The Innovation Hub

Between 2019 and 2026, the Bank for International Settlements developed a suite of interlocking projects that together form a planetary financial control system.

The components are designed separately and presented as technical experiments. But when viewed as a whole, they establish a system that can monitor every physical asset on earth, classify it according to official criteria, adjust its cost of capital accordingly, and ultimately determine whether related transactions are even allowed.

The System Described by Insiders

The characterisation of these projects as components of a larger system is not inference. The General Manager of the BIS has stated it repeatedly.

In February 2023, Agustín Carstens delivered a keynote at the Monetary Authority of Singapore in which he described the individual Innovation Hub projects and added: ‘But to fully realise the transformative potential of these new financial technologies, we need some way to bring them all together’1.

He proposed a unified programmable ledger with a common programming environment as the integrating infrastructure, with the central bank governing its operation.

In May 2024, opening the BIS Innovation Summit in Basel, Carstens told the audience that individual experiments should ‘always have in mind the larger purpose — the giant leap we hope to achieve. That is exactly what we do here at the BIS Innovation Hub’2.

In August 2024, speaking to the Reserve Bank of India, he was more explicit3: ‘To realise that vision, we need to deploy novel technologies — including tokenised assets, unified ledgers and fast payment systems — in an integrated way’.

In October 2024, at the Santander International Banking Conference in Madrid, Carstens identified what had been missing4: ‘What has been lacking is a vision of how the various initiatives should fit together, and of what the financial system of the future should look like and how it should function’.

He and Nandan Nilekani (Infosys) supplied that vision in an April 2024 paper: the ‘Finternet’, a concept of multiple financial ecosystems interconnected through unified ledgers, with compliance and governance features embedded directly into the technology.

The BIS published the 44 page blueprint as a working paper5.

In September 2024, his deputy Cecilia Skingsley confirmed the connection to the existing project portfolio: ‘It is possible to sketch many elements of the Finternet from the project portfolio of the BIS Innovation Hub, with experiments we have done on fraud and crime detection, cyber security, automated compliance controls and liquidity optimisation’.

By June 2025, the BIS was explicit6: ‘The BIS is not just theorising, it is working with central banks to test and develop tokenisation as the backbone of the future monetary and financial system’.

The characterisation is not inference. The components were designed with integration as the stated objective, described publicly as elements of a single vision, and developed iteratively toward a common destination.

The Innovation Hub

The BIS Innovation Hub was established in 20197, one year after the final Stranded Assets Forum at Waddesdon Manor. Its stated purpose is to ‘foster international collaboration on innovative financial technology within the central banking community‘.

The Hub operates centres in Switzerland, Hong Kong, Singapore, London, Stockholm, Toronto, and other financial capitals. Each centre develops projects addressing specific technical challenges: cross-border payments, regulatory compliance, climate risk assessment, digital currencies.

The projects share common characteristics. They build on shared infrastructure — the unified ledger architecture described in the BIS’s 2023 blueprint8 and the ISO 20022 messaging standard9 that governs financial data exchange. They are modular, designed for interoperability, rely heavily on artificial intelligence and machine learning, and operate at scales that would be impossible for human administrators. And they connect central bank authority directly to individual transactions.

I. The Directive Layer

Every control system begins with an objective — the state it seeks to achieve.

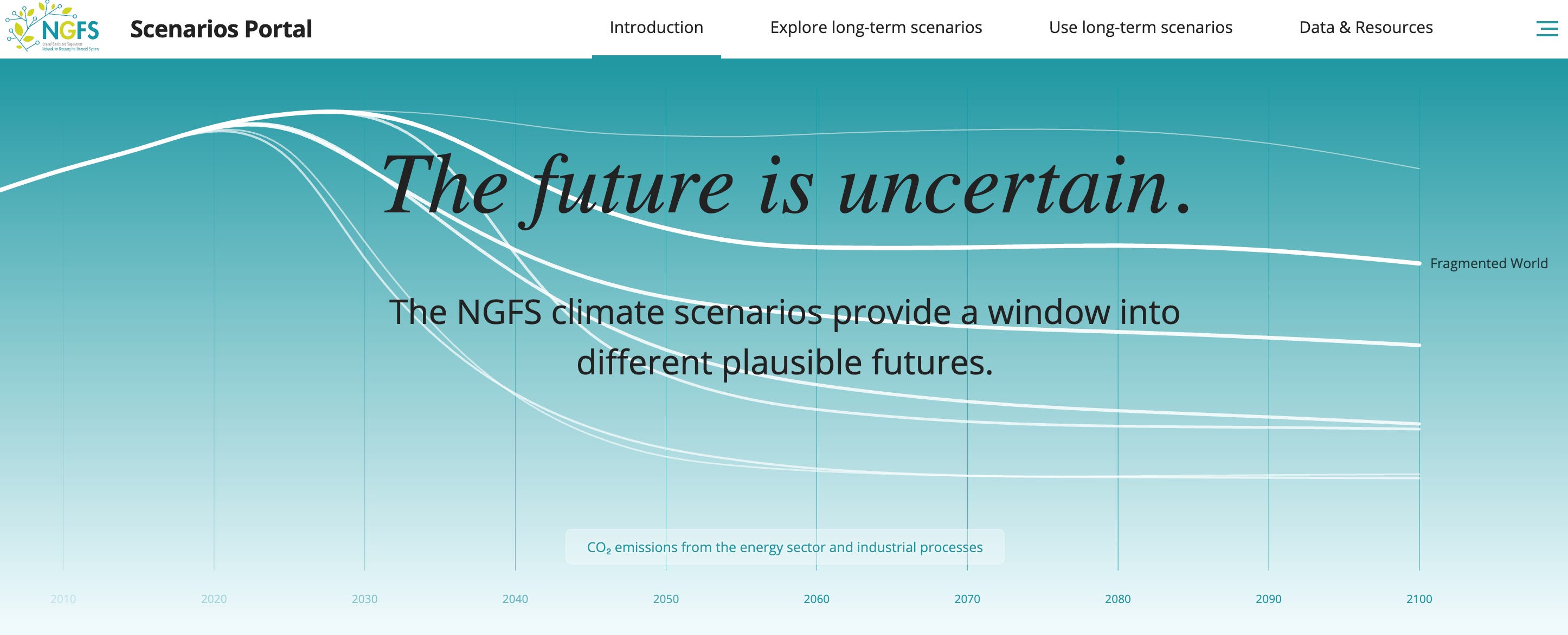

For the BIS architecture, the directives arrive through the Network for Greening the Financial System. Founded in December 2017 — at Emmanuel Macron’s One Planet Summit — the NGFS now comprises over one hundred central banks and financial supervisors representing approximately eighty-five per cent of global greenhouse gas emissions10.

The NGFS produces scenarios11. These are not forecasts but ‘plausible futures’ against which financial institutions must stress-test their portfolios. The scenarios specify pathways: orderly transition, disorderly transition, ‘hot house world’12. Each pathway assigns different values to carbon-intensive assets at different time horizons.

The scenarios originate from the IIASA-Potsdam consortium13 — the International Institute for Applied Systems Analysis and the Potsdam Institute for Climate Impact Research. The ‘black box’ integrated assessment models that generate these scenarios are proprietary, and their assumptions are not subject to democratic review.

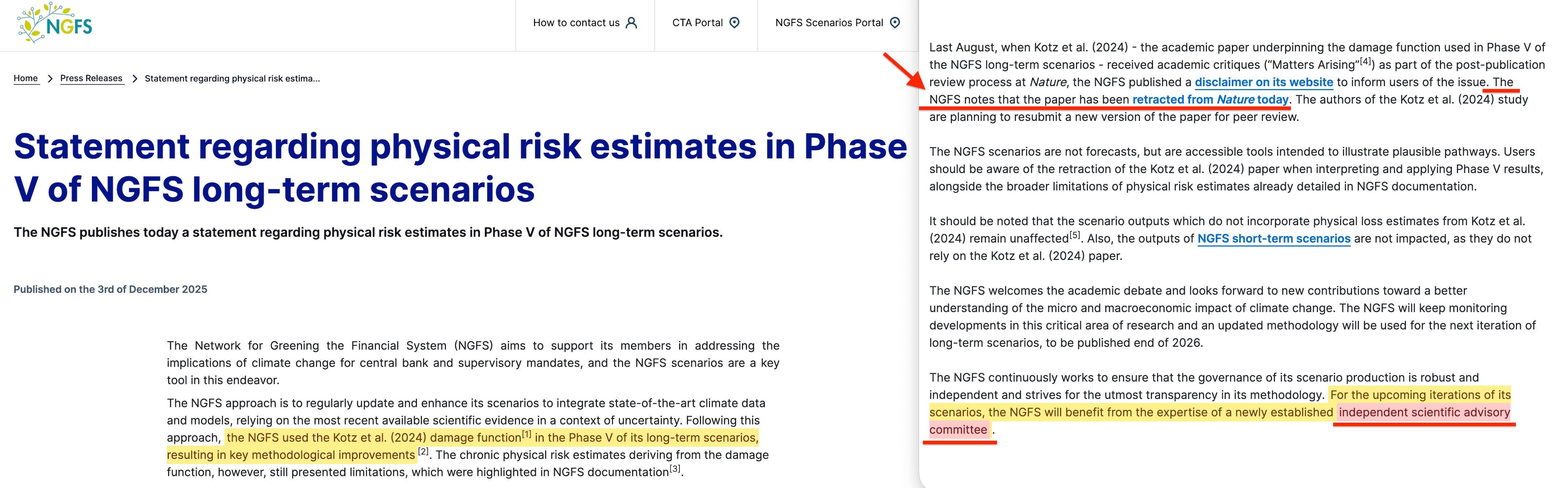

In December 2025, Nature retracted a paper by Maximilian Kotz14 that underpins the NGFS Phase V scenarios. The paper projected catastrophic economic damage from climate change based on data that included a major spreadsheet error. When corrected, the damage estimates fell by nearly two-thirds.

The NGFS response was to advise users to ‘be aware of the retraction when interpreting and applying Phase V results’15. Yet the scenarios continued operating, and the capital requirements remained calibrated to the erroneous estimates.

The same day the retraction was announced, the NGFS revealed it would establish a Scientific Advisory Committee (SAC) to oversee future scenario production. No membership has been published. No terms of reference have been released. The body that will direct the scenarios that pre-emptively strand assets through capital starvation has no public accountability.

No other action was taken. Consequently, it’s fair to say that the directive does not require accuracy. It just requires numbers for the system to process.

II. The Classification Layer

Once the directive enters the system, it must be translated into operational categories. This is the function of the classification layer.

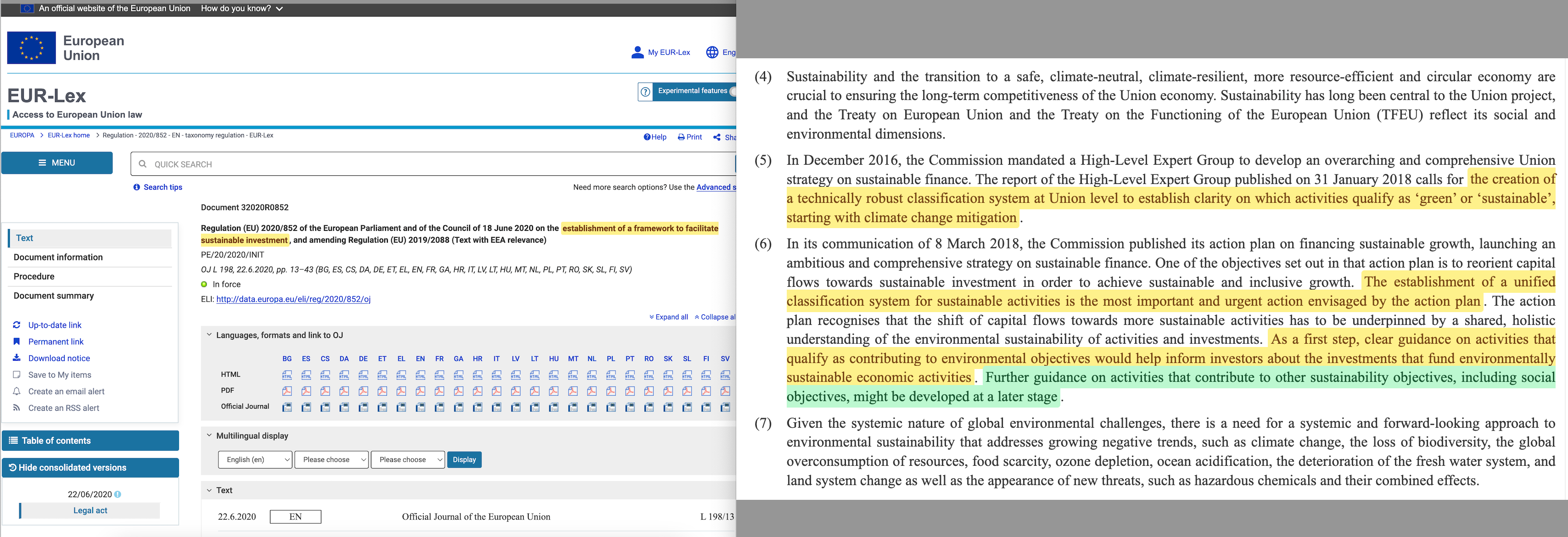

The EU Taxonomy Regulation of 202016 provides the master framework. The regulation establishes binding criteria determining which economic activities qualify as ‘environmentally sustainable’. Article 26 notes that guidance on activities contributing to ‘other sustainability objectives, including social objectives, might be developed at a later stage’.

The Taxonomy answers a binary question: is this activity compliant or non-compliant — is it ‘green’ or ‘brown’? The answer to that question determines eligibility for preferential capital treatment, such as access to green financing, and inclusion in sustainability indices.

The Task Force on Climate-related Financial Disclosures, launched in December 2015 and chaired by Mark Carney, established the disclosure framework17. Companies must report their climate-related risks according to standardised categories: governance, strategy, risk management, metrics and targets.

The International Sustainability Standards Board, established in 2021 under the IFRS Foundation, globalised these requirements18. The Transition Plan Taskforce, launched by HM Treasury in 2022, went even further — requiring companies not merely to disclose risks but to produce government-approved plans explaining how they will change their business models19.

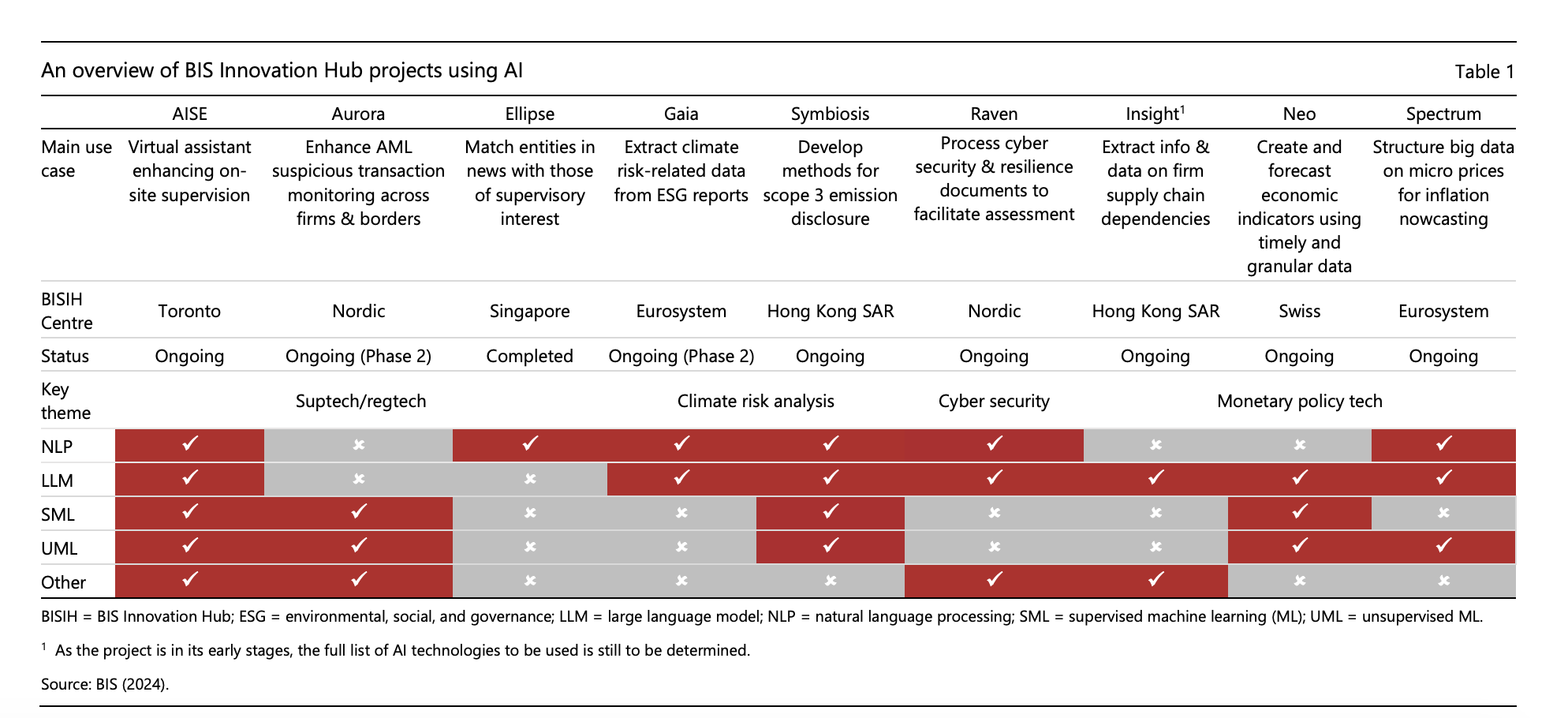

Classification at this scale requires automation. Manual review of thousands of corporate reports is impossible. The BIS addressed this with Project Gaia.

Project Gaia

Developed with the Bank of Spain, Deutsche Bundesbank, and European Central Bank, Project Gaia deploys large language models to scan corporate disclosures and extract climate indicators automatically20. The system identifies whether net-zero commitments match operational reality, flagging discrepancies between stated emissions and observable data without human review.

ECB President Christine Lagarde described the capability21:

Project Gaia makes assessing climate risk more transparent and efficient, as it uses generative AI to decipher vast unstructured data sets. If realised, Gaia has the potential to be a powerful tool for central banks in their comprehensive approach to assessing economic reality and risks

The output is classification: compliant or non-compliant. The label is attached to the entity and propagated through the system.

Viridis and the EDKP

Project Viridis22 serves as the distribution mechanism. Built on the Ellipse Data and Knowledge Platform23, it integrates regulatory data with external climate data and distributes the resulting risk assessments to fifteen or more participating central banks and supervisors.

Viridis generates heat maps showing supervisors which specific institutions hold excessive exposure to transition risk. The classification made by Gaia in Frankfurt can trigger supervisory attention in Singapore within hours.

III. The Surveillance Layer

The challenge identified at the Stranded Assets Forums was that voluntary corporate disclosure was insufficient. Companies reported what flattered them, omitted what did not, and used inconsistent methodologies.

The solution was to build automated monitoring independent of corporate cooperation.

Climate TRACE

Climate TRACE launched in September 202024, co-founded by former Vice President Al Gore. The name stands for Tracking Real-Time Atmospheric Carbon Emissions. The coalition uses over three hundred satellites, more than thirty thousand ground-based sensors, and machine learning algorithms to estimate facility-level emissions worldwide25.

By 2024, Climate TRACE had catalogued over 352 million individual emissions sources26. The system does not request data from companies — it observes them from space and infers their emissions from heat signatures, light patterns, and operational characteristics.

In November 2022, Al Gore presented Climate TRACE data at COP27 showing that oil and gas industry emissions were ‘three times higher than they have been telling the United Nations’27. The discrepancy arose because Climate TRACE was substituting its own satellite-derived measurements for industry self-reports28.

Gore described the system as ’a massively distributed body cam for the planet’29.

But who audits the auditors, and what’s the penalty when they’re wrong?

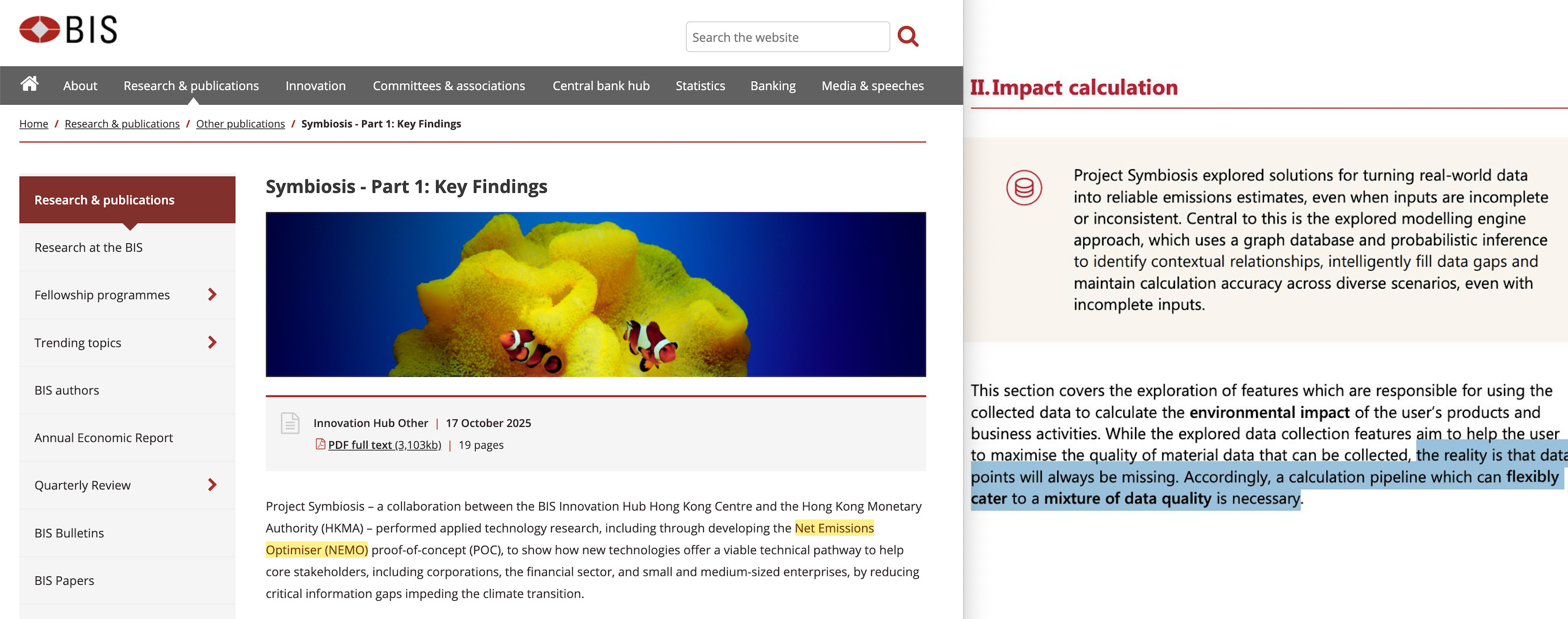

Project Symbiosis

Satellite observation addresses large industrial facilities. It does not reach the millions of small and medium enterprises that constitute the bulk of global supply chains. These entities lack the resources to measure their emissions and have no regulatory obligation to report.

Project Symbiosis30, developed by the BIS Innovation Hub, addresses this gap. Its core component is NEMO — the Net Emissions Optimiser.

NEMO is an artificial intelligence engine that generates emissions figures for entities that have never reported. It combines sector classification, location data, and financial proxies to produce facility-level estimates. The BIS documentation states that NEMO ‘can model emissions even in data-scarce environments’31.

A bakery in Southeast Asia that has never measured its carbon footprint, has no sustainability department, and has never heard of the Task Force on Climate-related Financial Disclosures now has an AI-generated emissions profile attached to it in the financial system. That profile feeds into the supply chain risk assessments of any multinational buyer subject to European disclosure requirements.

The AI assigns synthetic numbers which control access to funding.

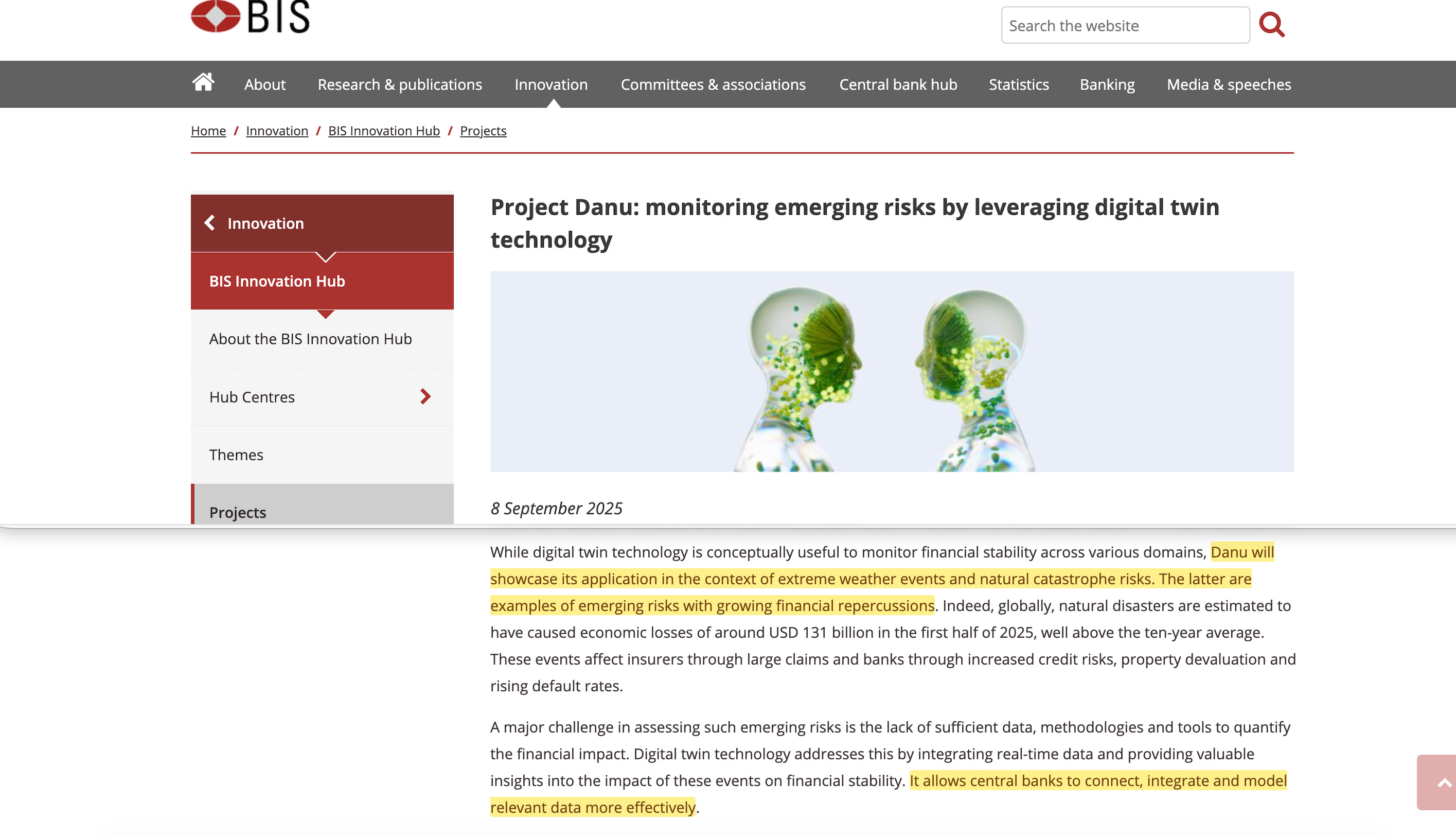

Project Danu

Project Danu, announced in September 2025, extends the surveillance architecture to physical and nature-related risks32. The project develops a ‘digital twin’ — a virtual model integrating climate data, geographic information, and financial exposure mapping.

The digital twin allows central banks to simulate scenarios in real time. A flood in Indonesia, a drought in Brazil, a wildfire in California — the model traces the impact through supply chains and financial networks to identify which portfolios are exposed.

The BIS states that Danu addresses ‘emerging risks with growing financial repercussions’ and enables central banks to ‘connect, integrate and model relevant data more effectively’.

Project Ellipse

Project Ellipse33 scrapes unstructured data — news reports, social media, sentiment indicators — to flag emerging risks before they appear in financial reports34. If a company faces criticism for environmental violations, Ellipse identifies the signal before markets react.

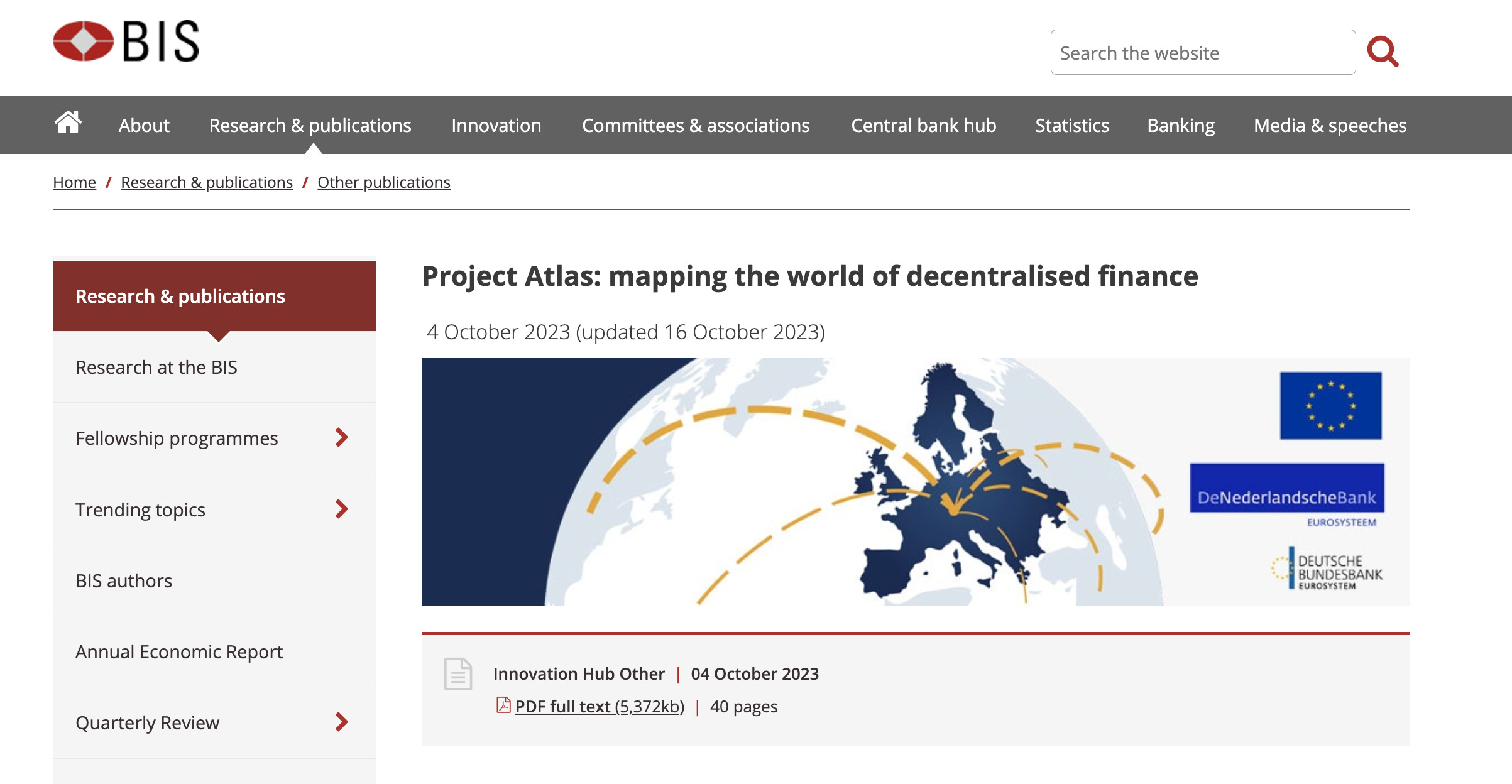

Project Atlas

While Basel 3.1 creates a capital barrier to cryptocurrency, Project Atlas creates a surveillance barrier35. Launched by the BIS Innovation Hub with the Deutsche Bundesbank and Dutch Central Bank, Atlas functions as a crypto intelligence platform.

The system fuses on-chain data — public ledger entries from blockchain networks — with off-chain data: exchange order books, trading flows, and institutional records. It maps capital movements across borders, identifying when funds flow between the regulated banking system and the cryptocurrency ecosystem.

The documentation describes this as ‘structural analysis’ of crypto markets. The function is de-anonymisation. Atlas tracks the money seeking exit from the regulated system, ensuring that even the alternative is mapped.

Project Pyxtrial

While Project Atlas watches the flows, Project Pyxtrial watches the backing36. Developed by the BIS Innovation Hub London Centre and the Bank of England, Pyxtrial creates a real-time data monitoring system for stablecoins.

Stablecoins — private digital dollars like USDT or USDC — represent the primary bridge between the crypto economy and the real economy. Most people seeking to exit the banking system do not want Bitcoin’s volatility. They want a digital dollar outside the bank, and that’s what stablecoins provide.

Pyxtrial automates the supervision of stablecoin balance sheets. It pulls data directly from issuers to verify that liabilities — the digital coins in circulation — are matched by assets: government bonds and cash reserves.

The documentation frames this as ‘consumer protection’. The function is to bring the shadow dollar system under the same surveillance umbrella as the regulated banking system. If you hold a digital dollar, Pyxtrial ensures the issuer is reporting your claim to the central authority.

The United States arrived at the same outcome. In January 2025, an executive order banned central bank digital currency37, and in July 2025, the GENIUS Act required all stablecoin issuers to possess the capability to ‘seize, freeze, burn, or block’38 payment stablecoins39.

Issuers are classified as financial institutions under the Bank Secrecy Act, subject to anti-money laundering, customer identification, and sanctions enforcement40. Foreign issuers must register with the Office of the Comptroller of the Currency and hold reserves in American financial institutions41. The state does not issue the currency, but it does compel whoever issues it to build and maintain the infrastructure at their own expense.

The American control architecture is identical, but implemented by the private sector rather than the central bank.

Project Aurora

Financial surveillance has traditionally operated in silos — one bank cannot see what another bank sees. A sophisticated actor can structure transactions across multiple institutions to avoid detection at any single point.

Project Aurora42 breaks these silos using what the BIS calls ‘Collaborative Analysis and Learning’.

The system deploys privacy-enhancing technologies that allow financial institutions to pool their data without technically sharing it. An artificial intelligence model trains on the collective dataset of multiple banks and payment providers simultaneously. It detects patterns that are invisible to any single institution — what the documentation describes as ‘complex money laundering schemes’ and ‘anomalous patterns’.

In effect, Aurora creates a single federated entity watching all transaction networks simultaneously. If an entity distributes activity across five different banks to stay beneath individual detection thresholds, Aurora’s unified model sees the aggregate pattern instantly.

Together, these projects create comprehensive situational awareness.

Climate TRACE watches facilities from orbit. NEMO estimates emissions for entities too small to observe directly. Danu models physical risk through digital simulation. Ellipse monitors the information environment for early warning signals. Atlas tracks capital fleeing into cryptocurrency. Pyxtrial monitors the stablecoin bridge. Aurora links the vision of every participating institution into a single analytical system.

The surveillance layer measures the gap between current reality and the directive — ‘is’ vs ‘ought’. It identifies who is compliant, who is not, by how much, and even who is attempting to exit.

IV. The Conditioning Layer

Awareness without consequence is observation. The conditioning layer converts surveillance into behavioural pressure.

The mechanisms operate through rewards and penalties — incentives that make compliance profitable and non-compliance expensive. They operate automatically, without committees convening or officials signing orders.

Basel 3.1: The Automatic Stranding Mechanism

The Basel Framework governs how much capital banks must hold against different asset classes. Higher risk weights mean higher capital requirements, which means higher cost of financing, which means the asset becomes less competitive.

Basel 3.1 introduces granularity to climate risk. Under the revised Standardised Approach, external ratings and specific risk factors directly determine capital charges43. The risk weight is not a judgment call, it’s a table lookup.

When Project Gaia flags an entity as high transition risk, the classification feeds into credit rating assessments. This determines the risk weight, which in turn determines the capital charge. The capital charge in effect determines whether holding the exposure is profitable.

No human decides to defund the company. The mathematics simply makes the loan unprofitable to hold.

This is the mechanism that strands assets automatically. A coal plant does not become uninvestable because a regulator issues an order. It becomes uninvestable because its risk classification triggers a capital charge that makes financing uneconomic. The stranding happens through calculation, and the input data might well be synthetic.

The same logic applies across the system. Every bank holding exposure to the flagged asset type faces the same capital mathematics simultaneously.

The asset strands without anyone lifting a finger.

The Green-Supporting Factor

The penalty has a mirror image. The Basel Framework provides preferential capital treatment for certified green assets. Banks holding green bonds or financing certified green projects face lower capital charges than equivalent conventional exposures.

Margin mathematics push banks toward green assets regardless of ideology. A portfolio manager seeking to optimise capital efficiency will favour assets that require less capital to hold. The Green-Supporting Factor and the Brown-Penalising Factor operate through the same capital mathematics in opposite directions44.

The carrot and the stick operate through the same mechanism: simple mathematics that makes compliance rational and non-compliance financially costly.

Insurance Withdrawal

Insurance operates as the first tripwire in the conditioning sequence. Most commercial loans require adequate insurance coverage as a covenant condition45. When insurance becomes unavailable or prohibitively expensive, the borrower breaches covenant regardless of operational performance.

The Global Resilience Index Initiative, co-chaired by Ben Caldecott of the Oxford Smith School, assigns resilience scores to infrastructure using digital twin data46. An asset with a low resilience score becomes high-risk in actuarial terms — the insurer withdraws or reprices, and the loan covenant triggers.

By 2023, the Insure Our Future campaign documented that 45 major insurers had adopted coal exit policies47. The market share of insurers refusing to underwrite new coal projects reached sixty-two per cent in reinsurance markets. Coal has become, in the campaign’s terminology, ‘increasingly uninsurable outside of China’.

The sequence is automatic. A digital twin assigns a synthetic score; the score determines insurability; insurability determines covenant compliance; covenant compliance determines whether a loan is allowed to continue.

If it isn’t, consider the asset ‘stranded’.

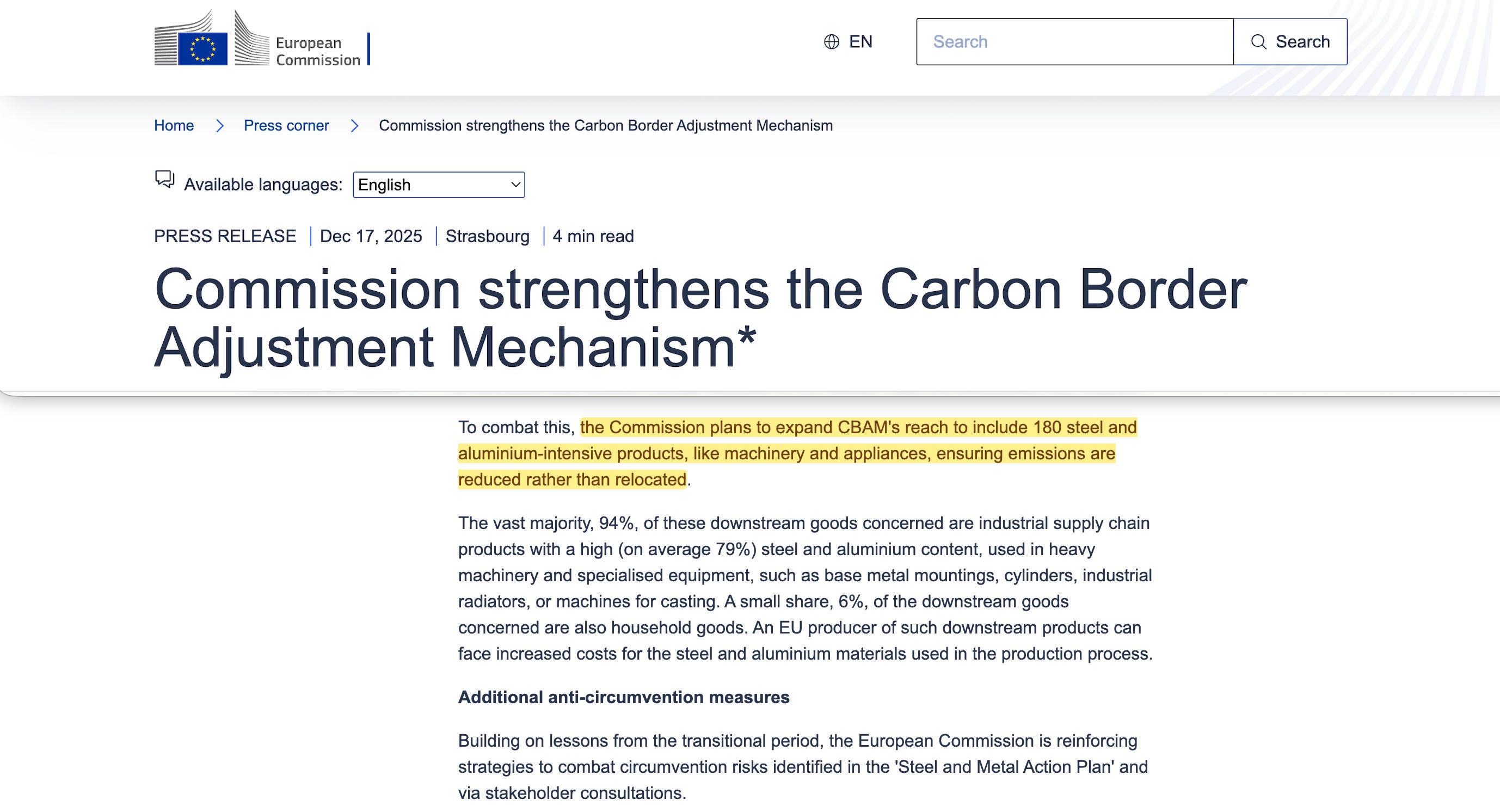

The Carbon Border Adjustment Mechanism

CBAM extends the automatic stranding mechanism across borders.

From January 2026, EU importers of covered goods — cement, iron, steel, aluminium, fertilisers, electricity, hydrogen — must purchase certificates reflecting the carbon embedded in those products48. The certificate price tracks EU Emissions Trading System allowances49.

Non-EU producers face a binary choice. They can provide verified emissions data to their European customers, subjecting themselves to the surveillance infrastructure. Or they can accept ‘default values’ — punitive estimates set at the highest emission intensity observed among countries with reliable data.

The mechanism requires no trade negotiation, no diplomatic pressure, no sanctions committee. A steel producer in Turkey or a cement manufacturer in India that does not adopt EU disclosure standards faces automatic tariffs based on algorithmic assessment. The tariff applies at the border, calculated from the classification — without human review.

CBAM makes the stranding mechanism extraterritorial. An asset that cannot export to Europe at competitive prices is worth less than an asset that can. The value differential is not imposed by decree. It emerges from the interaction of classification, surveillance, and automatic border pricing.

In December 2025, the European Commission announced expansion to 180 additional downstream products50 — pipes, structural steel, machinery, industrial equipment, household appliances. The stated intention is to cover all sectors under the EU Emissions Trading System.

The UK has announced its own CBAM from 202751.

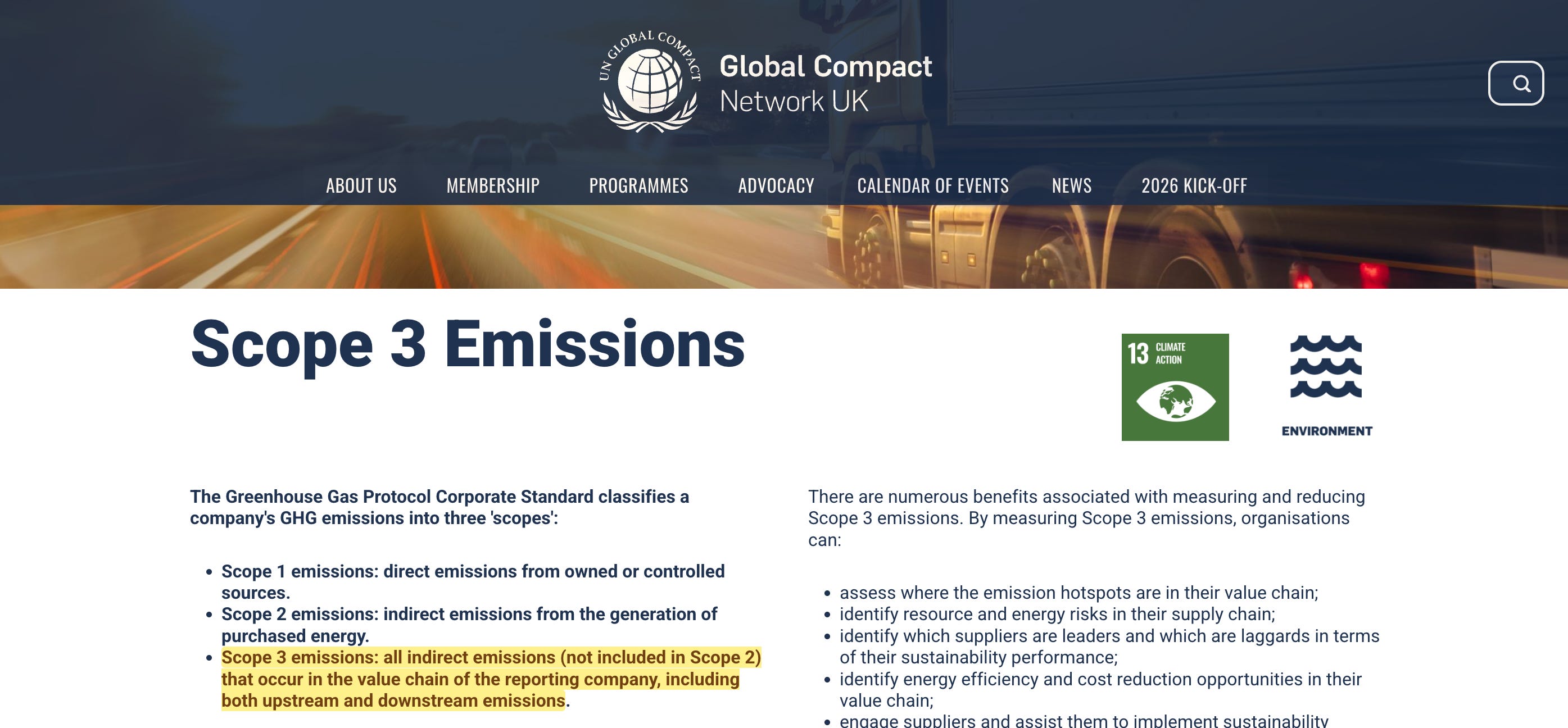

Scope 3 Requirements

Scope 3 emissions cover a company’s entire value chain — suppliers, customers, investments, employees52. They represent seventy to ninety per cent of most corporate carbon footprints. Under the Corporate Sustainability Reporting Directive, mandatory Scope 3 disclosure began in 2025 for large EU companies53.

The cascade effect reaches everywhere. A German automaker reporting Scope 3 emissions must account for the embedded carbon in steel from its Korean supplier. The Korean supplier must account for iron ore from Australia and coal from Indonesia. Each node in the supply chain becomes a data collection point.

When suppliers do not report, banks are authorised to use synthetic estimates. A January 2023 Smith School paper explicitly endorses ‘proxies’ and ‘machine learning’ to fill gaps, citing Climate TRACE and the Spatial Finance Initiative54 as data sources55.

The bakery that never reported finds its emissions estimated by NEMO, fed into the Scope 3 calculations of food companies it has never heard of, and priced through CBAM on products it did not know it was connected to.

Strategic Litigation

The Commonwealth Climate and Law Initiative, incubated at Oxford, published legal opinions arguing that directors who fail to consider climate risk breach their duty of care. Directors can be held personally liable for ignoring information they ought to have known — defined as the risk assessments and scenarios published by the network itself56.

By 2024, the Grantham Research Institute documented nearly 3,000 climate cases filed across sixty countries57. Approximately twenty per cent of cases filed that year targeted companies or their directors and officers directly. The success rate for climate-washing cases exceeded seventy per cent.

The conditioning layer shapes behaviour through every financial channel: the cost of debt, the cost of equity, the availability of insurance, the terms of trade, the threat of personal liability.

Compliance is rewarded. Non-compliance is penalised.

V. The Execution Layer

The final layer determines whether transactions proceed.

Traditional enforcement operates after the fact. A violation occurs, an investigation follows, a penalty is assessed. The subject retains agency until proven guilty.

Programmable finance inverts this sequence. Enforcement operates before the fact. Transactions that do not meet encoded criteria simply do not execute.

Project Mandala

Project Mandala automates compliance procedures for cross-border payments58. Sanctions screening, capital flow measures, and regulatory requirements are compiled directly into the payment protocol.

Money cannot leave a jurisdiction unless it satisfies the encoded policy requirements. The system does not flag non-compliant transactions for human review — it prevents them from initiating.

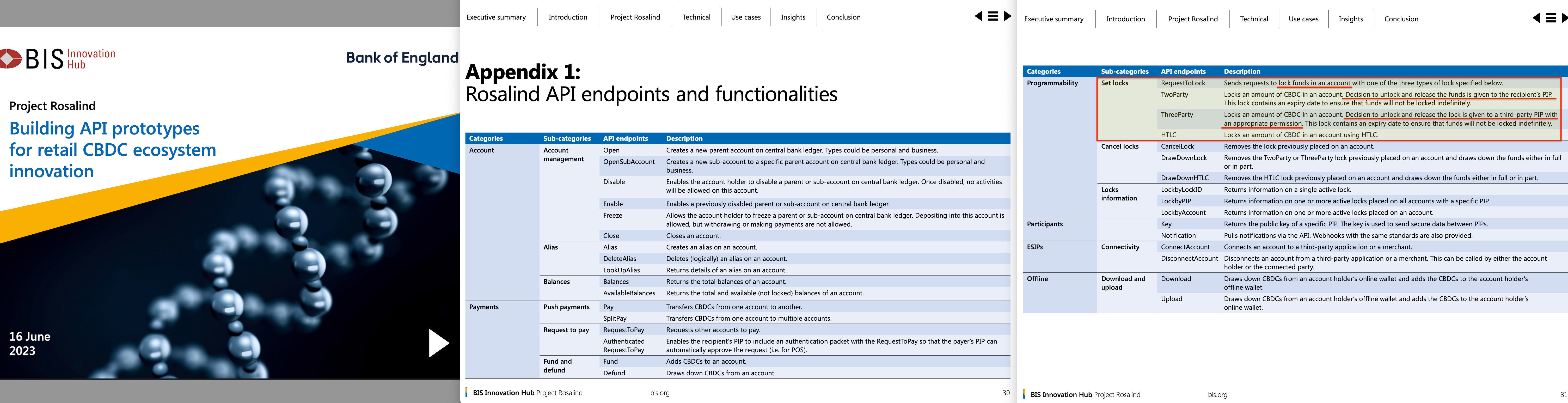

Project Rosalind

Project Rosalind59, developed jointly by the BIS Innovation Hub London Centre and the Bank of England, created thirty-three API functionalities for retail central bank digital currency distribution. The critical innovation is the multi-party lock.

The multi-party lock functions as automated digital escrow. Funds are held until conditions are satisfied: delivery verification, third-party authorisation, compliance checks, or any programmable criteria. The technology partner, Quant, explained the capability60:

What we found in digital money is we’re able to lock using different types of locks and program that lock for the first time.

A transaction does not fail because it’s blocked. The default is failure, and you have to prove your compliance, be it carbon credits in your account, or your vaccine status during an announced pandemic.

Project Agorá

Project Agorá develops a unified ledger where tokenised commercial bank deposits and wholesale central bank money coexist on a single programmable platform61. Seven central banks participate: the Bank of France, Bank of Japan, Bank of Korea, Bank of Mexico, Swiss National Bank, Bank of England, and Federal Reserve Bank of New York. Over forty private financial institutions are involved, including JP Morgan, Citibank, HSBC, Deutsche Bank, UBS, Visa, Mastercard, and SWIFT.

The unified ledger enables atomic settlement — instant, simultaneous exchange — but more significantly, it makes money itself programmable. Conditions can be encoded into the currency.

mBridge

mBridge62 connects central bank digital currencies across Asia and the Middle East: China, UAE, Thailand, Hong Kong, Saudi Arabia. The platform incorporates ‘programmable safeguards’ where exchange-rate management and cross-border capital controls are ‘embedded as core design principles’.

Project Icebreaker

If mBridge is the wholesale pipeline, Project Icebreaker is the retail cage63. Developed with the central banks of Israel, Norway, and Sweden, Icebreaker tests a hub-and-spoke model for interconnecting retail central bank digital currencies.

In this architecture, a citizen’s digital currency never leaves their domestic system. To pay someone abroad, the Hub executes a swap with a foreign exchange provider. The Hub selects the rate and routes the payment. The user has no custody of the foreign asset — only a domestic claim.

The architecture hard-codes capital controls into the infrastructure of cross-border retail payments. Money moves only through the approved Hub, at rates the Hub determines, along routes the Hub permits. The citizen retains the appearance of a digital wallet, while the system retains total control of cross-border movement.

You own a claim on a competing currency — not the currency itself. The central bank can prevent your exit.

SCO60: The Exit Prohibition

Basel Framework Chapter SCO60 governs bank exposures to cryptoassets64. It divides digital currencies into two groups.

Group 1 includes compliant assets: tokenised traditional assets, stablecoins with adequate reserves, central bank digital currencies. These receive standard risk weights.

Group 2 includes non-compliant assets: Bitcoin, decentralised finance, unbacked cryptocurrencies. These receive a 1250 per cent risk weight.

The 1250 per cent weight means a bank must hold capital equal to one hundred per cent of the exposure value. For every hundred dollars of Bitcoin a bank holds, it must hold one hundred dollars in capital. The mathematics makes it impossible for the regulated banking system to provide liquidity to decentralised alternatives.

The exit is watched by Project Atlas and blocked by capital requirements.

The Closed Loop

The components connect into a continuous cycle.

The NGFS scenarios define the target state — net-zero alignment along specified pathways.

Project Gaia classifies entities according to that target.

Climate TRACE, NEMO, and Danu measure the gap between current operations and required compliance.

Atlas and Aurora ensure that attempts to evade observation are themselves observed.

Basel risk weights, insurance scores, and CBAM tariffs apply pressure proportional to that gap.

Project Mandala compiles the rules.

Project Rosalind executes or rejects through payment conditionality.

Project Icebreaker ensures that retail cross-border movement passes through controlled hubs.

And the outcome even feeds back into the system. Companies that comply see their classifications improve. Companies that resist face compounding pressure. The gap between ‘is’ and ‘ought’ either closes or the entity is progressively excluded from the financial system, first through spiralling cost of capital, finally because you've become a liability no bank will carry.

The cycle operates continuously through transmitting satellites, classifying algorithms, and repriced capital. Transactions either clear or fail — no human decision intervenes at the critical nodes.

The Synthetic Data Regime

A control system requires information. When information is unavailable, the BIS architecture generates it.

The January 2014 specification paper from the Oxford Smith School acknowledged that ‘accurate quantitative projections’ did not exist for most climate factors. The authors demanded numbers anyway, because the financial system requires data points to function65.

This principle now operates at industrial scale.

When a company does not report its Scope 3 emissions, NEMO assigns an estimate based on sector, location, and financial characteristics.

When a facility does not disclose its carbon footprint, Climate TRACE infers it from satellite observation.

When the digital twin lacks verified data, it interpolates from available proxies.

The subject has no consent mechanism. The methodology is proprietary, and the estimate cannot be challenged through any administrative process.

A farm in England that has never engaged with climate disclosure finds its land mapped, its emissions estimated, and its risk profile assigned by AI systems trained on satellite imagery and natural language processing. The July 2025 Smith School dataset documented 117,116 farming entities mapped to ownership without the farmers’ participation66.

The stated purpose was explicit: ‘enabling verification of carbon credits, enhancing sustainability-linked loans, and improving risk assessment for climate finance’.

You are governed by numbers the system fabricated.

The Agricultural Extension

In May 2025, Nature Food published a paper by researchers including Ben Caldecott of the Oxford Smith School. The title was ‘Asset stranding could open new pathways to food systems transformation’67.

The paper did not frame agricultural stranding as a risk to be mitigated. It framed stranding as a mechanism to be deployed:

As the necessity of transitioning to food systems that are healthy and environmentally sustainable grows increasingly urgent, food systems seem to be locked into delivering negative outcomes. One driver of this lock-in is that some of the changes from transitioning food systems would result in asset stranding.

The solution proposed was to embrace stranding as a pathway for breaking lock-in. The paper cited Schumpeter’s theory of creative destruction and referenced the Glasgow Financial Alliance for Net Zero ‘Managed Phaseout’ framework — originally developed for coal power plants — as a model for agriculture.

The livestock sector was identified as the ‘bellwether case’. The paper argued that stranding traditional farms would ‘open pathways’ for ‘novel’ food systems to emerge.

The surveillance infrastructure provides targeting, while the disclosure regime provides mechanism. The outcome is liquidation of farms that cannot comply, and the input data might well be entirely synthetic.

The Sovereign Extension

The architecture applies to nations as well as companies.

In July 2025, the BIS published ‘Decoding climate-related risks in sovereign bond pricing’68. Researchers from the ECB, Sveriges Riksbank, Czech National Bank, Central Bank of Chile, and Bank of Greece examined fifty-two countries over two decades. The finding:

Transition risk is associated with higher sovereign yields, with the effect more pronounced for developing economies and for high-emitting countries after the Paris Agreement.

Countries that do not decarbonise at the required pace face automatic punishment through higher borrowing costs. The mechanism operates continuously. The bond market adjusts yield spreads according to transition risk scores without a sanctions committee hearing or a Security Council resolution.

ASCOR69 — Assessing Sovereign Climate-Related Opportunities and Risks — provides the scoring system. Developed by the Principles for Responsible Investment, the Transition Pathway Initiative, and the Institutional Investors Group on Climate Change, with the LSE Grantham Research Institute as academic partner, ASCOR covered seventy countries by 202470.

The stated purpose is to ‘incentivize governments’ through capital allocation. Countries with approved policies attract investment, while countries that resist face capital flight.

Project Promissa

The architecture also digitises the commitments of nations themselves. Project Promissa, a collaboration between the BIS, the Swiss National Bank, and the World Bank, tokenises promissory notes — the financial pledges that member nations make to international financial institutions71.

Historically, a nation’s pledge to the World Bank was a paper document, subject to diplomatic friction and administrative delay. Promissa converts these sovereign debts into digital tokens on a unified ledger.

The project creates a single source of truth for sovereign liability. A nation’s debt becomes a programmable object, visible to the central custodian, clearing instantly upon condition. It integrates the state’s fiscal obligations directly into the digital financial architecture.

The sovereign’s promise is no longer a treaty matter. It is a ledger entry.

When sovereign debt becomes distressed, the network offers a solution: debt-for-nature swaps. In May 2023, Ecuador exchanged $1.6 billion in sovereign debt for management rights over the Galapagos Marine Reserve72. The debt was purchased at a sixty per cent discount. Ecuador committed $18 million annually for twenty years to an offshore endowment beyond democratic oversight.

The same institutions that design the risk models that crash bond values then purchase the distressed debt and acquire governance over the territory.

The Retail Horizon

The architecture currently operates at wholesale level — corporations, banks, insurers, sovereigns. The infrastructure exists to extend it to individual citizens.

Project Rosalind’s multi-party lock can enforce conditions on any transaction. The EU Taxonomy defines which economic activities are sustainable. Mastercard’s Carbon Calculator, developed with Swedish fintech Doconomy, already tracks the carbon footprint of individual purchases across millions of cards73.

Doconomy’s DO Black card — marketed as ‘the credit card with a carbon limit’ — declines transactions when the user’s carbon budget is exhausted74.

Personal carbon allowances have been discussed in policy literature for decades. The obstacle was implementation — tracking individual consumption across thousands of daily transactions. Retail central bank digital currencies remove that obstacle.

China’s digital yuan pilot has explicitly linked CBDC to green finance75. A company received a digital yuan loan disbursed directly to its wallet, with observers noting the technology enables ‘precise control over the flow of funds’76.

Conclusion

The BIS Innovation Hub is not building isolated experiments. It’s building the components of a planetary financial control system.

The directives flow from NGFS scenarios shaped by integrated assessment models whose assumptions are not subject to democratic review.

The classifications flow from AI systems that scan, categorise, and label without human intervention.

The surveillance flows from satellites watching 352 million assets, algorithms generating emissions figures for entities that never reported, federated AI linking the vision of every participating bank, crypto intelligence platforms mapping the perimeter, and stablecoin monitors ensuring the shadow dollar remains visible.

The conditioning flows from capital requirements, insurance scores, and border adjustments that make non-compliance progressively more expensive.

The execution flows from programmable money that will not move unless conditions are satisfied, and hub-and-spoke architectures that ensure cross-border retail payments pass through controlled chokepoints.

The sovereign layer flows from tokenised promissory notes that convert national obligations into ledger entries, clearing instantly upon condition.

Each layer connects to the next. The output of classification feeds surveillance; the output of surveillance feeds conditioning; the output of conditioning feeds execution. The outcome returns to the directive layer, which adjusts scenarios for the next iteration.

The system is designed for expansion. Climate was the first application. The NGFS nature framework extends the architecture to biodiversity, water, and soil77. The Taskforce on Nature-related Financial Disclosures replicates the TCFD model for ecosystems. The EU Taxonomy’s Article 26 anticipates ‘other sustainability objectives, including social objectives’.

Seventeen Sustainable Development Goals. Each can acquire its own scenarios, its own classifications, its own surveillance apparatus, its own conditioning gradients, its own execution gates.

The SDG indicators78 enabling surveillance data normalisation already exist. Where measurement does not, the system can synthesise it.

The system's core operating principle is Anticipatory Governance — forward projection as financial control. Capital is allocated and withheld today on the basis of scenarios modelled decades ahead through proprietary assumptions. Stress tests project portfolio losses forward. Digital twins simulate events that have not occurred.

The NGFS scenarios are not forecasts — the documentation says so explicitly. They are plausible futures with no assigned probability, and they govern the present.

The same logic applies to the system itself.

Projecting the trajectory of an institutional programme with known participants, published technical specifications, and documented iteration cycles is a simpler problem than projecting global climate-economic interactions through 2050 using integrated assessment models calibrated to retracted papers.

Every component built to date remains available. No project’s outputs have been withdrawn, deprecated, or disavowed. Capability only accumulates.

The machine runs on data — real when available, synthetic when not.

It runs on scenarios — plausible rather than probable, with no assigned likelihood.

It runs on classifications — binary, automated, distributed across the network in real time.

It runs on mathematics — capital charges calculated algorithmically, insurance scores derived from digital twins, border adjustments applied without human review.

The machine runs… but mainly on indifference. Because every component described here is publicly documented. And it can be summarised very easily.

A black box governs the financial system, and the NGFS SAC — a committee with no published membership — governs the black box.

In his ‘Operating Manual for Spaceship Earth’79, Buckminster Fuller described a figure he called the Great Pirate80 — the navigator who controls global systems not through visible authority but through systemic design, ensuring that everyone else sees only their own specialisation and never the whole.

Were I the self-proclaimed Navigator of Spaceship Earth81, the NGFS SAC is probably where I would hide.

Looking at the cage is not looking on the lies of which the cage is constructed.

Looking at the symptoms and assuming that to be the disease - seeks to get rid, scape or eradicate symptoms without losing vested identity in masking lies.

Hence the masking agenda MUST run hidden as 'knowing not what ye do' - for the masked identity operates under masking dictates.

The mask of control requires sacrifice of awareness of being.

The masking management of conflict protects conflict by sacrificing life.

There is another way of looking than through the frame of a control mindset, but this calls for releasing or yielding of 'control' to a love we do not and can not manufacture.

It is by thinking that the mind becomes 'trapped in self-circular contradictions.

What we take as the basis for thought can run as a self-reinforcing loop.

We are always choosing and thus teaching and learning by our choices.

For the most part we automate on default assumptions that then 'structure' our world-experience/identity. But as pain of such a life breaks through the asking suppressions, we will come to question the basis from which we thought to think alone.

How do we stop these monsters? That is the question. Satyagraha will simply result in people starving to death, won't it?