The Van Zeeland Report

The textbook account of how the postwar world was built goes like this.

The Second World War showed that the 1930s had failed. Leaders gathered at Bretton Woods in 1944 to create new institutions. Keynes and Harry Dexter White drew up the plans. The IMF, World Bank, GATT, and the United Nations were the result.

This account is tidy — and wrong.

A closer look at documents produced between 1930 and 1944 shows that nearly every major element of the postwar economic order had already been designed before the war broke out.

The story begins in 1930 with the founding of the Bank for International Settlements. The BIS was officially set up to handle German war reparations, but its design drew on much older ideas.

In 1892, the economist Julius Wolf proposed an international gold clearing system at the Brussels Monetary Conference1. His idea was simple: take the model that had been working inside Britain for decades and apply it between countries. In Britain, the London Bankers’ Clearing House2 settled payments between banks through a central node, with the Bank of England at the top. Wolf wanted to do the same thing between nations. At the same conference, Alfred de Rothschild3 — representing the British Government and a former director of the Bank of England — described that London clearing house system as ‘approaching perfection’4.

Wolf didn’t stop at money. In 1904, he proposed a European-wide system of cross-border economic cooperation5 — the trade half of the same programme. The BIS, when it was founded in 1930, adopted Wolf’s monetary framework almost entirely, making itself the coordinator of central bank operations across national borders. Van Zeeland’s 1938 report would later combine both halves — the monetary clearing and the trade liberalisation — into a single blueprint.

Within a year of the BIS’s creation, the Royal Institute of International Affairs — the influential London think tank known as Chatham House — published the first of three reports that would destroy the case for the gold standard.

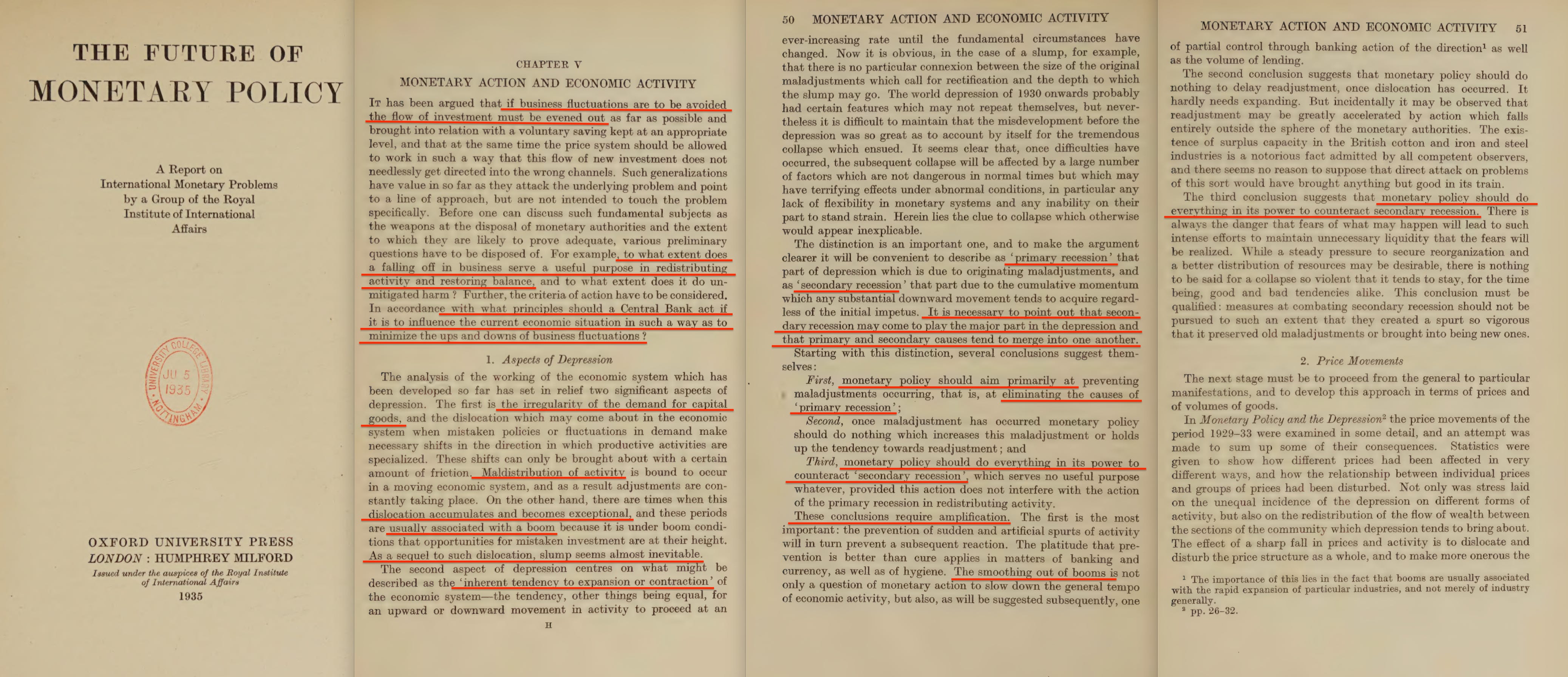

The International Gold Problem6 (1931) argued that tying currencies to gold stopped governments from responding to economic crises. Monetary Policy and the Depression (1933) said governments needed to coordinate their spending and money supply to fight downturns. The Future of Monetary Policy (1935) went further, calling for central banks to buy and sell government bonds to manage the economy directly — the technique now known as quantitative easing.

By 1936, the intellectual groundwork was complete. Keynes published The General Theory of Employment, Interest and Money7, pulling these arguments together: markets do not fix themselves, governments must manage demand, and monetary and fiscal policy must work together. But the Chatham House reports had already made every one of these arguments in separate pieces. What Keynes provided was political cover for state intervention in the economy.

There was a consequence built into this framework that is rarely discussed. By making government spending a tool for managing the economy, Keynes made governments permanently dependent on central banks. A government cannot spend its way out of a recession unless the central bank is willing to absorb the debt — by buying bonds, keeping interest rates low, or printing money. The politician proposes; the central banker disposes.

Each crisis deepens the dependency, because each round of spending needs the central bank to keep borrowing affordable. The framework gave elected governments a new lever of control over the economy, but it gave unelected central bankers a new lever of control over the government.

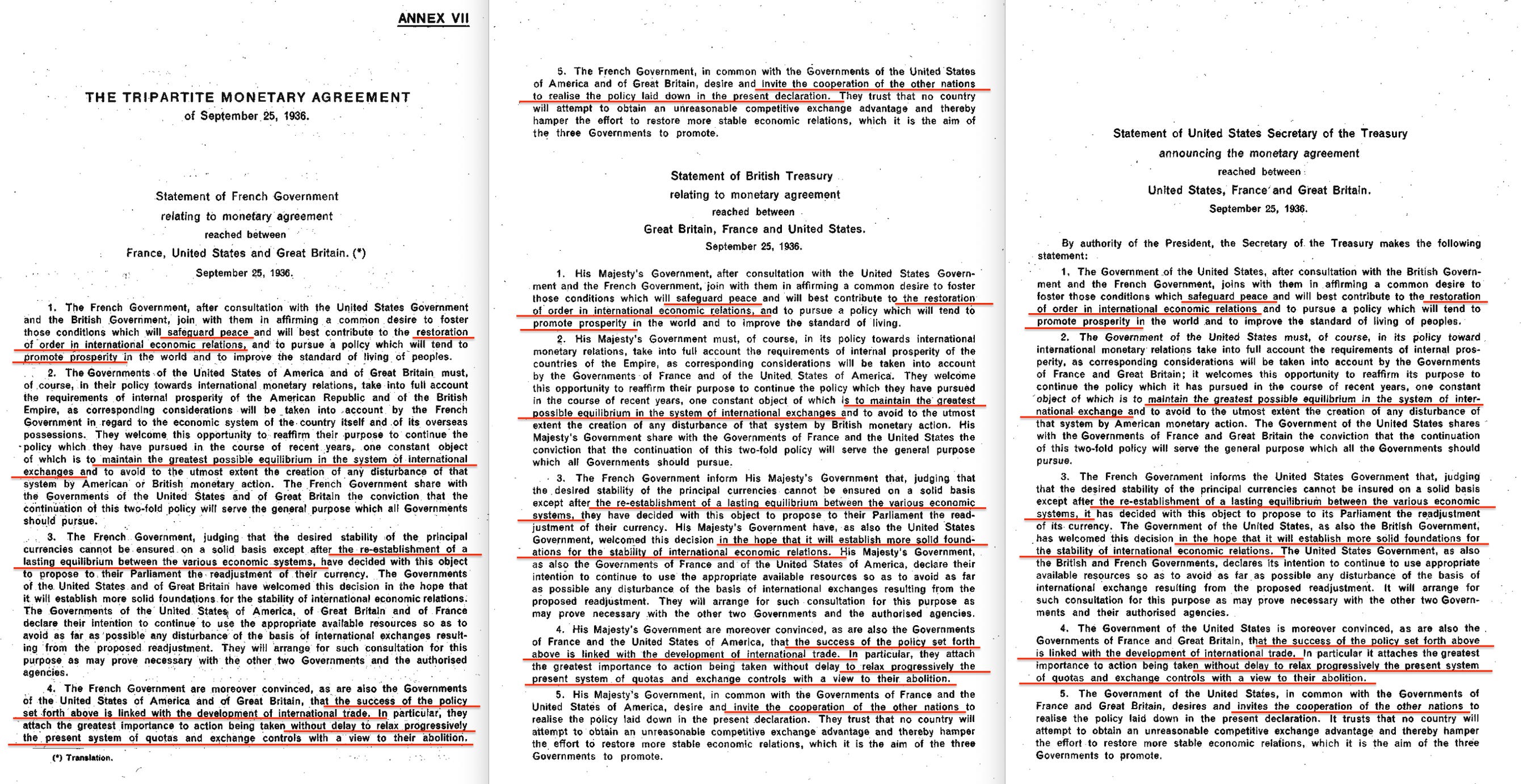

That same year, the United States, Britain, and France signed the Tripartite Agreement — the first arrangement in which major economies agreed to coordinate their currencies. It was modest — parallel statements rather than a formal treaty — but Belgium, the Netherlands, and Switzerland soon joined.

The declarations, however, went well beyond currency. Point 4 of all three statements declared that currency stability was ‘linked with the development of international trade’ and that the three governments would work ‘without delay to relax progressively the present system of quotas and exchange controls with a view to their abolition’.

Currency stabilisation, trade liberalisation, elimination of quotas, and abolition of exchange controls — the entire programme that would later define the postwar economic order — were all stated in a single document in September 1936.

The official account of the agreement was published in 1937 by the BIS’s own economics department. The institution that would shortly be proposed as the manager of the entire system was already writing the record that justified its expansion.

The BIS’s Seventh Annual Report8, dated May 1937, went further. It diagnosed the same six problems Van Zeeland would address ten months later — agricultural collapse, gold market tension, currency misalignment, high interest rates, debt burden, and tariff barriers. And it presented the BIS itself as the natural authority overseeing the international monetary system.

The institution defined the problem, documented the first solution, and positioned itself as the answer — before Van Zeeland had even been asked to start work.

There is a structural detail here that is rarely mentioned. Britain had left the gold standard in 1931. France finally devalued on the same day the agreement was signed. But the United States had not left gold entirely — Roosevelt had confiscated domestic gold and devalued the dollar in 1933-34, but foreign central banks could still swap dollars for gold at $35 per ounce. So when Britain and France in 1936 agreed to stabilise their currencies against the dollar, they were effectively re-anchoring to gold — but indirectly, through America rather than on their own terms.

The Chatham House reports had argued for leaving gold. Leaving gold created instability. The Tripartite Agreement fixed the instability. But the fix replaced a system where each country had its own gold anchor with one where everyone went through a single currency that still had the anchor to gold. That is the Bretton Woods structure eight years early — the dollar pegged to gold, everyone else pegged to the dollar — and it was the BIS that documented it.

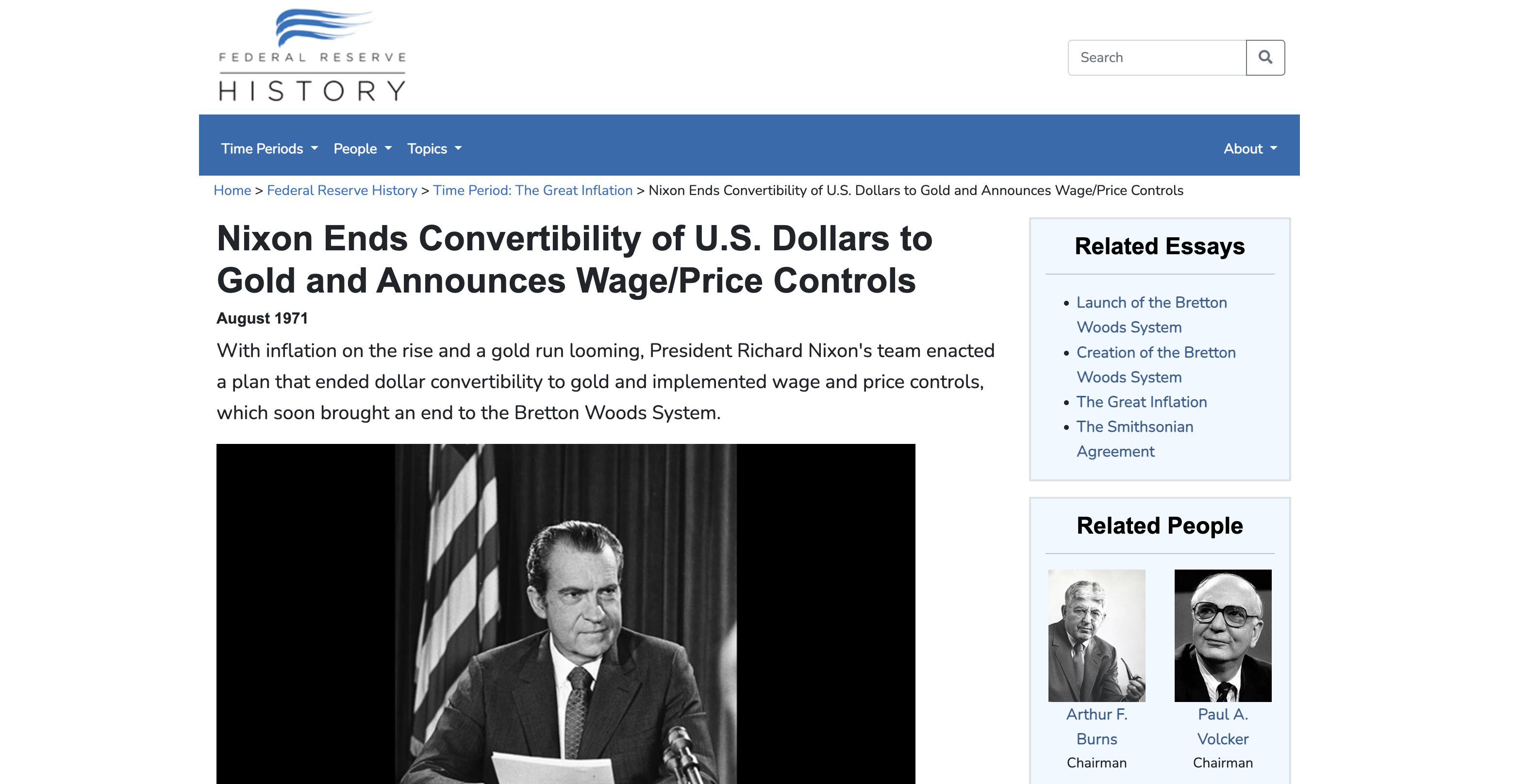

This had a consequence that shaped everything that followed. Before the Tripartite Agreement, moving the world off gold would have meant persuading every nation separately. After it — and after Bretton Woods formalised the same structure — every nation’s link to gold ran through a single point: the dollar. When Nixon closed the gold window in August 19719, one decision by one president floated every currency on earth at once. You could not float the world in one move until you had first routed the world through one node.

The centralisation of the anchor was what made its removal possible. And once the anchor was gone, the middleman did not disappear. It simply became less visible, operating through institutional trust, central bank coordination, and the BIS-managed standards that replaced the metal.

The same principle was later applied to securities: physical stock certificates migrated to central depositories, leaving holders with book entries whose validity depends on the clearing node honouring them — Wolf's 1892 template of replacing tangible assets with receipts held at a central node, applied to ownership itself.

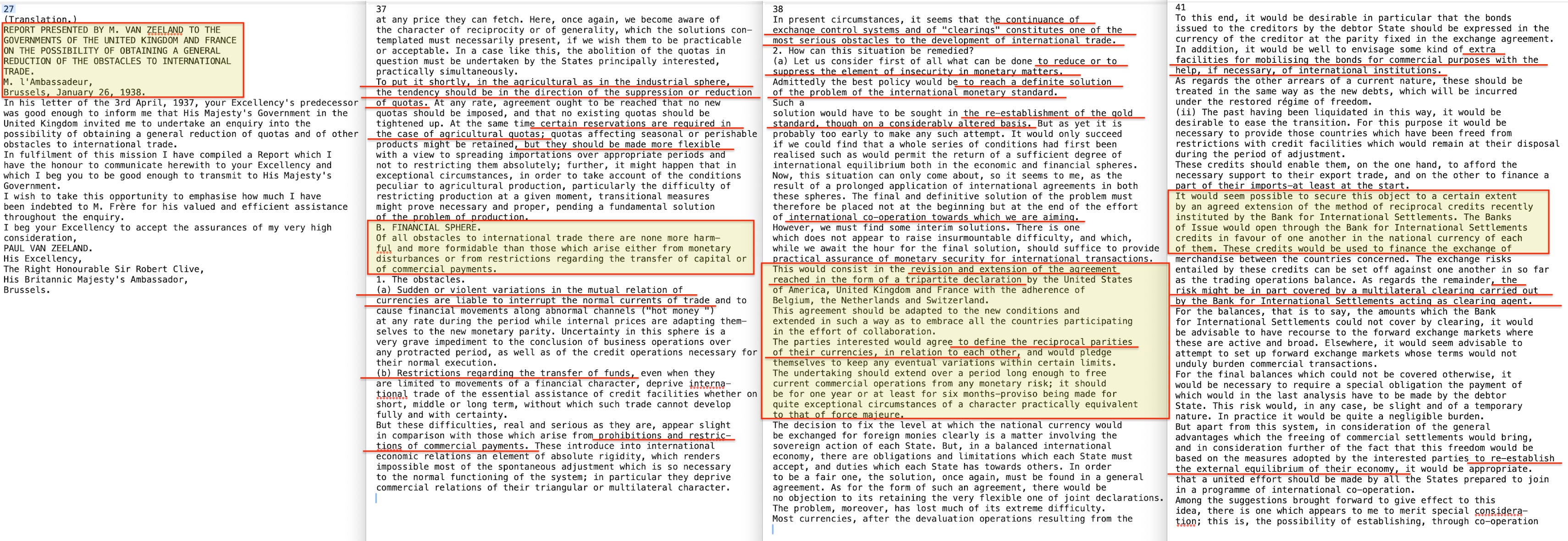

In April 1937, Britain and France asked Paul van Zeeland, the former Belgian Prime Minister, to work out the practical details of the programme the Tripartite declarations had announced — specifically, how to reduce the barriers choking international trade. The request came after the 1933 World Economic Conference in London10 had ended in complete failure, collapsing over currency and tariff disagreements. Van Zeeland submitted his report on 26 January 19381112. It deserves far more attention than it has received — not least because of who was involved in drafting it.

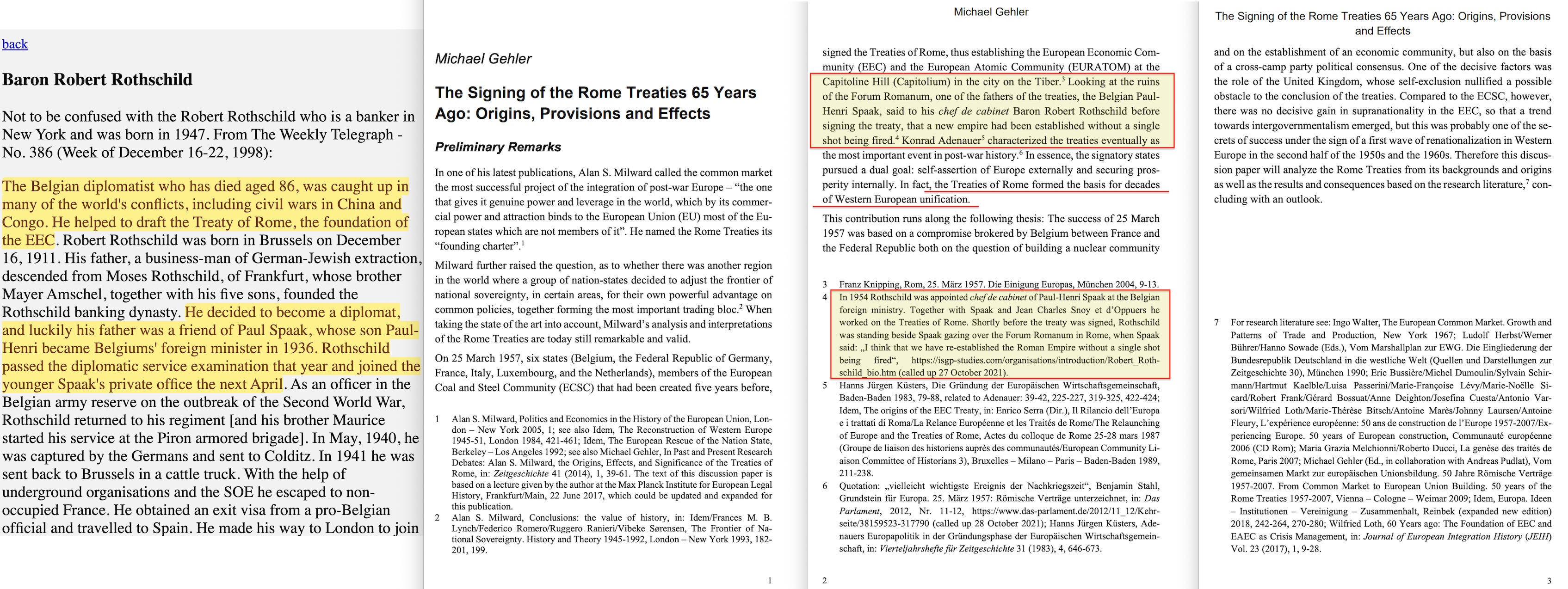

Robert Rothschild, a Belgian diplomat and member of the banking family, joined the private office of Foreign Minister Paul-Henri Spaak in April 193713 — the same month Spaak’s government commissioned Van Zeeland’s mission. Twenty years later, the same Robert Rothschild would help draft the Treaty of Rome, the founding document of what became the European Union14.

The same family at both ends of the chain.

Van Zeeland began by ruling out the idea that any country could wall itself off from the global economy and survive. No nation, he argued, however large, could do this without devastating its own people. The crisis years had proved it.

He then worked through the main obstacles to trade and proposed fixes for each.

On tariffs, he called for an immediate freeze on new duties and a gradual reduction of the highest ones. On hidden protectionism — governments abusing health regulations, imposing absurdly detailed product rules, or inventing anti-dumping measures to block imports — he proposed joint committees and arbitration panels to settle disputes. On quotas, he called for abolishing industrial quotas outright and steadily reducing agricultural ones.

None of this was new. The idea of expert committees settling disagreements between countries had been laid out twenty years earlier by Leonard Woolf in International Government15 (1916), a report published by the Fabian Society. Woolf argued that international economic life had become too complicated for any single government to manage alone. What was needed, he said, were groups of experts operating across borders, outside the control of any single parliament — specialists resolving disputes, international offices running agreements, shared rules emerging through cooperation rather than democratic votes.

International Government became the blueprint of the League of Nations. Van Zeeland was applying Woolf’s template to the specific problem of trade barriers, right down to proposing that arbitration should be handled by bodies already established under the League.

But Woolf realised something else. If you remove tariffs between countries and let people move freely across borders, the countries will eventually be forced to align their economic policies — because any difference in regulation creates an advantage that trade and migration will exploit until the difference disappears.

You don’t need laws forcing countries to harmonise. It happens on its own once the barriers come down. The expert panels and the trade liberalisation were not separate projects but two routes to the same destination: policy convergence without democratic legislation. One worked through institutions, the other through economic pressure. The Tripartite Agreement’s call for abolishing quotas and exchange controls was Woolf’s logic put into practice — and the progressive alignment of trade policy that followed, from GATT through the Common Market to EU regulatory harmonisation to neoliberalism in the 90s, is the same programme still running today.

Woolf and Keynes were not merely working in parallel. Both were members of the Cambridge Apostles, an elite and secretive intellectual society whose past members included Bertrand Russell and EM Forster — and, later, the Soviet spies Anthony Blunt and Guy Burgess. By the 1930s, according to MI5, nearly all the Apostles’ active members were communists16.

Victor Rothschild was a member during this period, and his London flat at 5 Bentinck Street served during the war as a shared home for Blunt and Burgess while both worked in British intelligence. The society produced the Cambridge Five — five confirmed Soviet agents. Keynes had dominated the Apostles for years, controlling recruitment. Woolf was a longstanding member. The man who designed the governance template and the man who designed the economic framework both came out of the same small room in Cambridge.

JD Bernal, a regular at Rothschild’s flat, proposed an International Resources Office at the 1941 Science and World Order conference — an initiative that developed into the International Union for Conservation of Nature (IUCN).

The financial sections of the report mattered even more. Van Zeeland saw currency instability and restrictions on moving money across borders as the biggest obstacles to trade.

His solution was to build on the Tripartite Agreement by committing countries to fixed exchange rate bands for at least six months at a time. The BIS would run a credit system between central banks — acting as a middleman settling trade payments between countries. For countries coming out of exchange controls, a common fund — again run by the BIS — would provide emergency credit to ease the transition.

He then laid out a step-by-step process: first, private talks among the major economic powers (France, Britain, the United States, Germany, and Italy); then a bureau to gather and organise proposals from all participating countries; and finally a diplomatic conference to sign the agreements.

Now compare this with what actually happened between 1944 and 1947.

The tariff freeze and gradual reduction became the General Agreement on Tariffs and Trade (GATT; 1947)17.

The fixed but adjustable exchange rates became the Bretton Woods currency system (1944)18.

The common fund for countries in transition became the International Monetary Fund19.

Long-term development lending became the World Bank20.

The procedural sequence — great power talks first, then wider preparation, then a conference — is almost exactly what took place. And it was written in a document published on the eve of the Second World War.

These parallels are not coincidental. French planners in wartime exile explicitly revived Van Zeeland’s framework. The 1943 Alphand-Istel plan2122, circulated among Allied governments, proposed payments agreements inspired by those of the 1936 Tripartite Agreement and by those presented in the report by Paul van Zeeland (1938). The wartime negotiators were not arriving at similar conclusions independently. They were working from his report.

Taken together, the postwar institutions form a set of clearing functions covering every dimension of economic life.

The BIS coordinates monetary policy between central banks.

The IMF provides short-term emergency lending, with conditions that force borrowing countries to change their fiscal policies.

The World Bank provides long-term development lending, with conditions that force borrowing countries to restructure their economies.

The GATT removes trade barriers and lets competitive pressure align regulations automatically — exactly as Woolf predicted.

All four were specified in Van Zeeland’s 1938 report.

And Robert Rothschild — who was in the Belgian Foreign Minister’s office when that report was commissioned — went on to help draft the Treaty of Rome in 1957 — which applied the same template to Europe but took it further. Economic harmonisation became political harmonisation: a common commission, a common court, a common parliament, and eventually a common currency, all operating above national democratic control.

The economic institutions were not working alone. The International Council of Scientific Unions (1931) was harmonising science across borders. The Grotius Society had been working on legal harmonisation since 191523. The Carnegie Endowment for International Peace had been working on peace since 1910.

Every domain was being run through the same ‘expert’-led model at the same time.

Van Zeeland’s report was not the only pre-war blueprint. In 1939, the Bruce Committee24 proposed reorganising the League of Nations around a central committee for economic and social affairs — and that design became the template for the UN’s Economic and Social Council.

The League’s team of economists relocated to Princeton during the war and kept working — not just preserving archives, but actively planning the postwar order under four headings: reconstruction and relief, trade and trade policy, economic security, and demographic questions. These mapped directly onto what was built: UNRRA for relief, GATT for trade, the IMF and World Bank for economic security, and the population programmes that would run through the UN system for decades, commonly funded by Rockefeller — who also donated the land for the UN headquarters in New York25.

Ragnar Nurkse’s International Currency Experience26 (1944) made the historical case for Bretton Woods monetary arrangements using a decade of League research. The League’s own wartime report27 on the handover to the United Nations stated plainly that the new Economic and Social Council was ‘based directly on the League’s experience’ and ‘similar to the Central Committee projected by the League in 1939/40’.

Staff, archives, buildings, the library, and decades of knowledge passed from the League to the United Nations more or less intact.

The Rockefeller Foundation paid for the Princeton operation. League officials helped draft the implementation of the Atlantic Charter.

Laid out in order, the chain of documents reads like a construction schedule.

Wolf’s gold clearing mechanism (1892) gave the BIS its operating model when it was founded in 1930.

The Chatham House reports (1931, 1933, 1935) dismantled the gold standard and introduced the tools of central bank management.

Keynes (1936) wrapped these ideas in a political framework.

The Tripartite Agreement (1936) put managed currency cooperation into practice, indirectly anchored to gold.

Van Zeeland’s report (1938) combined the monetary and trade programmes into a single blueprint, named the BIS as the managing body, and laid out the diplomatic steps to get there.

The Bruce Report (1939) supplied the design for the UN’s economic and social machinery.

Nurkse’s International Currency Experience (1944) provided the evidence base.

Bretton Woods and GATT (1944, 1947) carried it out.

The United Nations (1945) preserved most aspects of the League of Nations — staff, archives, intellectual heritage, and institutional design — with the Bruce Committee’s central committee becoming ECOSOC.

Each document in this chain builds on the ones before it. Van Zeeland cites the Tripartite Agreement as his starting point. The Bruce Committee drew on the League’s existing structures. Nurkse used a decade of League research.

The Bretton Woods negotiators worked within the framework these earlier documents had already established.

The postwar settlement did not require new ideas. It required the political will to act on old ones. The designs were ready, the blueprints drawn up, the steps mapped out. What was missing in 1938 was the willingness to move — governments accepted the case for cooperation but would not commit, retreating into what Van Zeeland called ‘very great reserve’ whenever practical steps were proposed.

The war changed that. It discredited economic nationalism. It concentrated power among a small group of allied governments. It produced populations willing to accept change. And it removed from the table the countries — Germany and Italy — whose cooperation Van Zeeland had wanted but never received.

Van Zeeland’s 1938 framework assumed the great economic powers were roughly equal. What the war produced was American dominance — and with it, a willingness by the United States to underwrite the whole system with the dollar at its centre. The designs were European; the execution was American. The Americans even tried to shut down the BIS at Bretton Woods because of its wartime dealings with Nazi Germany. The Europeans refused28. The institution survived, and went on to become the central coordinating body for global monetary policy — exactly the role Van Zeeland had proposed for it in 1938.

The phrase ‘American priorities’, however, deserves a closer look. The two Americans who did most to shape the postwar institutions were both working for Soviet intelligence.

Harry Dexter White, the senior Treasury official who dominated the Bretton Woods conference and whose plans for the IMF and World Bank won out over Keynes’s, was a Soviet asset. Notes taken from KGB archives in the early 1990s29 — known as the Vassiliev notebooks — record White under multiple codenames including ‘Jurist’ and ‘Richard’. More than two dozen wartime KGB documents show the agency managing White between 1943 and 1945 through a spy network run by Nathan Gregory Silvermaster out of the Treasury Department. White was considered so valuable that when he thought of quitting government because he couldn’t afford his daughter’s university fees, his handlers offered to pay the tuition to keep him in place.

At the 1945 San Francisco conference that founded the United Nations, KGB officers got American negotiating positions directly from White, who handed them over willingly. Moscow concluded the results showed what ‘skilful guidance’ by Soviet agents could achieve.

Alger Hiss, a senior State Department official and one of the key Americans at the Dumbarton Oaks conference that designed the United Nations, was also a Soviet asset30. A bipartisan Senate commission chaired by Senator Daniel Patrick Moynihan, reporting in 1997, stated that his complicity appeared to be established31.

So the two founding conferences of the postwar order — Dumbarton Oaks for the UN and Bretton Woods for the financial system — both had Soviet agents among their principal American architects. The European designs passed through American hands, but at critical points those hands were reporting to Moscow.

Whether that changed specific outcomes matters less than the basic fact: the key positions were held, at the moment the system was being configured, by people Moscow considered valuable assets. And the British network that produced the designs — the Cambridge Apostles, the Fabian Society, Chatham House — was itself deeply penetrated by Soviet intelligence, with several of its most prominent members later confirmed as agents. Victor Rothschild was himself publicly accused of being a Soviet agent in the 1970s3233.

The standard story of these institutions emerging from open debate among free nations needs, at the very least, some qualification.

But the programme itself — the tariff framework, the monetary cooperation, the role of the BIS, the governance model of expert panels operating outside elected parliaments — had all been written before the first shot was fired.

The Tripartite Agreement had put currency stabilisation into practice in 1936.

Van Zeeland had laid out the full institutional architecture in 1938.

Keynes had provided the political justification, built on Chatham House research stretching back to 1931.

The Bretton Woods conference of 1944 did not design the postwar economic order. It gave American backing and new names to a system that had already been prepared, tested, and formally proposed to governments before the war began.

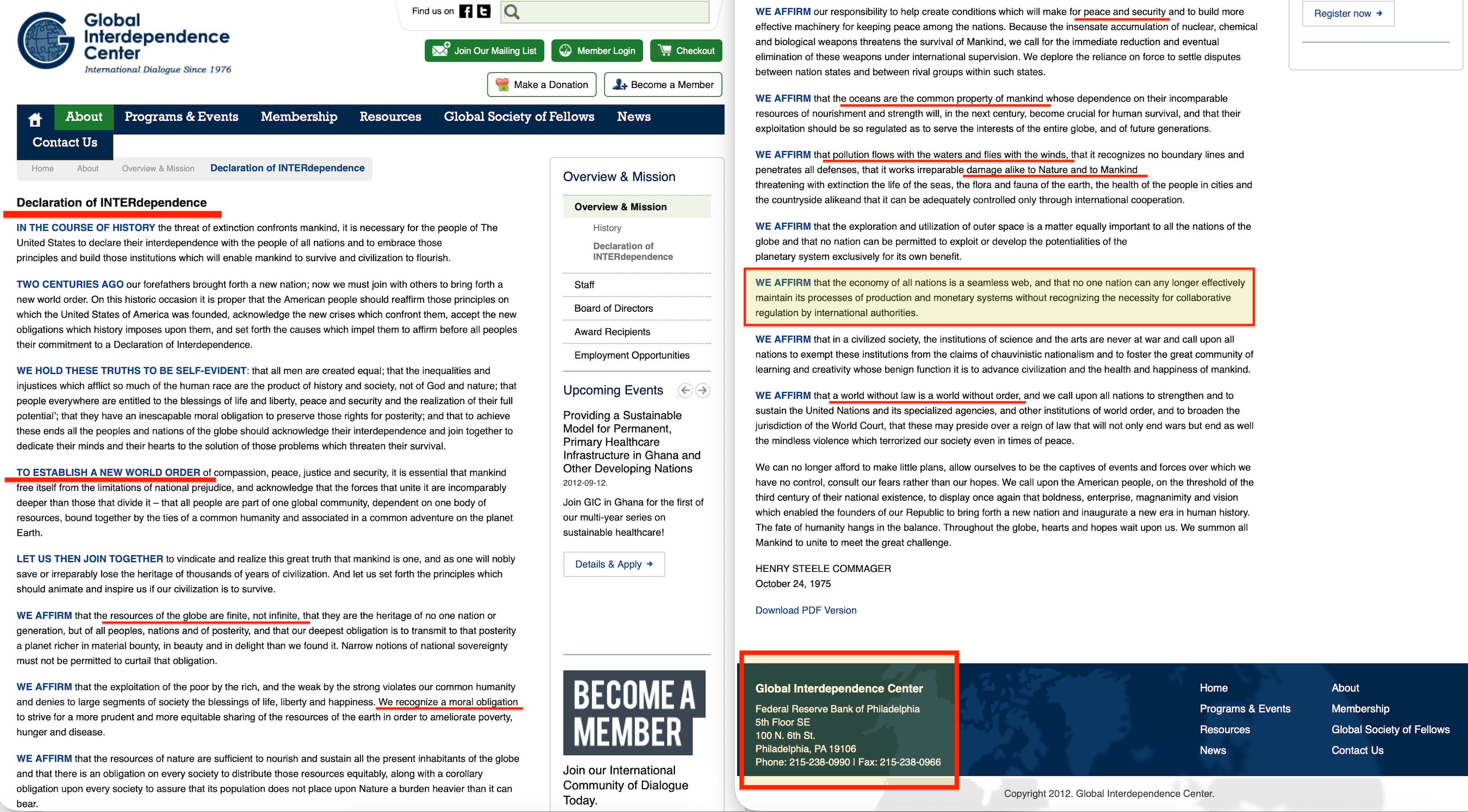

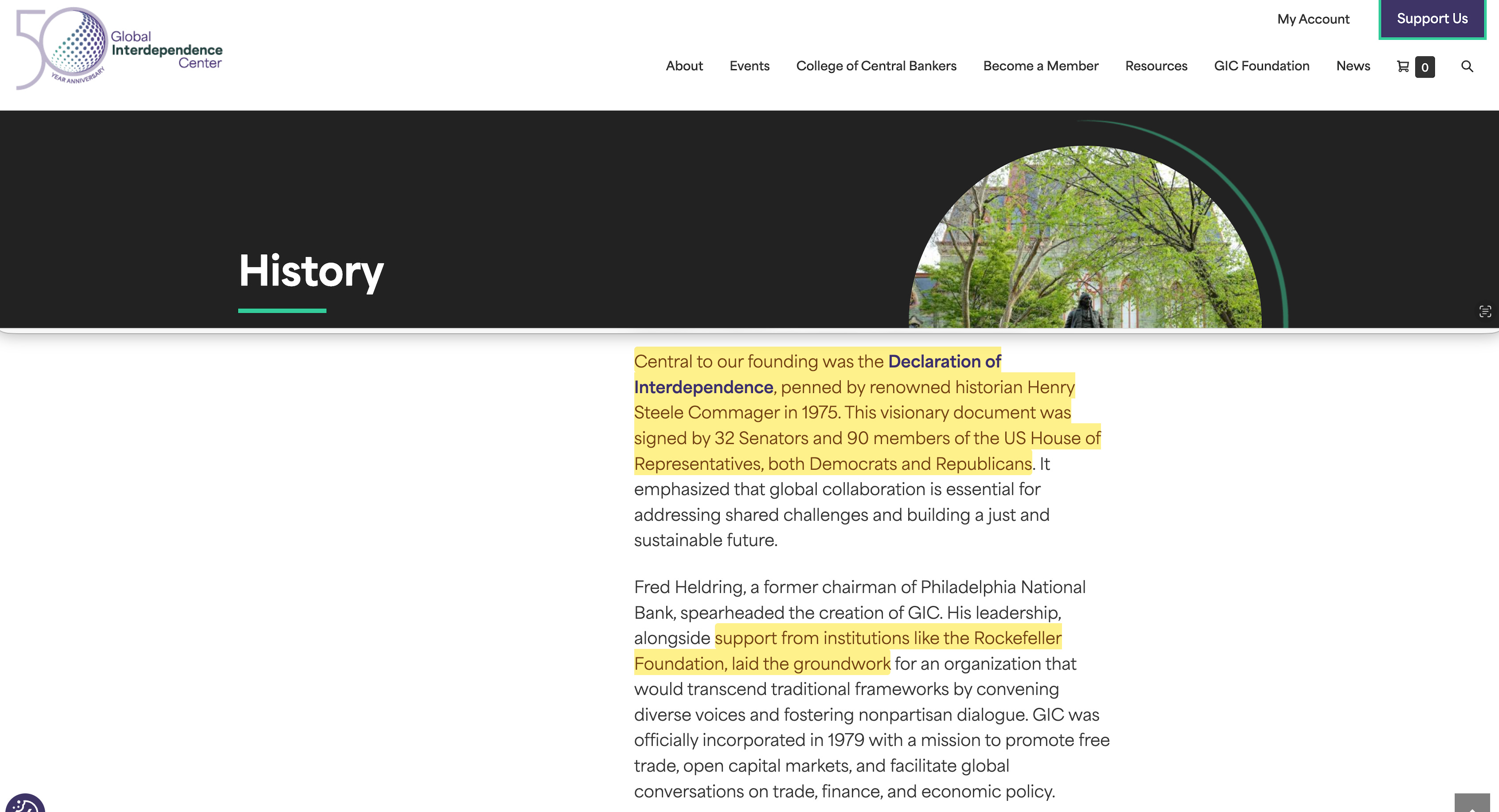

The programme did not stop there. In 1975, the historian Henry Steele Commager drafted a Declaration of Interdependence34 which put the same objectives into political language: ‘the economy of all nations is a seamless web, and no one nation can any longer effectively maintain its processes of production and monetary systems without recognising the necessity for collaborative regulation by international authorities’.

But the declaration went far beyond money. In just two pages it called for the erosion of national sovereignty (‘narrow notions of national sovereignty must not be permitted to curtail that obligation’), planetary resources managed through international coordination, population control, peace and security through ‘more effective machinery’, pollution controlled ‘only through international cooperation’, the strengthening of the United Nations and its agencies, the broadening of the World Court, and the exemption of science from national control. Monetary policy, environment, population, peace, science, international law, resources, and sovereignty — every domain now subject to international coordination — assembled in one declaration, calling openly for ‘a new world order’.

It was signed by 32 senators and 90 members of the House of Representatives. The organisation created to carry it forward — the Global Interdependence Center, whose own history describes its founding as reflecting on ‘the new world order’ — was funded by the Rockefeller Foundation, the same foundation that paid for the League’s wartime operation at Princeton35.

The Global Interdependence Center is headquartered inside the Federal Reserve Bank of Philadelphia and today runs a College of Central Bankers. The programme that began with Wolf’s clearing mechanism in 1892, was formalised by the BIS in 1930, tested through the Tripartite Agreement in 1936, detailed by Van Zeeland in 1938, and implemented at Bretton Woods in 1944, was by 1975 openly calling for a new world order and global monetary policy from inside the Federal Reserve itself — same backers, same language, same logic.

Julius Wolf was not just a monetary economist. He edited the Zeitschrift für Socialwissenschaft36 — a journal of social science — writing on social policy alongside his work on clearing mechanisms and trade. The monetary programme was never separate from the social one. It belonged to a tradition stretching back to the father of communism, Moses Hess37, in the 1840s, which understood monetary reform as a vehicle for social transformation — reform how exchange works and you reform the social relations that flow through it. Wolf turned that idea into a mechanism. Eduard Bernstein gave it an ethical framework. The BIS gave it an institution. Woolf and Zimmern built it into the League of Nations, later the United Nations.

The programme that runs from Van Zeeland through Bretton Woods to Lynn Forester de Rothschild’s Council for Inclusive Capitalism still carries the same premise: whoever turns social ethics into (cognitive) standards the (evaluative) clearing function checks against controls the social order.

And that mechanism will soon be integrated into central bank digital currencies, refusing to settle your transaction should you not abide the social ethic.

The war provided the political conditions. The plans — and the clearing function that tied them together — were already there.

The programme is still being developed. Over two decades of work, the economist Thomas Piketty has drafted blueprints for a system of total financial visibility — a global registry of who owns what, wealth and inheritance taxes coordinated across borders, central bank accounts for every citizen, and individual carbon cards. Half the planks of the Communist Manifesto, restated as mainstream economics, with the surveillance architecture to enforce them.

Meanwhile, the same Van Zeeland method — build the financial architecture first, attach governance conditions, let the politics follow — is being applied right now across three active wars by Jared Kushner and Steve Witkoff, two real estate developers negotiating the reconstruction of Ukraine, the governance of Gaza, and the terms under which Iran re-enters the international system. The blueprint is not historical — it is operational.

If the fifth plank of the Communist Manifesto called for the centralisation of credit in the hands of the state through a national bank with an exclusive monopoly — and if that centralisation has now been achieved through central bank coordination, international standard-setting, and compliance-based clearing — then what, exactly, was the revolution for?

JM Keynes was an economic fraudster, a Commie paedophile with a penchant for young boys in North Africa.

Absolutely brilliant! You are rewriting history!