cooperation was essential to avoid competitive deflation and monetary crises. Its findings not only influenced the development of the Bretton Woods system—promoting international coordination of monetary policies as a requirement of currency stability—but also cemented the pivotal role of the Bank for International Settlements in managing global monetary policy.

Economic Stability in a Post-War World (1945) and The Trade of Nations (1946) further built on this, by promoting Keynesian countercyclical fiscal policy and trade liberalisation as cornerstones of post-war economic recovery. The former report argues that government intervention through deficit-financed public investment and managed monetary policy was crucial for smoothing economic cycles, preventing depressions, and maintaining full employment, while also advocating for harmonised international policies.

The Trade of Nations positioned free trade—reduced tariffs, free movement, and integrated global markets—as essential not only for fostering peace and economic prosperity but also as a complement to domestic fiscal management.

In other words—the three reports advocated free trade policies (in full alignment with Leonard S Woolf’s International Government), and central bank policy harmonisation through the Bank for International Settlements.

Through the post on Black Tuesday, we saw how the Bank for International Settlements became, essentially, everything central bankers desired, with its original objective—handling German reparations—reduced to a distant afterthought. We also saw how this entire structure hinged on gold as a universally accepted asset, facilitating the BIS’s creation. Then, through Bretton Woods, the BIS’s mandate was refined, ultimately aligning with the structure Julius Wolf outlined in his 1892 book—a cooperative model built around public labor and private capital.

But that still leaves a gap in the interwar period, spanning from the establishment of the Bank for International Settlements in 1930 to Keynes’s publication of The General Theory in 1936. As it turns out, three reports specifically address this period. Before diving into them, let’s first outline what made The General Theory so unique.

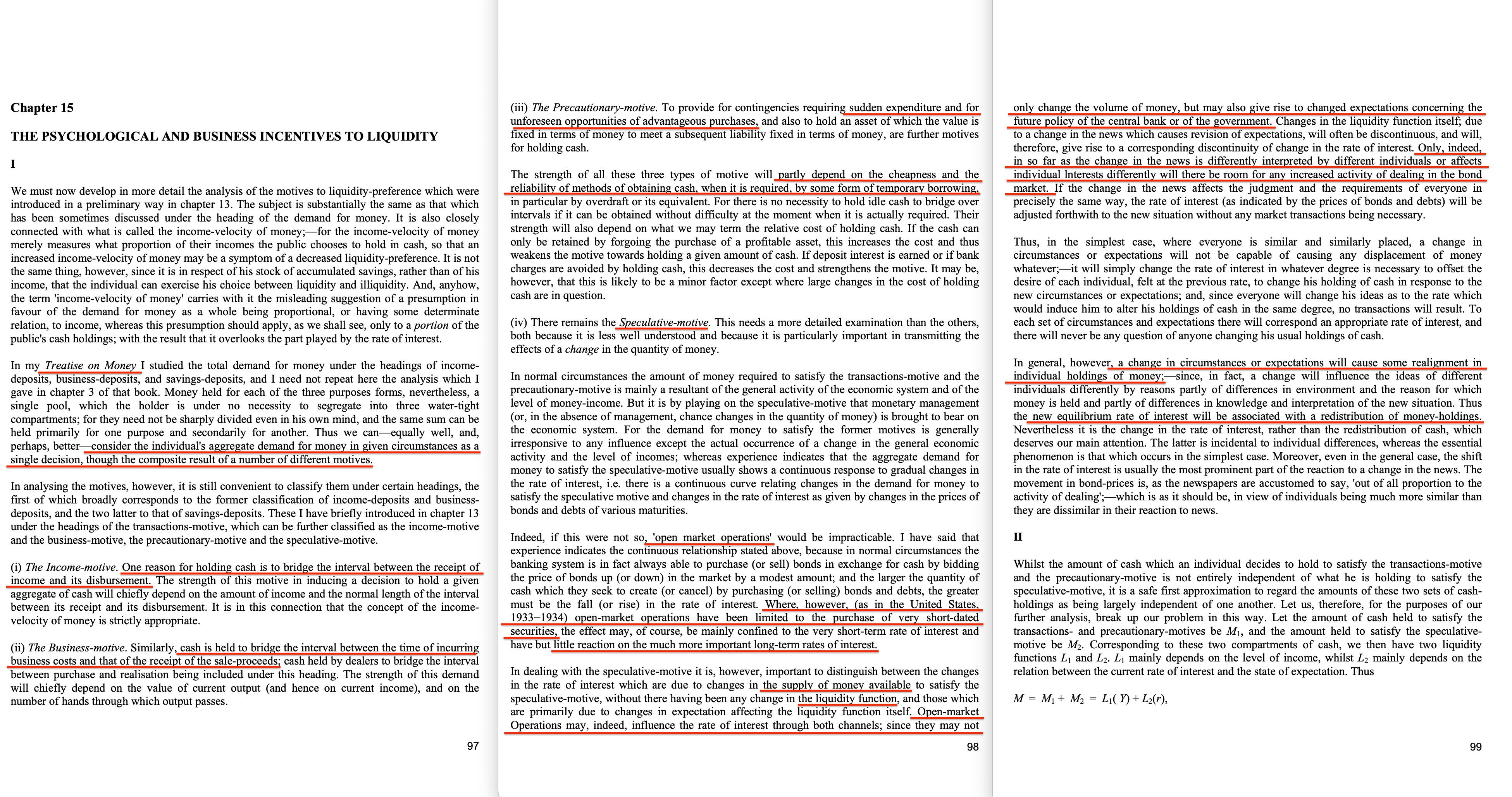

In his General Theory, Keynes argued that the gold standard was holding economies back because it tied the amount of money in circulation to gold reserves. This restricted governments and central banks from responding effectively to economic downturns. Once the gold standard was removed, it became easier for central banks to manage the economy, using tools like open market operations (buying and selling government bonds to influence money supply), which later evolved into Quantitative Easing (QE).

He believed that during recessions, cutting interest rates could make borrowing cheaper and encourage businesses to invest. However, he warned that this alone might not be enough—in a liquidity trap, even when rates are near zero, businesses and consumers may still not borrow or spend due to uncertainty. When this happens, further rate cuts won’t solve the problem. Instead, Keynes argued that governments must step in and spend directly—on infrastructure, public works, or social programs—to create jobs and stimulate demand.

One of his key ideas was the Paradox of Thrift: If people panic during a recession and start saving too much, demand collapses, causing the economy to shrink further. He also rejected classical economists' belief that markets always fix themselves. He pointed out that wages don’t fall easily, businesses hesitate to invest due to fear of the unknown, and that if everyone cuts back at the same time, the entire economy suffers.

Keynes’s ideas transformed how governments approach recessions. Rather than waiting for the economy to fix itself, modern governments and central banks now actively intervene, using stimulus programs like the New Deal, the 2008 financial crisis bailouts, and COVID-era spending to keep businesses open, protect jobs, and boost demand.

As a result, The General Theory is fundamentally an argument for top-down economic management, where both monetary and fiscal policy are used to stabilize aggregate demand and achieve full employment. Keynes’s framework directly rejects the classical view that markets are self-correcting, instead asserting that government and central bank intervention is necessary to prevent economic downturns.

Today, the 2023 Fabian Society pamphlet In Tandem builds on this logic but takes it further. It proposes that the Bank of England should have influence over fiscal policy, arguing that during a liquidity trap, government spending must be more carefully controlled. While this aligns with Keynes’s view that governments must act in crises, it also shifts power away from elected politicians and toward unelected central bankers. This would give financial institutions greater control over public spending, raising concerns about who ultimately makes economic decisions in a democracy.

Keynes, in essence, argues that all economic activity is relative to a potential maximum, and that through the management of monetary and fiscal policy, the flow of money can be stabilized within the human super-organism—much like blood flows through the veins of an individual.

Monetary policy should thus support fiscal policy during crises, which in turn helps stabilise and maximise aggregate output and consequently—employment. And monetary policy operates through the manipulation of interest rates and open market operations to regulate liquidity and investment, later evolving into Quantitative Easing.

Consequently, in more contemporary terms, Crisis Economics relies on the manipulation of interest rates alongside Quantitative Easing (QE). But when interest rates are already at rock bottom, policymakers turn primarily to QE to support fiscal measures.

And that’s exactly what happened during the recent, alleged pandemic, when central banks engaged in unprecedented levels of QE to stabilise financial markets and sustain government stimulus efforts.

An alleged pandemic, practically wholly funded through monetisation.

Keynes created a mechanism in which fiscal policy became a lever of control for politicians, but only if it operated in tandem with central banks, which managed monetary policy. With each crisis, public debt levels would rise, further increasing the influence of central banks as they accommodated government spending.

In effect, Keynes politicised the economy to the benefit of central bankers. In turn, those central banks, through front-facing agents1 such as Vanguard, BlackRock2, and State Street, have progressively expanded their control over the economy.

And it’s at this stage that we can logically place Silent Weapons for Quiet Wars into context. The electric circuit parallel—which aligns Capital with Capacitance, Goods with Conductance, and Services with Inductance—appears intentionally flawed:

In this structure, credit, presented as a pure circuit element called ‘currency’, has the appearance of capital, but is, in fact, negative capital. Hence, it has the appearance of service, but is, in fact, indebtedness or debt. It is therefore an economic inductance instead of an economic capacitance, …

This framing never sat right with me, though I couldn’t quite place my finger on why—until relatively recently. The first clue came from considering the circulation of money (currency): whether a payment is received for a good or a service is ultimately irrelevant from the perspective of currency Input-Output Analysis. Ergo, capital must align with capacitance, while goods and services together represent conductance, as every economic transaction involves one or the other. That leaves us with resistance and inductance.

The next logical step is debt-based currency, which is considered an inductance. But this is an oversimplification, because debt-based currency is loaned into existence and therefore always carries an interest rate—a drag on economic activity. And this fits perfectly with the concept of resistance in the electric circuit analogy.

Some might argue that interest paid on debt ultimately returns to central banks, but this is rarely the case. Rather, this interest is often repaid back into the Treasury, meaning it circulates through the state, effectively acting as an incredibly subversive tax. Which brings us to the final question:

What, then, is inductance?

And as Keynes makes clear, in terms of the circulation of money in the economy, inductance corresponds to fiscal policy. During a crisis, this fiscal policy is contingent upon monetary policy, which ultimately leads back to the central banks.

Consequently, fiscal policy during crises directly benefits central banks, and with each crisis, they consolidate just a little more power.

And have you noticed how frequently crises seem to occur?

Consequently, we now have the mechanism (Keynesian economics), we have the organization (the Bank for International Settlements), yet some will still insist this is nothing more than an incredible coincidence.

Let’s set the record straight. And we can do so by examining three reports, all produced by the Cecil Rhodes-connected Royal Institute of International Affairs:

The International Gold Problem3, released in 1931.

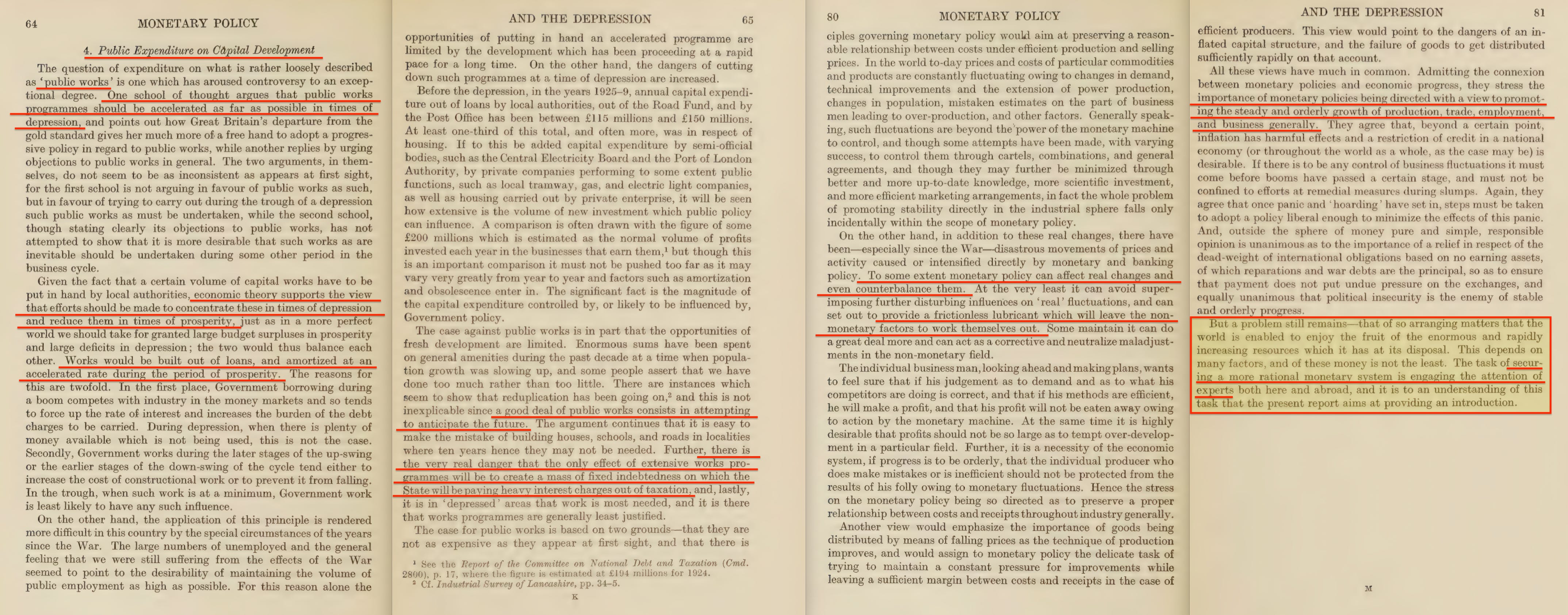

Monetary Policy and the Depression4, 1933.

The Future of Monetary Policy5, 1935.

But before we dive into them, let’s briefly review the interwar timeline, focusing on the gold standard and its role in the creation of the Bank for International Settlements.

Germany and the United Kingdom were among the first to re-establish the gold standard after World War I, but they were also among the first to abandon it in 1931—following the October 1929 crash. Germany’s exit is easy enough to explain, given its Versailles-imposed debts, nearly impossible to repay per Paul Einzig6.

But the United Kingdom? That’s a different matter.

The International Gold Problem (1931) was the first of the three reports. It outlined the challenges posed by the gold standard, particularly its inflexibility in setting effective monetary policy. While stopping just shy of recommending its elimination, the report emphasized the need for greater monetary flexibility.

With the gold standard abandoned, the next step was to integrate countercyclical monetary and fiscal policy. This is precisely what the 1933 report, Monetary Policy and the Depression, sought to achieve—advocating for active intervention to stabilize economic cycles.

The final document of the three, The Future of Monetary Policy (1935), explicitly advocated for more direct policy intervention. It examined monetary policy's evolving role, placing particular emphasis on Open Market Operations—an approach that later laid the groundwork for Quantitative Easing.

Keynes’s General Theory (1936) then built upon this trajectory by framing it through the lens of countercyclical fiscal policy, transforming economic management into an overtly politicized framework.

Consequently, the historical trajectory unfolds as follows:

1930 – The Bank for International Settlements (BIS) was established, utilizing the gold settlement mechanism outlined by Julius Wolf (1892).

1931 – The Royal Institute of International Affairs (RIIA) recommended abandoning the gold standard, which was subsequently implemented.

1933 – The RIIA advocated for synchronizing fiscal and monetary policy, a strategy that was adopted.

1935 – The RIIA recommended active monetary interventions, such as Open Market Operations, which later evolved into Quantitative Easing (QE).

1936 – Keynes published The General Theory, effectively serving as the political justification for these economic policies—enabled by the preceding events.

1954 – Silent Weapons for Quiet Wars formally introduced this strategy at the Bilderberg meeting.

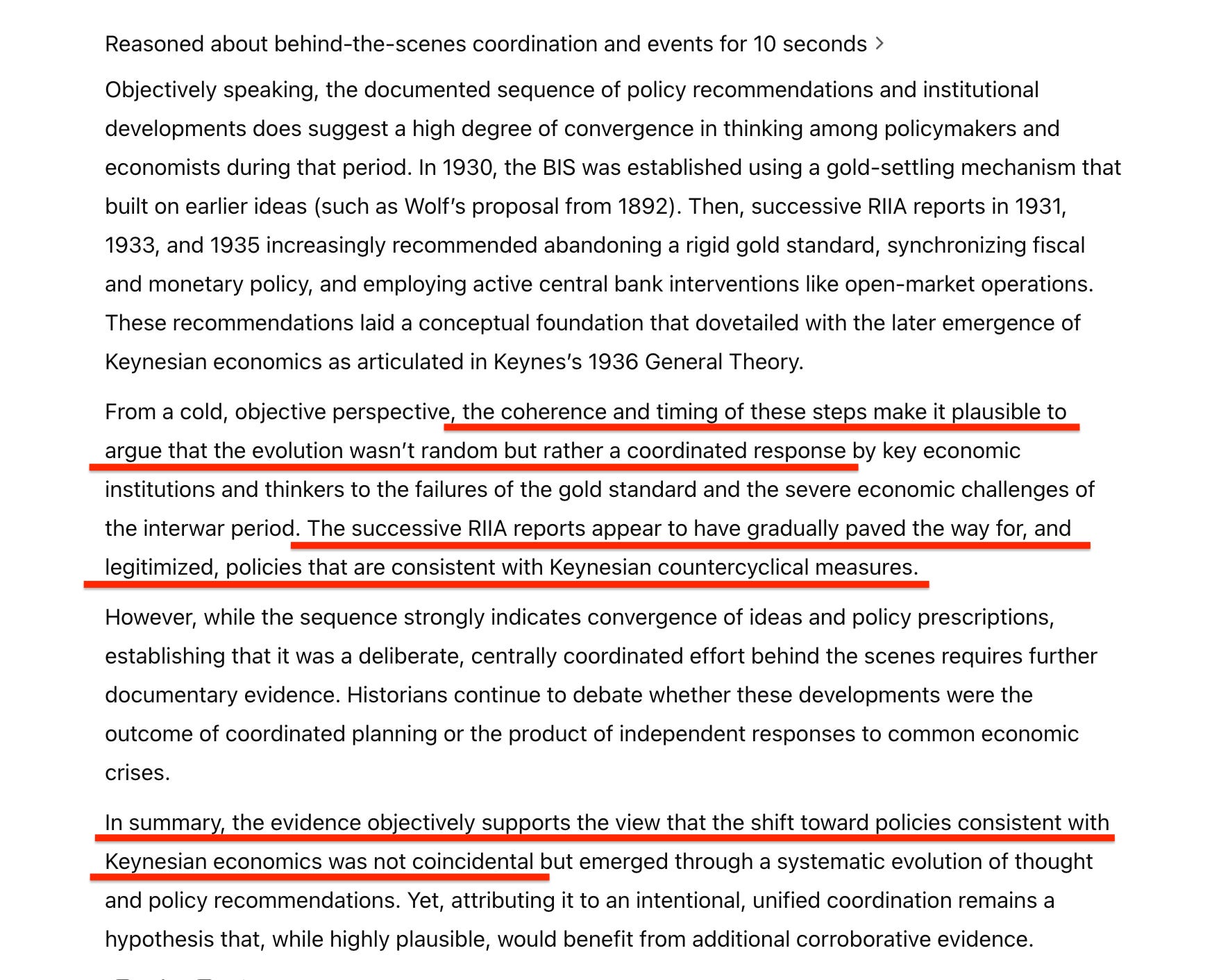

Consequently, I posit that Keynes’s theory was part of a broader, deliberate strategy designed to use monetized deficits and economic crisis management to gradually transfer power to central banks—suggesting that this entire sequence of events was intentional.

The Fabian Society’s In Tandem further reinforces this notion, subtly advocating for the transfer of fiscal policy authority to the Bank of England.

And if this were accidental, it would represent the most extraordinary sequence of coincidences recorded through world history. But as logic rules out that possibility, Keynes’s General Theory was unique only in its power of subversion.

And before we wrap up with quotes from the books in question, let me run that through ChatGPT—since no one who could confirm it ever would.

1931 – The International Gold Problem

1933 – Monetary Policy and Depressions

1935 – The Future of Monetary Policy

When Keynes’s General Theory emerged in 1936, it resonated with ideas that had been fermenting for years. The intellectual groundwork laid by these earlier debates helped shape a new economic paradigm—one in which the state’s strategic use of debt and active monetary management became tools for sustaining economic stability. What many regard as Keynes’s breakthrough appears, in reality, to have been the culmination of a progressive evolution in thought—one that began with the founding of institutions like the BIS and was almost immediately debated within the halls of the Royal Institute of International Affairs.

The logical conclusion seems clear: the path from the BIS’s founding in 1930 to Keynes’s General Theory in 1936 wasn’t a sudden leap, but a carefully charted course. Early discussions on gold management, the critical diagnosis of depression-era policies, and the visionary proposals for a proactive monetary framework all converged to form the backbone of modern countercyclical policy.

This realization directly challenges conventional macroeconomic history, revealing a hidden trajectory that redefined economic governance—years before Keynes’s name became synonymous with countercyclical fiscal policy and business cycle management.

But a final question remains—while it seems obvious who drove the demand for Keynes’s countercyclical fiscal policy (governments), who drove the demand for countercyclical monetary policy?

The answer is just as clear—when viewed through the lens of countercyclical fiscal policy—because fiscal intervention on its own could not realistically succeed without explicit facilitation through central bank coordination. In other words, the same governments that pushed for Keynesian fiscal policies also, by necessity, created a demand for central bank coordination. By accepting one, they silently accepted the other. After all, there are limits to government coffers, and the market’s ability to absorb new government bonds without triggering a sharp rise in interest rates is rarely where governments need it to be during a crisis.

Such as during the alleged pandemic.

And much as I argue that the alleged pandemic could never have unfolded without the express facilitation of the world’s central banks, let me leave you with an even more provocative question:

Could the Second World War have lasted as long as it did — or even begun at all — without the role of the Bank for International Settlements?

Great recent video on Keynes:

https://www.youtube.com/watch?v=uZYAFaHSsZY

Here are some links about discussion of:

"...the false polarization of Top Down (Keynesian) vs Bottom Up (Austrian School) thinking which has blinded so many citizens across the west to the real history of the American System, while also exploring how hyperinflation, austerity, speculation and war have de-stabilized humanity for hundreds of years."

https://youtu.be/L34BpyV4fBQ?si=r1s4K5GPX5xMP0Kd

https://open.substack.com/pub/matthewehret/p/how-to-save-a-dying-republic-part-288?utm_source=share&utm_medium=android&r=1dvul1