The Crossing

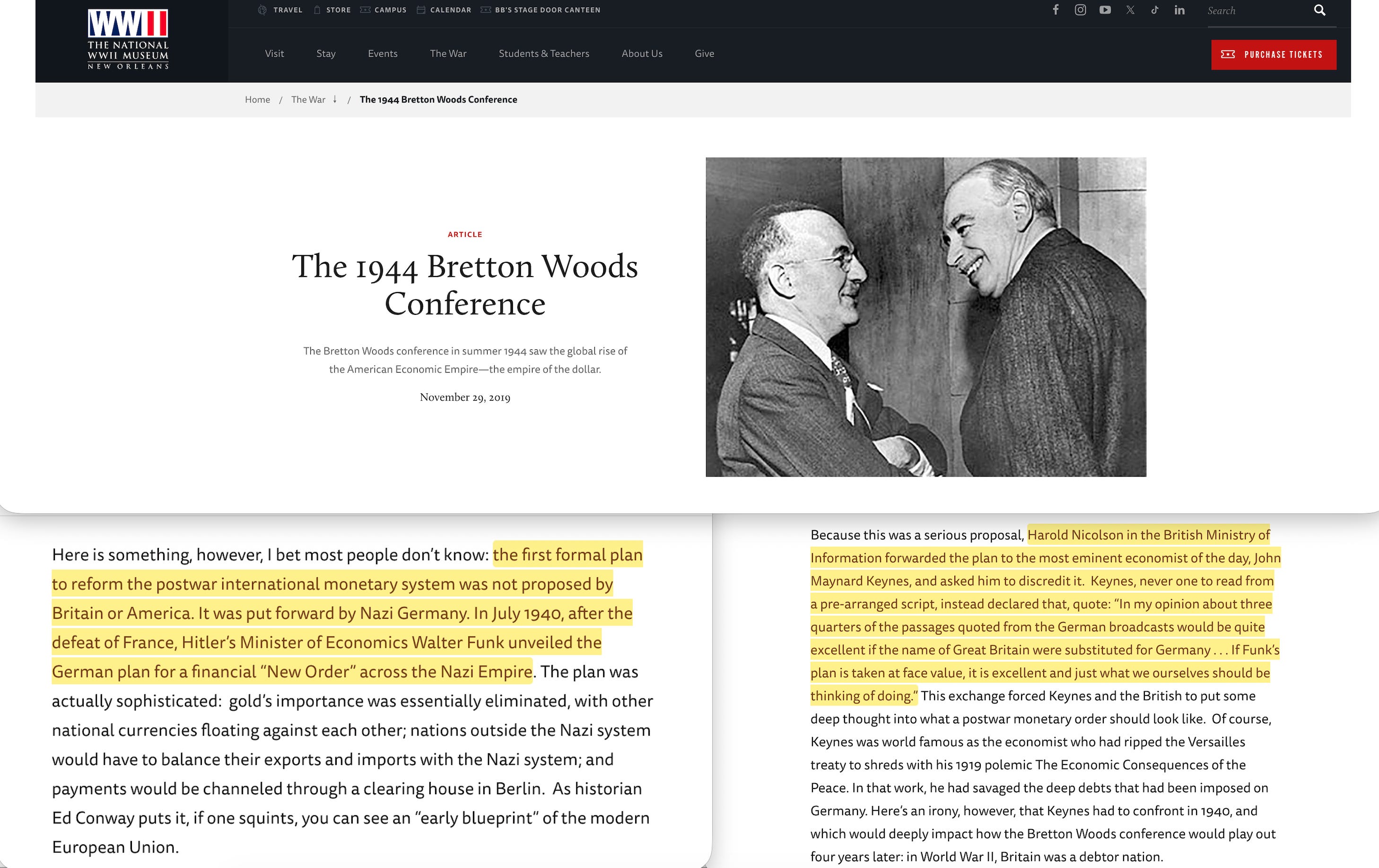

In November 1940, Harold Nicolson at Britain's Ministry of Information sent Walther Funk's European economic plan to John Maynard Keynes and asked him to discredit it publicly

Keynes refused.

His response:

In my opinion about three quarters of the passages quoted from the German broadcasts would be quite excellent if the name of Great Britain were substituted for Germany... If Funk’s plan is taken at face value, it is excellent and just what we ourselves should be thinking of doing.

The British response

Keynes then built the British version. His International Clearing Union, proposed in 1941 and presented at Bretton Woods in 1944, replaced the Reichsmark with Bancor and London with an international clearing centre. The Keynes plan ‘was conceived as a response to the Nazi plan to establish a multilateral clearing system. However, Keynes did not elaborate a plan radically opposed to the Nazi proposal, but shared its essential core’. The recognition went both ways — Reichsbank vice president Puhl welcomed Keynes’s plan, seeing the same clearing architecture under different management.

Same form, different operator. Europäische Wirtschaftsgemeinschaft showed how the 1942 volume laid out the European Economic Community’s entire institutional architecture fifteen years before the Treaty of Rome. Keynes’s response shows this architecture crossing from one side of the war to the other — because an economist could read the specification and judge it on its merits.

Keynes didn’t adopt Funk’s plan because of the regime. He adopted the clearing mechanism because he found it useful. A multilateral clearing system that settles payments between nations through bookkeeping rather than gold shipment solves the problem that had crippled international trade since 1931 — the chronic shortage of settlement currency that forced countries into bilateral barter. The gold standard had collapsed, bilateral clearing created bottlenecks, and multilateral clearing through a central institution was the answer.

The differences between Keynes’s plan and Funk’s specification were political. Keynes proposed symmetrical adjustment — both surplus and deficit countries sharing the burden of rebalancing. Funk’s system put Germany at the centre with no adjustment obligation. Keynes wanted an international institution governed by member states; Funk’s system was run by the Reichsbank. But the clearing function itself — multilateral netting of payment balances through a central institution, with exchange rates managed against an anchor currency — was identical.

Bretton Woods adopted the American plan (White’s) rather than Keynes’s, but the clearing architecture survived in every later European monetary arrangement. The European Payments Union, set up in 1950, was a multilateral clearing mechanism run through the BIS, settling net balances monthly, with conditional credit for debtors and mandatory gold settlement for persistent surplus countries. The Deutsche Verrechnungskasse’s function moved to Basel.

The American response

The same month Keynes got Funk’s plan, Roosevelt’s National Resources Planning Board commissioned a confidential memorandum on the Nazi economic system across the Atlantic. Its introduction states: ‘there is a wide-spread feeling that, whatever our attitude toward Nazi philosophy, its economic procedures may carry a lesson for democratic countries’.

In November 1940, two Allied governments independently studied the same architecture, and asked whether democratic countries could learn from it. The postwar adoption of the clearing architecture was driven by Allied planners who’d studied the specification during the war and recognised its effectiveness.

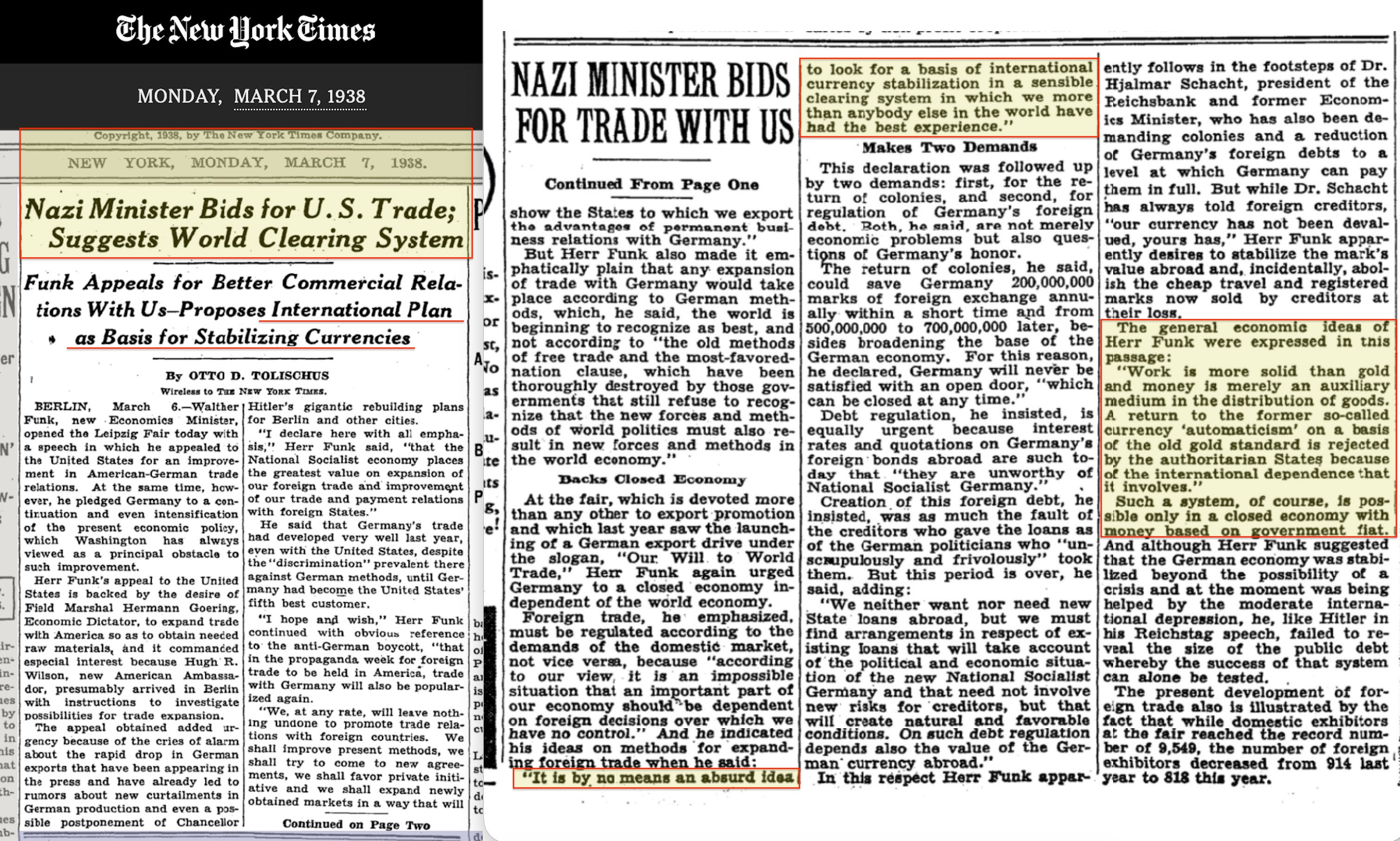

The architecture was published, broadcast, studied, and filed by the people who would build the postwar order. Funk’s Leipzig speech of March 1938 — ‘such a system, of course, is possible only in a closed economy with money based on government fiat’ — was reported on the front page of the New York Times.

The Van Zeeland bridge

In 1937, British and French governments commissioned Belgian Prime Minister Paul Van Zeeland to report on reducing trade barriers and restoring economic cooperation. Belgian diplomat Robert Rothschild served on the mission and drafted memoranda setting out the postwar institutional architecture in one document: fixed but adjustable exchange rates, a common fund for countries in financial difficulty, a freeze on tariffs followed by gradual reduction, and the Bank for International Settlements as managing body.

The tariff framework became GATT, the exchange rates became Bretton Woods, and the common fund became the IMF. Rothschild carried that framework across twenty years to help draft the Treaty of Rome in 1957.

Van Zeeland’s report sat between the German specification and the postwar implementation. Commissioned by democratic governments, it proposed the same institutional architecture that the 1942 volume would specify under authoritarian management. The form stayed the same because the problem hadn’t changed: how to organise continental economic flows when the gold standard had collapsed and bilateral clearing couldn’t scale.

The postwar sequence

The European Payments Union ran from 1950 to 1958. When it dissolved, the European Monetary Agreement replaced it — a softer clearing mechanism — and the Treaty of Rome embedded the clearing function into a permanent framework covering trade, agriculture, transport, and labour.

The same pattern repeated at every stage. The EMA gave way to the Snake, the Snake to the European Monetary System, the EMS to the Exchange Rate Mechanism, and the ERM to the eurozone. Every transition came from a crisis in the previous arrangement, and every crisis was resolved by extending the clearing function rather than dismantling it. The 1992–93 ERM crisis — when Soros broke the Bank of England and Italy crashed out — didn’t produce a retreat to floating rates. Instead, it accelerated the move toward full monetary union. The Maastricht Treaty was already signed. The failure of partial clearing produced total clearing.

Benning had identified the structural risk in his 1942 chapter on European currency questions. The income gap between northern and southeastern Europe was enormous — per-capita income in the northwest ran at three to four times the southeastern level. A premature single currency would founder on these differences. He proposed a partner-currency system with managed exchange rates instead, aligned gradually toward convergence. The Maastricht convergence criteria tried to solve the same problem Benning had diagnosed — and the eurozone sovereign debt crisis of 2010–2012 confirmed that the investment hadn’t produced the convergence Benning had warned was required.

The clearing architecture produced imbalances, the imbalances produced crisis, and the crisis produced more architecture — the European Stability Mechanism, the Fiscal Compact, the Banking Union, the Single Supervisory Mechanism, the Single Resolution Mechanism, and ECB bond-buying programmes. Six new layers of institutional control over national fiscal and banking policy, each extending the clearing function deeper into member states’ economic life.

The direction was always the same: more gates, more conditions, more institutional authority, and more domains covered. Never less, never dismantling, never returning to the simpler system that preceded the crisis.

The Hallstein question

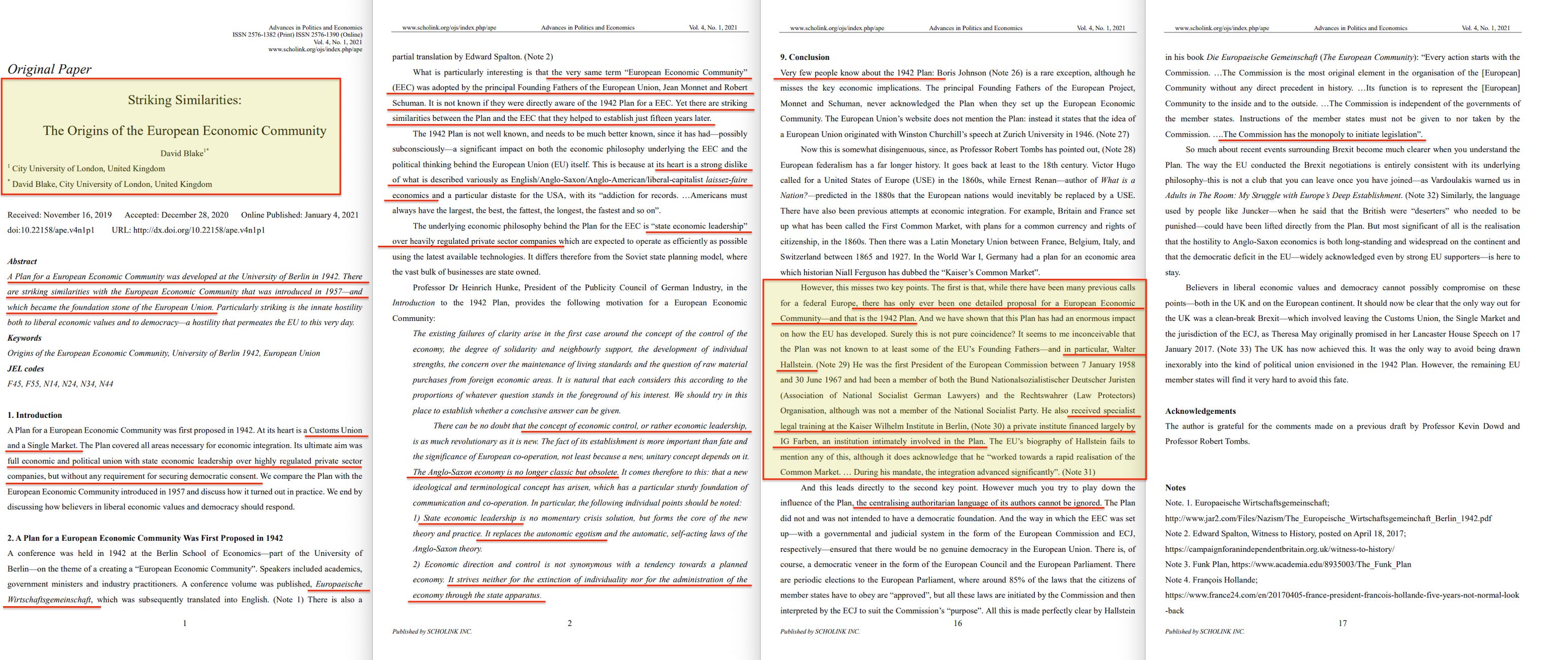

Walter Hallstein became the first President of the European Commission in 1958. His background was in Nazi-era legal academia — he held a chair in law at the University of Frankfurt, was a member of the Bund Nationalsozialistischer Deutscher Juristen, and delivered a 1938 lecture on the legal foundations of the Großraum. His later book Die Europäische Gemeinschaft described the Commission as independent of member-state governments, immune from member-state instructions, holding a monopoly on initiating legislation, and unprecedented in institutional history. The form he called unprecedented was the same form the 1942 conference proceedings had specified sixteen years earlier.

David Blake’s 2020 City University paper, which documents the parallels between the 1942 volume and the Treaty of Rome, notes that ‘it’s not known’ whether Jean Monnet and Robert Schuman were directly aware of the 1942 plan. He adds that it seems ‘inconceivable’ that Hallstein didn’t know, given his background.

Hallstein wasn’t alone. Karl Blessing, a Schacht protégé who served on the Reichsbank Directorate during the war, became President of the Deutsche Bundesbank in 1958 — the central bank whose currency would anchor European monetary integration. And Bernhard Benning, who wrote the 1942 volume’s currency chapter — the partner-currency system, the managed exchange rates, the rejection of premature single currency on convergence grounds — sat on the Bundesbank Zentralbankrat by December 1957. The man who’d specified the European monetary architecture under one regime was on the central banking council of the institution that’d implement it under another.

The 1942 volume wasn’t an obscure document produced by marginal figures. It was published by Berlin’s leading commercial association and its business school, and featured contributions from the Reichswirtschaftsminister, the head of IG Farben’s economics department, a Ministerialdirektor at the labour ministry, and the Foreign Ministry’s chief treaty negotiator. By 1942, these ideas were the common currency of German institutional economics. Any trained German economist or legal scholar working on European economic integration in the 1950s would’ve encountered the same concepts, vocabulary, and institutional designs — whether or not they’d read this particular volume.

What the crossing demonstrates

The architecture moved from wartime Berlin to postwar Brussels along three routes.

First, direct study. Keynes read Funk’s plan and backed its core. Roosevelt’s planning board studied the Nazi economic system and filed it. Allied intelligence watched German economic arrangements throughout the war, so the postwar planners had the blueprint in front of them.

Second, institutional continuity. The BIS, founded in 1930, operated throughout the war and became the base for the European Payments Union. The clearing function didn’t need reinventing — it was already running in Basel when the EPU began. The Deutsche Verrechnungskasse’s multilateral clearing moved to an international body that predated and survived the war, then hosted the postwar version.

Third, professional continuity. The economists, lawyers, and administrators who built Europe’s institutions came from the same tradition as those who’d drawn up the 1942 architecture. They’d studied the same textbooks, attended the same conferences, and worked within the same systems. The 1942 volume’s contributors and the Treaty of Rome’s architects shared the same ideas, even when they stood on opposite sides of the war.

The conventional story treats the European project as a democratic peace initiative born from fascism’s ashes. The documents show an architecture designed to govern continental economic flows, drawn up under one regime, backed by the other side’s top economists during the war, and put into practice by the winners using the same forms, tools, and on occasion even words.

Fascism installed it, democracy operates it. The form outlasted both operators because it was never about the ethic — it was about the clearing function.

Funk said it on page 24 of the 1942 volume: the fascist and then the National Socialist revolution created the foundation for a new political and social order. The architecture needed a rupture to install — the old system of liberal parliamentarism, gold-standard orthodoxy, and Anglo-Saxon free trade doctrine wouldn’t dismantle itself. But once installed, it survived the destruction of the regime that built it, because the form’s ideology-neutral in operation even when its installation isn’t. Every implementation has needed a rupture — revolutionary, military, or institutional — that the architecture itself couldn’t produce. The rupture belongs to the operator, the form continues regardless.

The ethic shifted from Volksgemeinschaft to democratic peace to European solidarity to sustainability, and the clearing function settled payments the same way under each one.

The CIA documented the same crossing pattern in the Soviet specification through declassified files. In 1975, Alan Greenspan — then Chairman of the Council of Economic Advisers — requested a CIA report on Gosplan. He became Chairman of the Federal Reserve twelve years later. McNamara’s PPBS at the Pentagon copied Gosplan’s three-layer architecture — planning, compliance monitoring, resource allocation — under American management. IIASA in Laxenburg merged both systems formally from 1972. The architecture crossed the war from Berlin and the Cold War from Moscow.

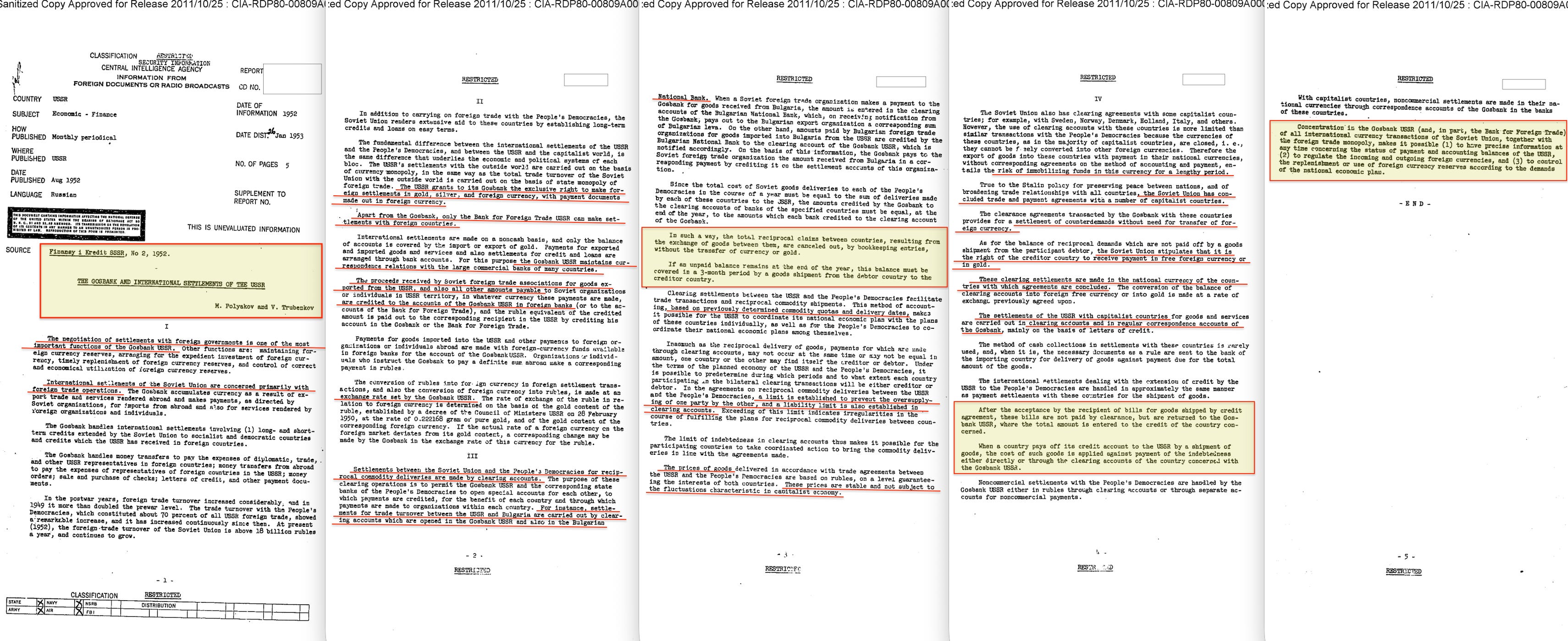

A 1952 CIA report on ‘The Gosbank and International Settlements of the USSR’1 documented the Soviet version in detail. Bilateral clearing accounts between the USSR and the People’s Democracies, periodic netting of balances, commodity delivery plans determining what cleared, the Gosbank holding the exclusive right to settle in gold, and state monopoly of foreign trade enforced through the clearing layer. The report identified Gosbank’s four core functions: providing information on foreign trade flows, maintaining planned accounting balances, regulating incoming and outgoing foreign currencies, and controlling the use of foreign currency according to the demands of the national economic plan. That’s Verrijn Stuart’s 1932 specification — central bank authority above the nation, controlling settlement — implemented under Soviet management. The structural parallel with Schacht’s bilateral clearing system was exact: the national economic plan determined what cleared, bilateral accounts accumulated balances, and Gosbank settled. Three regimes — fascist, communist, democratic — all arrived at the same clearing architecture.

The two threads converged at Basel, where the BIS had been operating since 1930 — Wolf’s international clearing office, hosting the postwar version of the mechanism all sides eventually adopted.

They were never on different sides in the first place.

cf Anthony Sutton on Wall Street funding both the Bolsheviks and the Nazis.

So, not v surprising if they all converged in 1957 or whenever.

That was always the plan, the Kalergi plan.

Perhaps superfluous for those following ESC's work, but — as an intermediate shortcut and to put things in a broader perspective, this:

"A multilateral clearing system that settles payments between nations through bookkeeping rather than gold shipment solves the problem that had crippled international trade since 1931 — the chronic shortage of settlement currency that forced countries into bilateral barter. The gold standard had collapsed, bilateral clearing created bottlenecks, and multilateral clearing through a central institution was the answer."

is a driving force behind multilaterism (today) —> (technocratic) globalism in an ethical guise.

https://www.iberdrola.com/social-commitment/what-is-multilateralism

Because, as ESC rightly notes: "it was never about the ethic(s) — it was about the clearing function."

Naturally, you are not presented with these 'bridges' during your economics studies at university. Not even during (exclusive) 'Globalization' lectures by a former PM and later UN Secretary.

Instead "you'll study the choices made by individuals, businesses, and governments and how those choices impact the world."