Stranded in Haifa

For a century, every plan to move Middle Eastern energy to Europe has ended at the same place: Haifa.

The route has never changed.

What has changed is the scale, the layers of control built on top of it, and the number of alternatives that had to be removed before it became the only option.

The first pipeline

In 1927, the Iraq Petroleum Company struck oil at Baba Gurgur, north of Kirkuk12. The problem was geography: Kirkuk was isolated, and the markets that wanted the oil were in Europe. The solution was a pipeline — two, in fact — running westward from Kirkuk to the Mediterranean. The northern line ran through Syria to Tripoli in French-mandated Lebanon. The southern line ran through Transjordan to Haifa in British-mandated Palestine.

Construction began in 1932 and was completed in 1934. It was the world’s first transnational oil pipeline3, described at the time as the most ambitious engineering project of its era. The Iraq Petroleum Company was a consortium of Anglo-Persian (now BP), Royal Dutch Shell, Compagnie Française des Pétroles (now Total), and American oil majors. Calouste Gulbenkian held his famous five per cent share — a position on the path between production and market, not in either domain.

Oil arrived at Haifa, was refined, stored in tanks, and shipped by tanker to Europe. By 1939, the Haifa refinery could process the entire supply4. During the Second World War, the pipeline and refinery provided much of the fuel for British and American forces in the Mediterranean.

In 1948, with the establishment of the State of Israel, Iraq shut off the pipeline5. The route that had supplied Europe with oil for fourteen years was severed by politics. The Haifa refinery lost its supply, and the southern line never reopened.

The second pipeline

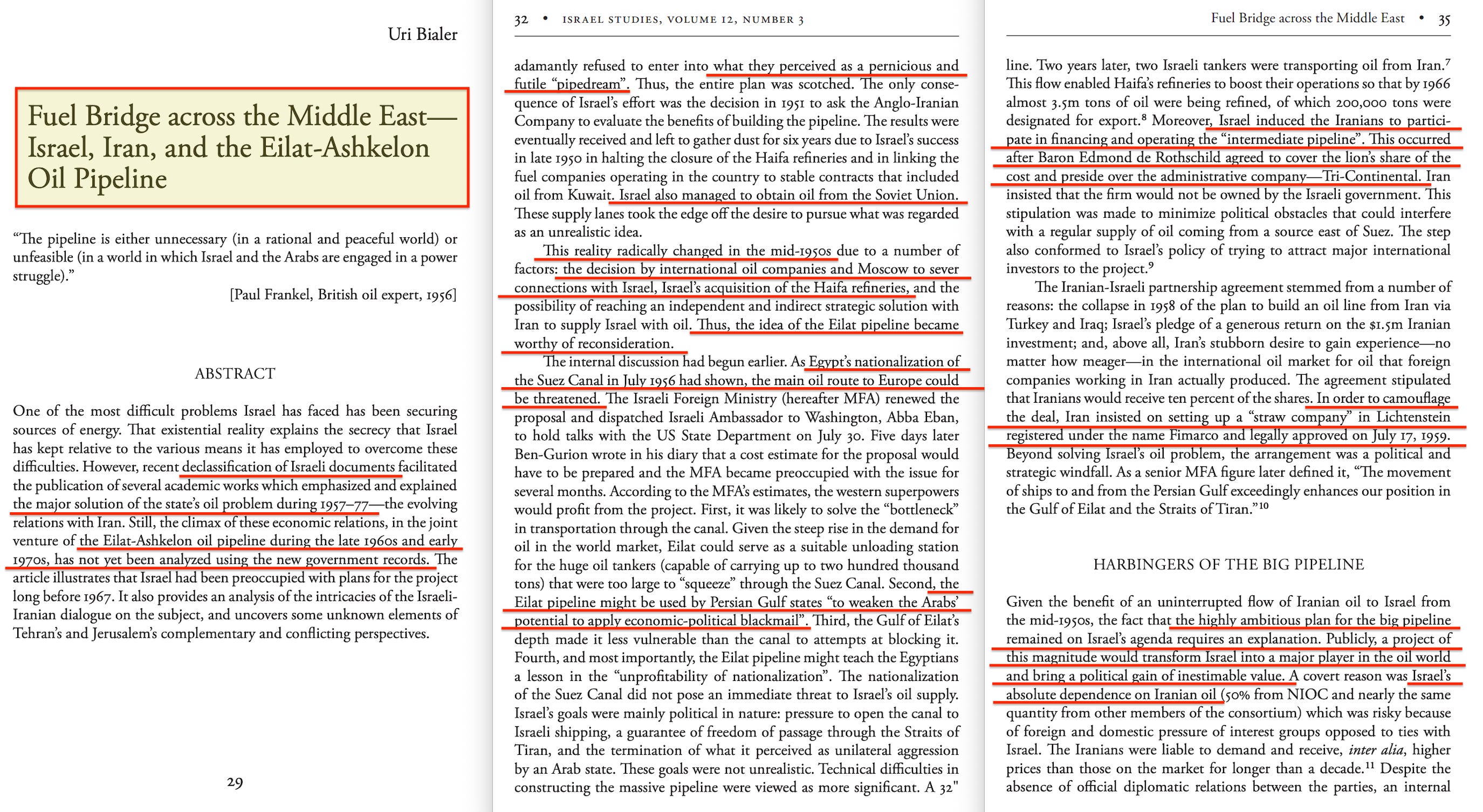

The closure of the Kirkuk-Haifa line, followed by Egypt’s nationalisation of the Suez Canal in 19566, created the conditions for the next iteration. Israel had lost its oil supply from Iraq, been cut off from the Suez Canal, and seen the Soviet Union cancel its oil deliveries7. Every alternative had been removed.

The idea of an overland pipeline from Eilat on the Red Sea to the Mediterranean had been discussed in Israel since 1950, when the British Foreign Office dismissed it as a ‘pipedream’. By 1957, the idea had become operationally necessary. A small-diameter line from Eilat to Beersheva was laid using equipment expropriated from an Italian oil company in Sinai. Iranian oil began flowing through it almost immediately.

By 1968, the project had scaled into a 42-inch, 254-kilometre pipeline from Eilat to Ashkelon — a joint venture between Israel and Iran’s National Iranian Oil Company. Baron Edmond de Rothschild agreed to cover the lion’s share of the financing and presided over the administrative company, Tri-Continental8. Iran insisted the venture could not be owned by the Israeli government, so a front company called Fimarco was registered in Liechtenstein to camouflage the arrangement.

The pipeline’s function was identical to the Kirkuk-Haifa line: route Gulf oil overland through Israel to the Mediterranean, bypassing the Suez Canal. Its terminals could handle supertankers too large for the canal. Over ninety per cent of Israel’s oil imports came from Iran through this route.

The pipeline operated under a blanket state decree that shrouded its affairs in secrecy for reasons of national security. The Eilat Ashkelon Pipeline Company remains one of Israel’s most secretive institutions to this day9.

In 1979, the Iranian Revolution severed the partnership. Israel nationalised the company10, and the pipeline lost its source. The architecture failed because it depended on a single political relationship and a single ruler.

The lesson the architecture learned

The vulnerability that killed the Eilat-Ashkelon pipeline was its dependence on one supplier and one political relationship. When the Shah fell, the oil stopped flowing and the infrastructure became stranded.

The current iteration — IMEC — appears to have been designed to eliminate that vulnerability.

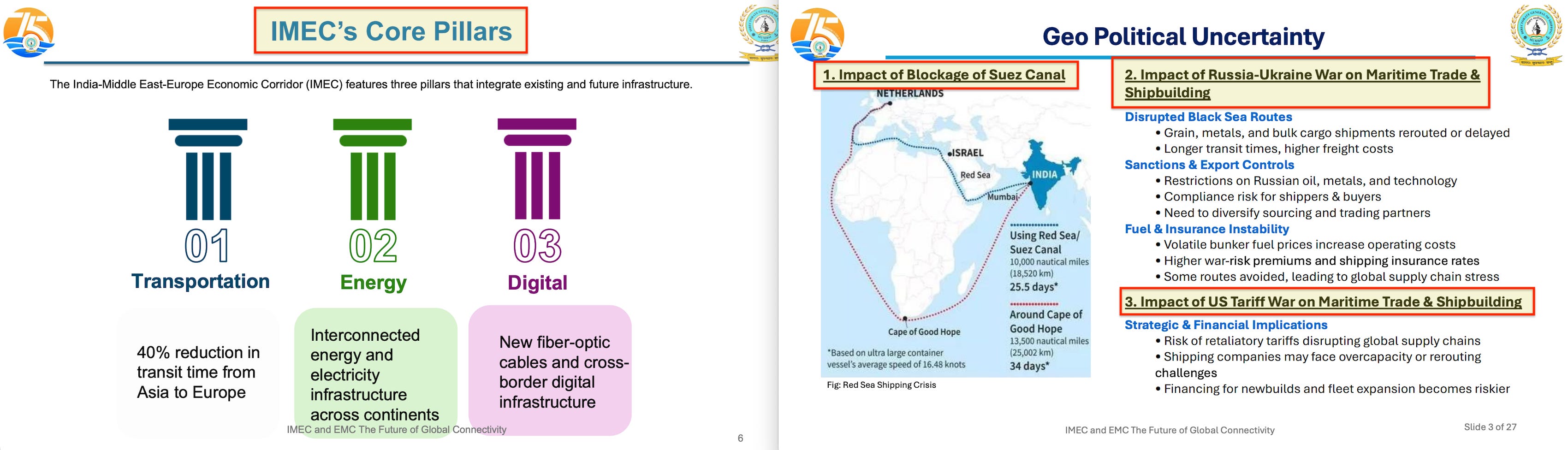

Rather than depending on a single supplier, the corridor connects multiple Gulf producers: the UAE, Saudi Arabia, and potentially Oman. Rather than depending on a bilateral political relationship, it operates through multilateral agreements and institutional frameworks. Rather than depending on a single commodity, it carries energy, goods, data, and money simultaneously1112.

And rather than depending on political goodwill for compliance, it embeds conditions into the infrastructure itself through programmable standards, digital settlement layers, and regulatory frameworks that operate automatically.

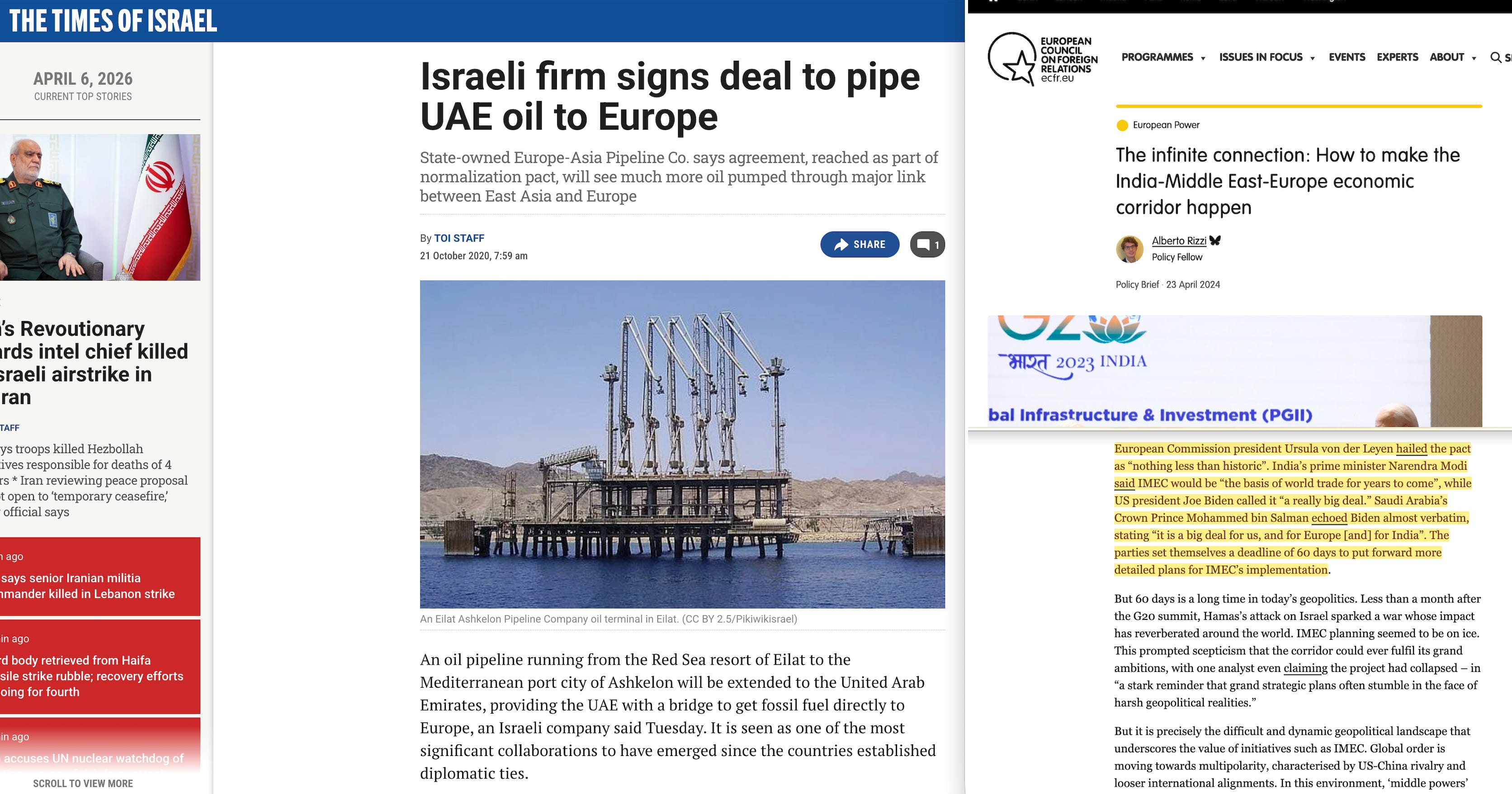

The Abraham Accords13, signed in 2020, reopened the route. Within weeks, the Israeli state-owned Europe Asia Pipeline Company and the UAE-based MED-RED Land Bridge signed an agreement to move Emirati oil through the Eilat-Ashkelon pipeline14 — the same physical infrastructure built in 1968, now carrying UAE oil instead of Iranian oil.

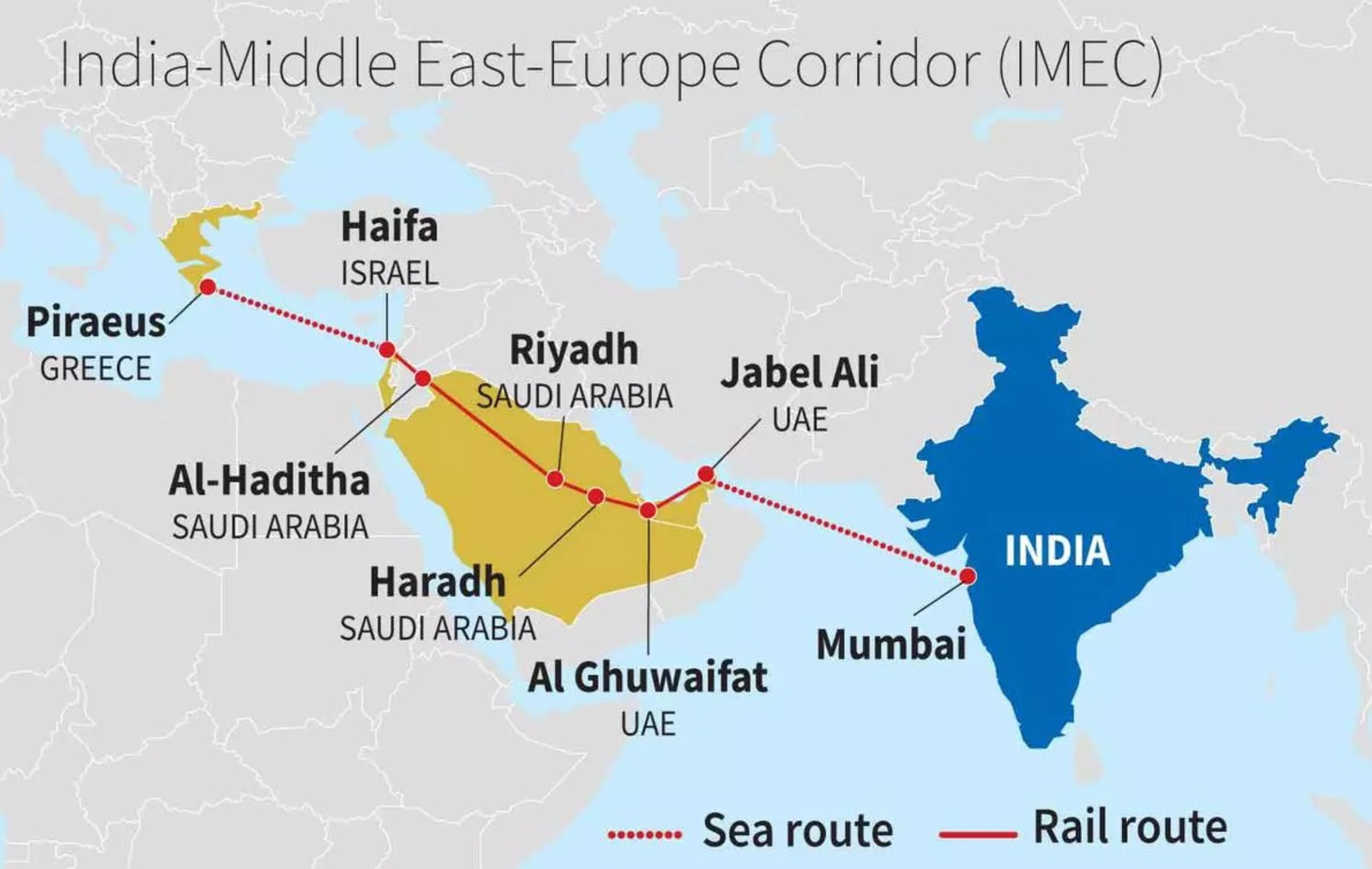

In 2023, IMEC was announced at the G20 summit in New Delhi15. The corridor runs from India through the UAE and Saudi Arabia, overland through Jordan to Israel’s port of Haifa, and across the Mediterranean to Europe. It includes rail, pipeline, fibre optic cable, hydrogen pipeline, and electricity cable. European Commission President Ursula von der Leyen called it ‘nothing less than historic’16.

The route is the same route proposed in 1932. The terminus is the same terminus. The function — sitting between Gulf production and European consumption, routing everything through a single node — is identical. What has changed is the number of layers built on top of the physical infrastructure, and the degree to which those layers make the arrangement self-enforcing.

The layers

The Kirkuk-Haifa pipeline in 1932 was a physical pipe and nothing else. Oil flowed from producer to consumer through a fixed route. The control was visible: the Iraq Petroleum Company owned the concession, the consortium members set the terms, and everyone knew who sat in the middle.

The Eilat-Ashkelon pipeline in 1968 added a financial layer. Rothschild funding, shell companies in Liechtenstein, military credit bundled with oil supply — Israel provided Iran with $75 million in military equipment financing, repaid in oil once the pipeline operated. The control was less visible: the ownership was concealed, the financial arrangements were secret, and the pipeline operated under a state secrecy decree.

IMEC in 2023 adds a regulatory and digital layer. The corridor’s three pillars — transportation, energy, and digital connectivity — carry not just goods but conditions. The energy pillar delivers hydrogen produced to standards set by the EU’s taxonomy. The digital pillar runs fibre optic cables that carry data subject to cross-border regulatory frameworks. The financial transactions that flow through the corridor clear through settlement systems — mBridge or Agorá — built by the Bank for International Settlements.

The compliance conditions are environmental, financial, and regulatory, calibrated through Basel 3.1, the NGFS climate scenarios, and ESG metrics developed at forums including those hosted at Waddesdon Manor between 2014 and 2018.

Each layer makes the control less visible and harder to challenge.

A physical pipe can be shut off by a government. A financial arrangement concealed through shell companies can be exposed and unwound. But a regulatory framework embedded in the capital requirements of every bank in Europe, enforced through institutional protocols that no parliament voted on, operating automatically through programmable compliance — that cannot be shut off by any single actor.

The elimination of alternatives

At each stage, the route through Israel became operational only after the alternatives were removed.

In 1948, Iraq shut off the Kirkuk-Haifa pipeline, Egypt closed the Suez Canal to Israeli shipping, the Soviet Union cancelled oil deliveries, and the international oil companies refused to sell. The Eilat pipeline became necessary because every other source of supply had been cut off.

In 2022, Russian pipeline gas to Europe was severed by the Ukraine war and made physically irreversible by the destruction of the Nord Stream pipelines17. Between 2014 and 2018, the stranded assets framework developed at Waddesdon Manor fed through the TCFD and the NGFS into Basel 3.1, making European domestic fossil fuel development financially unbankable. In 2026, the US-Israeli war on Iran closed the Strait of Hormuz18, destroyed Iran’s military capacity, and eliminated the competing corridors — the International North-South Transport Corridor and Iraq’s Development Road — that would have bypassed Israel. Qatar’s LNG capacity was struck by Iranian missiles, taking seventeen per cent of its export capacity offline.

The pattern is consistent across ninety years. The route through Israel does not compete with alternatives. It becomes viable when the alternatives are removed19. The removal is accomplished through different mechanisms — war, regulation, physical destruction — operated by different actors, over different timescales. But the outcome is the same each time: the node at Haifa becomes the only option.

The two theatres

The corridor creates dependency through two distinct mechanisms aimed at two different powers.

Europe loses sovereignty through energy. It cannot develop domestic fossil fuels because the stranded assets framework makes them impossible to finance. It cannot restore Russian supply because the infrastructure has been physically destroyed. It cannot diversify through Iran because the United States and Israel are destroying the alternatives.

What remains is imported energy through IMEC, on conditions attached to its digital and regulatory infrastructure. European politicians — von der Leyen, Meloni, Macron — celebrate the corridor as historic while their regulatory architecture ensures Europe cannot build an alternative to it.

The United States loses sovereignty through the dollar. America provides the diplomatic capital, military force, and financial backing to build the corridor. Trump called it ‘one of the greatest trade routes in history’. But the physical infrastructure is currency-agnostic.

The rail, the pipeline, the fibre optic cable — none of it changes when the financial layer swaps from SWIFT to mBridge. Every IMEC corridor state — the UAE, Saudi Arabia, India — sits on both settlement platforms. The moment mBridge offers better terms, the clearing switches.

The dollar funded the construction of the corridor that no longer requires the dollar.

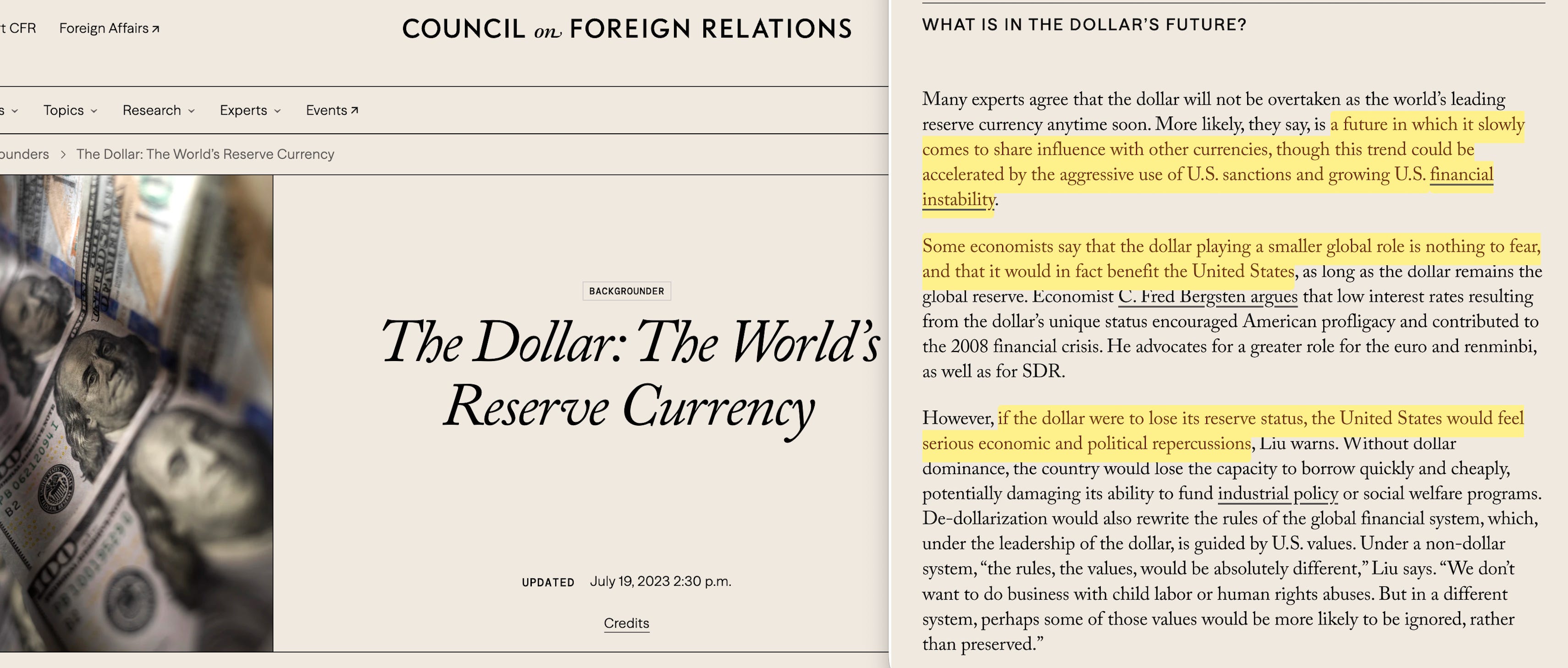

The Council on Foreign Relations — the institution that shaped American foreign policy for a century — is already publishing the intellectual framework for why this is acceptable2021. Its backgrounder on dollar dominance describes a future in which the dollar ‘slowly comes to share influence with other currencies’ and notes that some economists argue this would ‘benefit the United States’. Chatham House, the CFR’s British counterpart, publishes frameworks for ‘reducing dependencies’ and navigating a ‘multipolar world’. Both institutions present the erosion of their home nations’ strategic advantages as rational, inevitable, and beneficial.

The beneficiary of a multipolar world is never the poles. It is whoever sits between them and sets the standards by which they interact. Leonard Woolf made this argument in 1916, in the Fabian Society report that became the blueprint for the League of Nations.

The question this raises is whether the United States is a victim of this architecture or its co-designer.

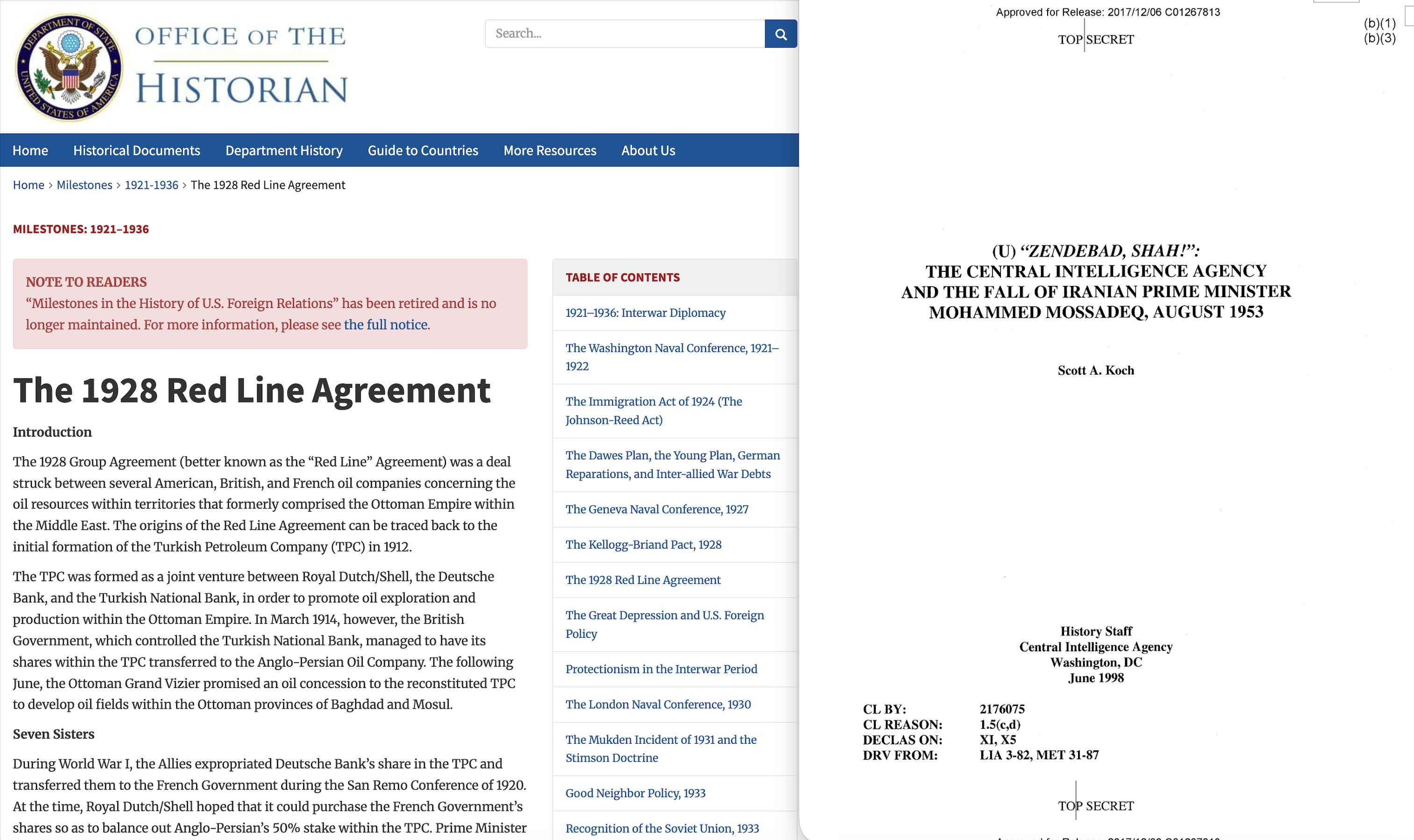

The hundred-year record suggests it is both. America has enforced the node’s viability at every stage — the 1928 Red Line Agreement that carved up Ottoman oil22, the 1953 coup that secured Iranian supply23, the military protection of Gulf shipping lanes for decades, and now the destruction of Iran’s military capacity to clear the corridor’s final obstacle24. At each point, the United States acted as the enforcer of a system whose long-term beneficiary was the node, not the enforcer.

The CFR’s current framing — that dollar erosion is manageable, even beneficial — is the intellectual preparation for America to accept the consequences of an infrastructure it built for others to operate. The enforcer, having constructed the corridor and eliminated every competing route, is being captured by the architecture it enabled. Even the hegemon, in the end, becomes a franchisee.

The corridor, then, is not one trap but two — an energy clearinghouse between Arabia and Europe, and a money clearinghouse between the United States and China. Both route through the same physical infrastructure. Both clear through the same settlement systems built by the BIS in Basel.

The energy clearinghouse determines what flows between producer and consumer, and on what conditions. The money clearinghouse determines what denomination those flows settle in, and whether the dollar is required. One corridor, two clearinghouse functions, two powers subordinated through different mechanisms.

This is the unified ledger — the BIS’s own blueprint for the future monetary system — made physical.

The node

For a hundred years, every plan to connect Gulf energy production to European consumption has routed through the same point. The Kirkuk-Haifa pipeline in 1932. The Eilat-Ashkelon pipeline in 1968. The EAPC-MED-RED agreement in 2020. IMEC in 2023. The source has rotated — Iraqi oil, Iranian oil, Emirati oil, green hydrogen.

The financial layer has upgraded — visible consortium, secret joint venture, programmable settlement.

The regulatory layer has accumulated — from no conditions, to concealed conditions, to automated compliance.

The scale has expanded — from a single pipeline to a multimodal corridor carrying energy, goods, data, and money across three continents.

But the central node never moved. The route has never changed, and the function — sitting between producer and consumer, controlling what passes through — has been identical since the first pipe was laid from Kirkuk to Haifa in 1932. The outcome, in every iteration, is the same: a clearinghouse inserted between oil producer and consumer.

In the early 1930s, a Fabian-linked organisation called Political and Economic Planning published a pamphlet titled Freedom and Planning. It proposed decoupling distribution from production, installing an unelected planning authority between producer and consumer, and setting the standards by which goods would flow. The pamphlet noted that of all Britain’s institutions, only one would require no structural change to fit the new order: the Bank of England.

Ninety-four years later, the architecture is the same — but the scale is now global.

The institution that now requires no change is the Bank for International Settlements — which published the unified ledger blueprint, calibrates the capital requirements, and built the settlement infrastructure through which the corridor will clear — be it mBridge or Agorá.

The central clearinghouse node never moved, but the architecture developed. And the alternatives, this time, are not coming back.

And the eventual result could well bring an end to Western hegemony.

h/t Freedom Fox for the historical links.

The Iranians don't appear to be military defeated at this moment in time.

I knew you could take the info links and analyze it, make it digestible to readers.

In the immortal words of Tenacious D, That's F'in Teamwork!

https://www.youtube.com/watch?v=X6n5ndX6yTs