The SDG Machine

‘The Innovation Hub’ discussed how BIS Innovation Hub projects assemble to become a planetary financial control system focused on carbon emissions.

The architecture, however, was never specific to climate.

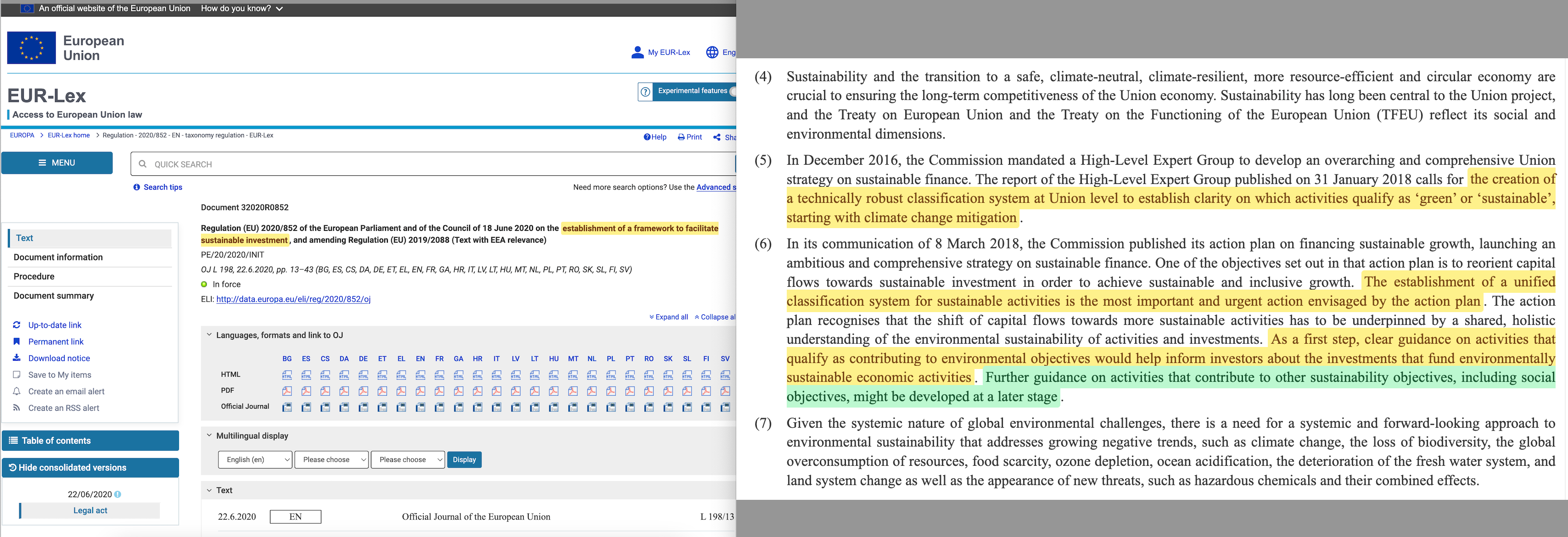

The EU Taxonomy Regulation of 20201 made this explicit in Article 26, which stated that guidance on activities contributing to ‘other sustainability objectives, including social objectives, might be developed at a later stage’.

Since Article 26 was published, the BIS has expanded the Innovation Hub from six centres to seven2, increased its project portfolio, and published a 44-page blueprint for extending the system to every individual participant in the global economy.

Each new project generalises the architecture further from its climate origins, bringing a new domain under the same operational logic.

The Blueprint

In April 2024, Carstens and Nilekani published a BIS working paper proposing the ‘Finternet’3: a vision of interconnected financial ecosystems built on unified ledgers, with compliance and governance embedded directly in the technology.

The paper identified three structural requirements: an efficient financial architecture, the application of advanced technology, and a robust legal and regulatory basis. On the question of identity, it was explicit:

… identity is central to the enforcement of rules and policies within the system, necessitating features like traceability, accountability and observability directly tied to identity management.

This is the layer that connects the wholesale infrastructure to the individual citizen. The Innovation Hub projects described in the prior essay operate primarily at the institutional level — banks, corporations, sovereigns. The Finternet paper extends the architecture to retail transactions by anchoring it to digital identity.

The operational template is India’s ‘India Stack’, which combines Aadhaar4 (digital ID), the Unified Payments Interface5 (real-time payments network), and a data exchange layer that enables verified document sharing6. The BIS published a detailed study of this model in 2019, noting that India had accelerated ‘financial inclusion’ (onboarding the poor) from 17 per cent bank penetration to 80 per cent in a decade — a process that would ordinarily have taken fifty years.

The model is currently being exported. Nigeria, Kenya, and Bangladesh have adopted Aadhaar-derived digital identity systems. Ghana has modelled its payment infrastructure on UPI7. Nepal has integrated UPI for cross-border transactions8. Trinidad and Tobago signed a memorandum of understanding with India’s NPCI International in September 20249. At the IMF in April 2025, Nilekani confirmed the Finternet was moving from concept to implementation10:

In the last one year, we have created a lot of the basic tools for how this Finternet would look like, how you do credentialing, and how you create wallets.

The technology would be released as open source, available for any jurisdiction to adopt.

The Finternet paper describes the end state, the Innovation Hub projects build the components, and digital identity provides the binding layer. Without it, the system classifies and conditions institutions. With it, the system reaches every participant in the financial system.

The Finternet paper anticipates the surveillance concern. It devotes substantial space to privacy-enhancing technologies — zero-knowledge proofs, multi-party computation, self-sovereign identity — which would allow users to prove compliance without revealing the underlying data. These are technically substantive mechanisms. But they protect the data in transit, not the classification logic. A user could demonstrate taxonomy alignment through a zero-knowledge proof and still be subject to an AI classification they cannot see, built on criteria they did not set, enforced through a smart contract they cannot appeal.

The privacy layer addresses surveillance of personal information. It does not address who defines compliance, who operates the classifier, or who writes the conditions embedded in the token.

The Grammar

For the architecture to operate across domains, it requires standardised data inputs. Data from different sources must speak the same language before it can be aggregated, analysed, and acted upon. The financial system historically lacked these — payment messages varied by jurisdiction, format, and protocol.

Project Keystone11, launched by the London Centre in collaboration with the Bank of England, addresses this by building a standardised analytics platform for ISO 2002212, the messaging standard now adopted by 93 per cent of payment system operators worldwide13.

ISO 20022 replaces unstructured payment messages with a rich, structured data format. A traditional SWIFT MT10314 message carries a sender, a receiver, an amount, and a free-text reference field. An ISO 20022 message can carry the legal entity identifier of the payer, the purpose code of the transaction, the tax identification number of the beneficiary, and structured remittance information linking the payment to a specific invoice or contract.

Keystone provides two modules: one for managing the complex data structure and storage requirements of ISO 20022, and another for conducting data-driven analysis. The BIS documentation describes capabilities for ‘real-time economic monitoring’ and ‘liquidity oversight’. It is designed as an off-the-shelf component that any payment system operator can integrate.

When every cross-border payment carries a standardised, machine-readable description of who is paying, why, and to whom, the surveillance and classification layers described in ‘The Innovation Hub’ acquire a universal grammar. Project Mandala’s automated compliance checks15, Project Aurora’s federated financial crime detection16, and Project Hertha’s network analytics all become more effective when the underlying data conforms to a single specification17.

Without standardised data…

… Project Aurora’s collaborative learning cannot function — banks speak different dialects.

… Project Gaia’s classification cannot propagate — labels do not translate18.

… Project Mandala’s compliance rules cannot compile — the code cannot read the inputs.

Keystone19 provides the Rosetta Stone. Once all payment data speaks the same language, any analytical layer can be placed on top — and climate was merely the first.

The Cognitive Layer

The companion essay described Project Gaia as the BIS’s AI tool for analysing climate-related financial risk, trained to assess corporate disclosures against the EU Taxonomy. Gaia was climate-specific by design — its training data, its classification criteria, and its outputs were all calibrated to environmental objectives. What has changed since is that the BIS itself has announced Gaia’s extension beyond climate. The 2025-26 work programme states that20:

Project Gaia will build on the already developed proof of concept, which addressed the specific use case of climate-related risk analysis, by extending it to other use cases within and beyond the theme of green finance.

Two additional projects complete the generalisation.

Project AISE21 (Artificial Intelligence Supervisor Enhancer), developed by the Toronto Centre, builds a virtual assistant for financial supervisors capable of automating research, enhancing on-site supervision, and supporting decision-making processes.

AISE is Gaia without the climate constraint. Where Gaia scans disclosures for net-zero alignment, AISE scans for whatever the supervisor wishes to find. The documentation describes ‘general AI automation for central bank oversight’.

The architecture is identical — ingest documents, extract indicators, flag discrepancies, generate classifications — and the objective function is simply a parameter. Set it to carbon emissions and you have Gaia. Set it to labour practices and you have a social compliance scanner. Set it to political donations and you have something else entirely.

The BIS describes AISE as a response to the challenge of high staff turnover and the ‘ongoing need for training and adaptation to sophisticated market dynamics’ within supervisory institutions — embedding proven supervisory practices into an AI tool that any regulator can deploy against any regulatory objective22.

Project Noor23 addresses the interpretability problem. AI classification tools like Gaia produce outputs — risk scores, taxonomy alignments, compliance flags — but the reasoning behind those outputs is frequently opaque. When an algorithm makes a decision, regulators demand to know why. Noor develops explainable AI frameworks for supervisory decisions, so that a regulator can justify an adverse classification to the entity classified.

The function is legitimation. Explainable AI makes automated classification defensible. When AISE flags a company for non-compliance, Noor ensures the reasoning can be documented. The appeal process receives an answer it cannot easily challenge.

Together, these three projects describe a progression:

Gaia demonstrated that AI could classify entities against a regulatory taxonomy, its announced expansion applies that capability beyond climate

AISE generalises it to any supervisory domain

Noor provides the justification layer that makes the outputs defensible

The resulting cognitive architecture is domain-agnostic.

The Settlement Infrastructure

A parallel set of projects has been assembling the settlement infrastructure that would make enforcement operationally scalable. Several of these have moved beyond prototyping into deployment.

Project Nexus24 is the most consequential. It connects domestic instant payment systems across borders through a hub that standardises connectivity protocols. Nexus was handed to partner central banks for live implementation in 2024, making it one of the first Innovation Hub projects to move from experiment to production infrastructure.

Where mBridge25 and Icebreaker26 require CBDC adoption, Nexus works with existing payment rails. The cross-border payment plumbing does not depend on any single jurisdiction’s decision to issue a digital currency; it is being built on what already exists.

Project FuSSE27 (Fully Scalable Settlement Engine) provides an open-source, modular settlement engine that any jurisdiction can integrate into payment systems, securities settlement, or other financial market infrastructure.

It targets developing economies specifically through the IDB partnership.

Project Rialto28, published in December 2025, combines automated foreign exchange with tokenised central bank money settlement for instant cross-border payments, building explicitly on both Mariana29 and Nexus.

It represents the convergence of earlier projects into a single integrated cross-border mechanism.

Two completed projects demonstrate that the architecture does not merely clear or block transactions but can create entirely new financial instruments with embedded compliance conditions.

Project Genesis30 (presented at COP27) produced tokenised green bonds with real-time IoT-based environmental impact tracking and smart contract-based carbon credits attached directly to the bond instrument.

Classification, surveillance via physical sensors, and programmable enforcement were collapsed into a single financial product — and the ESG covenant structure was explicitly designed to be replicable across other sustainability domains.

Project Dynamo31 built programmable digital trade tokens for SME finance on a public blockchain, with a critical design feature: the prototype included ESG conditions for triggering payment. A payment released only when sustainability criteria were met — Rosalind’s three-party lock applied to trade finance, with environmental compliance as the unlock condition.¹⁹

Project Leap32 (Phase II) addresses permanence. Having established a quantum-safe communication channel between the central banks of France and Germany in Phase I, Leap now demonstrates how payment systems can be protected from quantum computing — the one technology that could theoretically break the cryptographic foundations of the entire architecture.

The Market Eye

The surveillance layer built for climate — Climate TRACE, NEMO, Danu, Ellipse — operates on corporate assets and disclosures. It watches facilities, estimates emissions, models physical risk, monitors sentiment. A parallel surveillance architecture watches financial markets directly.

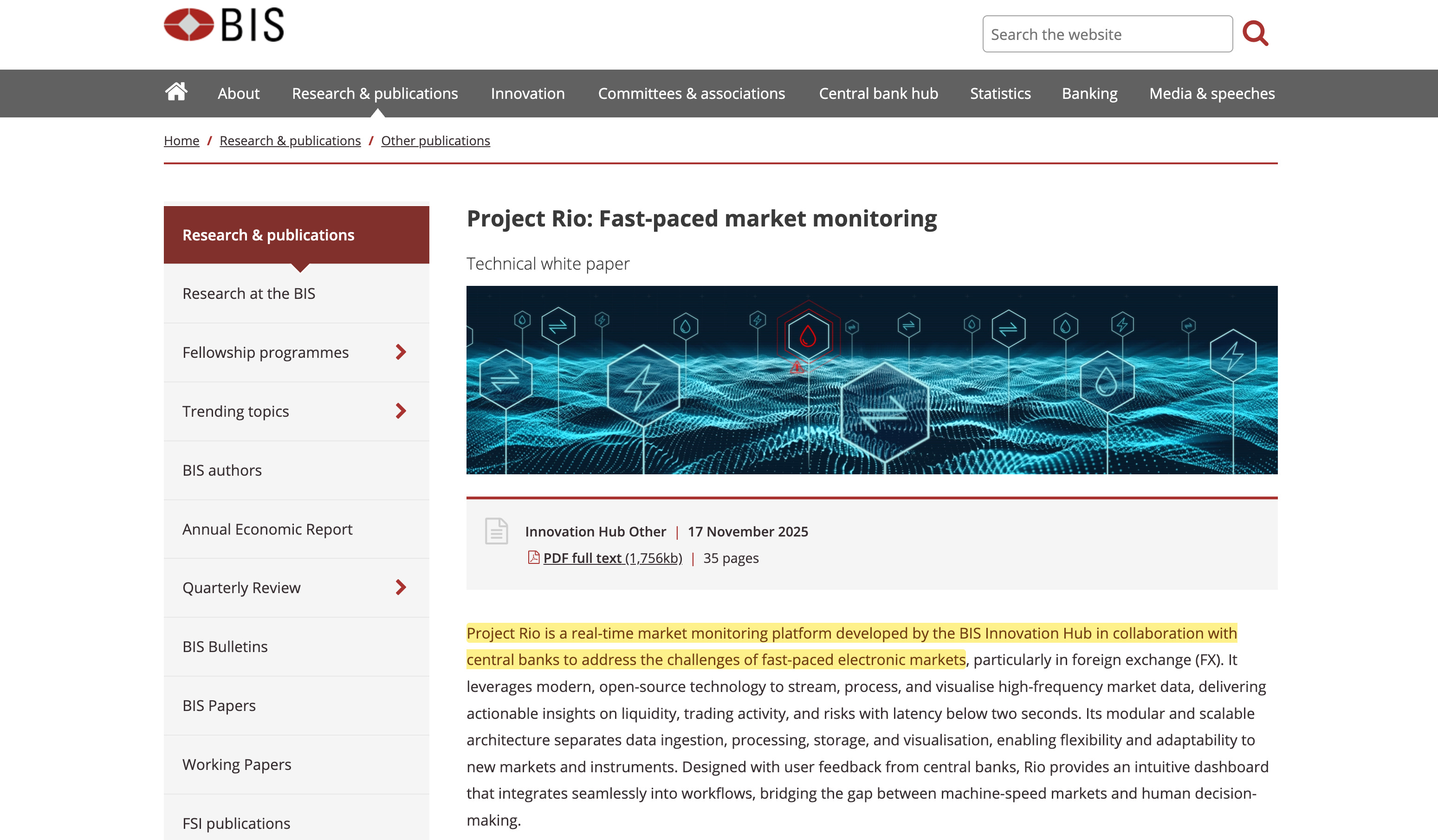

Project Rio33, developed by the Singapore Centre, builds a real-time, cloud-based market monitoring platform. It processes financial data feeds to compute liquidity measures and market risk indicators continuously.

The system operates at market speed. Where traditional supervision reviews quarterly reports, Rio watches order books in real time. It identifies stress building in specific markets before the stress manifests as crisis. The BIS describes Rio as suptech for fast-paced electronic markets — not merely the carbon-intensive sectors that Climate TRACE observes, but all traded instruments34.

Project Hertha35 deploys network analytics to map financial crime patterns in payment systems.

Rather than flagging individual suspicious transactions, it identifies suspicious clusters — networks of entities whose relationships suggest coordinated activity. Hertha’s approach is architecturally significant because network analysis operates independently of what the network carries.

A transaction graph that reveals money laundering patterns can also reveal sanctions evasion, tax structuring, or any other pattern that regulators define as anomalous. The tool requires only a definition of the target pattern and a sufficiently granular data feed — which is precisely what ISO 20022 adoption and Project Keystone provide.

The BIS has been explicit about the intended convergence. Through projects Mandala, Hertha, and Aurora, it stated, ‘we have started to develop components for a global financial integrity technology stack’36.

The Nature Extension

The first domain extension beyond climate is biodiversity, and it is already well advanced.

The NGFS published its conceptual framework for nature-related financial risks3738. The framework extends the climate architecture to biodiversity, water, soil, and ecosystem services. The logic mirrors climate exactly.

Physical risks arise from environmental degradation — pollinator collapse affecting agriculture, water scarcity affecting manufacturing, deforestation affecting local climate. Transition risks arise from policy responses — regulations protecting ecosystems, liability for environmental damage, market shifts away from nature-intensive products. The NGFS framework specifies that nature risks should be integrated into the same stress-testing and scenario analysis processes developed for climate.

The scenarios are different, but the mechanism is identical.

The Taskforce on Nature-related Financial Disclosures (TNFD), modelled on the climate-focused TCFD, published its final recommendations in September 202339. By September 2025, 730 organisations across more than fifty countries — including 179 financial institutions managing $22.4 trillion in assets — had adopted the framework. Over 500 TNFD-aligned reports had been published.

Sixty-three per cent of surveyed companies viewed nature-related risks as equal to or more significant than climate risks for their long-term financial prospects, and 78 per cent of disclosing companies had integrated climate and nature reporting into a single process40.

The TNFD signed a memorandum of understanding with the IFRS Foundation in 2025, aligning it with the International Sustainability Standards Board41 (ISSB) — the same body that globalised climate disclosure by absorbing the TCFD recommendations into mandatory reporting standards42.

The institutional pathway that converted voluntary climate disclosure into binding financial regulation is being replicated for biodiversity through the same organisations, the same standard-setting bodies, and the same integration with banking supervision.

Within the Innovation Hub, Project Danu43 — the digital twin integrating climate data, geographic information, and financial exposure mapping — is designed for expansion beyond climate. The documentation describes modelling ‘physical and nature-related risks’.

A digital twin that models flood risk can model water stress. A system that traces climate impact through supply chains can trace deforestation impact through the same chains. The NGFS Data Directory 2.044 catalogues data sources across the full environmental domain, redesigned as a public resource.

The surveillance infrastructure built for carbon already observes ecosystems with minimal modification.

The Social Extension

The EU Taxonomy’s Article 26 anticipates ‘social objectives’45. The Platform on Sustainable Finance published its final Social Taxonomy report in February 202246, proposing a structure with three defined objectives:

Decent Work (including value chain workers in third countries)

Adequate Living Standards and Well-being for End-Users (covering health, food, housing, and education)

Inclusive and Sustainable Communities and Societies (addressing non-discrimination, community livelihoods, and access to basic economic infrastructure)47

Each objective includes sub-objectives, proposed criteria, and a structure that mirrors the environmental taxonomy’s framework of substantial contribution and ‘do no significant harm’ assessment.

The Platform’s third mandate, running from February 2026 through end-2027, is now active48. Article 18 of the existing Taxonomy Regulation already imposes minimum social safeguards — requiring taxonomy-aligned activities to comply with the UN Guiding Principles on Business and Human Rights49, the OECD Guidelines for Multinational Enterprises50, and the International Bill of Human Rights51.

The Social Taxonomy would convert these safeguards from minimum thresholds into a full classification framework — with the same architecture of criteria, screening, and assessment currently applied to environmental activities.

But social objectives present a measurement problem that environmental objectives do not. Carbon dioxide is fungible and somewhat measurable. Labour practices vary by context and resist quantification. ‘Decent Work’ in a garment factory in Bangladesh involves assessments of wage adequacy relative to local cost of living, freedom of association in a jurisdiction that may restrict it, workplace safety standards that vary by sector and country, and supply chain traceability across multiple tiers of subcontracting52. These are judgements dressed as measurements.

The BIS has been solving this through the AI projects. AISE and Noor enable classification of qualitative data — documents, reports, narrative disclosures — that cannot be reduced to simple metrics. Where Climate TRACE measures emissions from satellite imagery53, AISE can classify labour compliance from corporate reports, news coverage, and regulatory filings.

The cognitive layer requires patterns, not quantitative inputs. If a social criterion can be specified — ‘adequate living wage’, ‘safe working conditions’, ‘non-discrimination’ — AISE can scan for indicators of compliance or non-compliance. Noor ensures the classification can be explained. The measurement challenge reduces to a training problem — the architecture already supports it.

The Platform on Sustainable Finance’s February 2025 report on taxonomy simplification addressed the data gap directly. It recommended54:

… allowing for estimates and proxies for reporting subject to guidance and criteria, in conjunction with safe harbours to protect against greenwashing allegations.

This applies to the 99 per cent of European businesses classified as SMEs.

The recommendation would institutionalise a regime in which banks use modelled estimates — of the kind that Project NEMO55 already produces for supply chain emissions — as the basis for taxonomy classification, with legal protection against challenge.

The entity being classified would have no ground to contest a synthetic estimate backed by regulatory safe harbour.

The Seventeen Goals

The United Nations Sustainable Development Goals provide the complete list of potential applications.

The architecture built to enforce Goal 13 (Climate Action) can enforce any of the others. Each goal can acquire:

Scenarios specifying pathways to compliance (NGFS model)

Taxonomies defining which activities qualify (EU Taxonomy model)

Disclosure frameworks requiring companies to report (TCFD/TNFD model)

AI classification scanning reports and flagging non-compliance (Gaia/AISE model)

Surveillance measuring the gap between current state and target (Climate TRACE/Rio model)

Capital requirements conditioning behaviour through cost of finance (Basel model)

Programmable enforcement executing or rejecting transactions (Rosalind/Mandala model)

Goal 8, Decent Work and Economic Growth, illustrates the pattern concretely. The Social Taxonomy already defines Decent Work as an objective with proposed criteria. AISE can classify corporate labour disclosures, NEMO can estimate supply chain working conditions for entities that do not report, Aurora’s federated learning can detect patterns across institutions, and Mandala can compile the resulting compliance rules into cross-border payment protocols.

The architecture needs only to be pointed at the objective.

The goals are already specified, the measurement techniques exist56, and the architecture is operational.

Monetary Policy on the Ledger

Project Pine57, referenced alongside Agorá in the June 2025 Annual Economic Report58, explores how central banks can implement monetary policy operations in a tokenised environment. Interest rate transmission, open market operations, collateral management, and liquidity provision — the most fundamental tools of central banking — would operate through the same programmable platform that hosts the classification, surveillance, and enforcement layers.

The June 2025 report described how tokenised government bonds on a unified ledger would serve as ‘the cornerstone of financial markets’, enabling ‘collateral management, monetary policy operations, and various financial transactions’ to be automated through smart contracts.

In a tokenised environment, a central bank could adjust collateral haircuts, modify lending facility terms, or implement tiered reserve requirements through programming instructions rather than administrative processes.

The implication extends beyond automation. In the current system, monetary policy operates through intermediaries: a central bank adjusts its policy rate, commercial banks pass the change through to lending and deposit rates, and the effect propagates through the economy over weeks or months. The transmission mechanism depends on commercial bank behaviour, which central banks influence but do not control. On a unified ledger, this intermediation becomes optional.

If a central bank can programmatically adjust the properties of tokenised money and bonds held within the system, it can apply policy changes directly — modifying interest accrual on reserves, imposing tiered or negative rates on specific holdings, or setting expiration conditions on emergency liquidity. The announcement effect, where a central bank speaks and markets respond, gives way to direct execution, where the code updates and the money behaves differently.

Qualitatively, this is a different claim from the domain-extension argument that structures the rest of this essay. The classification, surveillance, and conditioning layers accept new parameters — swap climate for biodiversity or labour standards, and the architecture runs the same pipeline.

Project Pine does something else: it places the most fundamental function of central banking on the same programmable platform. It ceases to be a tool that central banks use and becomes the environment in which central banking takes place.

The Finternet paper itself explicitly preserves the two-tier monetary system — central bank money as foundation, commercial banks as intermediaries. But if the unified ledger makes intermediation technically optional, the architecture enables what monetary reformers have long called ‘positive money’: a system where only the central bank issues currency, and commercial banks lose the capacity to create money through lending.

The infrastructure does not even require legislation to reach this outcome, incidentally comparable to plank 5 of the communist manifesto59.

The Convergence

The projects are designed for integration. The BIS Innovation Hub’s 2025-26 work programme explicitly emphasises ‘synergies between projects and themes’6061 — AI tools linking to green finance extensions, suptech platforms feeding supervisory dashboards, data standards enabling cross-border analytics.

Keystone standardises the data. AISE classifies the disclosures. Rio monitors the markets. Hertha maps the networks. Aurora links the institutions. Gaia handles climate. TNFD handles nature. The Social Taxonomy handles labour and equity. Viridis distributes the classifications. Basel prices the risk. Mandala compiles the rules. Rosalind executes the lock. Nexus connects the existing payment systems. Agorá builds the unified ledger. FuSSE provides the modular settlement engine. Genesis and Dynamo demonstrate that the entire chain — classification, surveillance, programmable enforcement — can be collapsed into a single financial instrument. Pine places monetary policy itself on the platform. Leap quantum-proofs it against future cryptographic threats.

The June 2025 Annual Economic Report provided the integrating vision62. Tokenised central bank reserves, tokenised commercial bank money, and tokenised government bonds, residing on a unified ledger, form what the BIS called the ‘trilogy’ at the foundation of the next-generation financial system. Each project is modular and connects to the others through standardised interfaces. The BIS Innovation Hub’s design philosophy — interoperability across centres — ensures the components snap together.

The convergence is not merely hypothetical. The Coalition of Finance Ministers for Climate Action documented forty-one national roadmaps from thirty countries63. Twenty-three per cent of these roadmaps were drafted by the Generation Foundation64, Principles for Responsible Investment65, and UNEP Finance Initiative66 — the network’s own templates adopted as national policy.

The same pattern will apply to nature, to social objectives, to each SDG in turn: international bodies produce the standards, think tanks draft the templates, national governments adopt the frameworks, central banks enforce through capital requirements, and the BIS provides the technology layer.

Carstens described the end state at the Santander conference in October 2024: a system in which ‘individuals and businesses could transfer any financial asset, in any amount, at any time, using any device, to anyone else, anywhere in the world’ — subject to compliance rules embedded in the transfer protocol itself67.

The installation is incremental: each SDG adds another module, each module reinforces the others, and the system grows by accretion.

The Political Friction

The extension is not proceeding without resistance. The European Commission’s February 2025 ‘Omnibus’ proposals to streamline the Corporate Sustainability Reporting Directive (CSRD) would significantly reduce the scope of mandatory taxonomy reporting, exempting smaller companies and narrowing disclosure requirements68.

The Platform on Sustainable Finance itself warned that reducing CSRD scope ‘results in the loss of specific Taxonomy data’ and ‘reduces the effectiveness of the Taxonomy generally in the market’69.

Several EU member states and industry lobbies have pushed back against the reporting burden. The Omnibus package70 represents genuine democratic accountability operating on the disclosure layer — the layer where citizens and businesses actually interact with the classification regime. This is where resistance can form, where legislators face electoral consequences, and where the burden of compliance is felt directly.

The constraint, however, operates only on the disclosure mandate — on the question of which companies must report their taxonomy alignment. It does not reach the infrastructure layer. The BIS Innovation Hub projects, the unified ledger architecture, the AI classification tools, and the programmable settlement systems continue to develop on their own timeline, funded by central bank contributions and governed by the BIS’s institutional processes. The NGFS scenarios, the TNFD framework, and the ISSB standards continue to mature independently of whether any individual EU directive survives the legislative process. The infrastructure layer develops without equivalent democratic input.

The distinction matters because the architecture described in these essays does not depend on voluntary corporate self-reporting. Projects like NEMO estimate supply chain emissions from trade and shipping data without requiring corporate input. Climate TRACE monitors emissions from satellite imagery. Project Gaia classifies entities by analysing publicly available disclosures.

The surveillance and classification layers can operate with or without the co-operation of the entities being classified.

Political friction slows the formal adoption of taxonomy-aligned regulation. It does not slow the construction of the infrastructure that makes taxonomy-aligned enforcement technically possible.

The Accountability Gap

The generalisation introduces a compounding accountability problem.

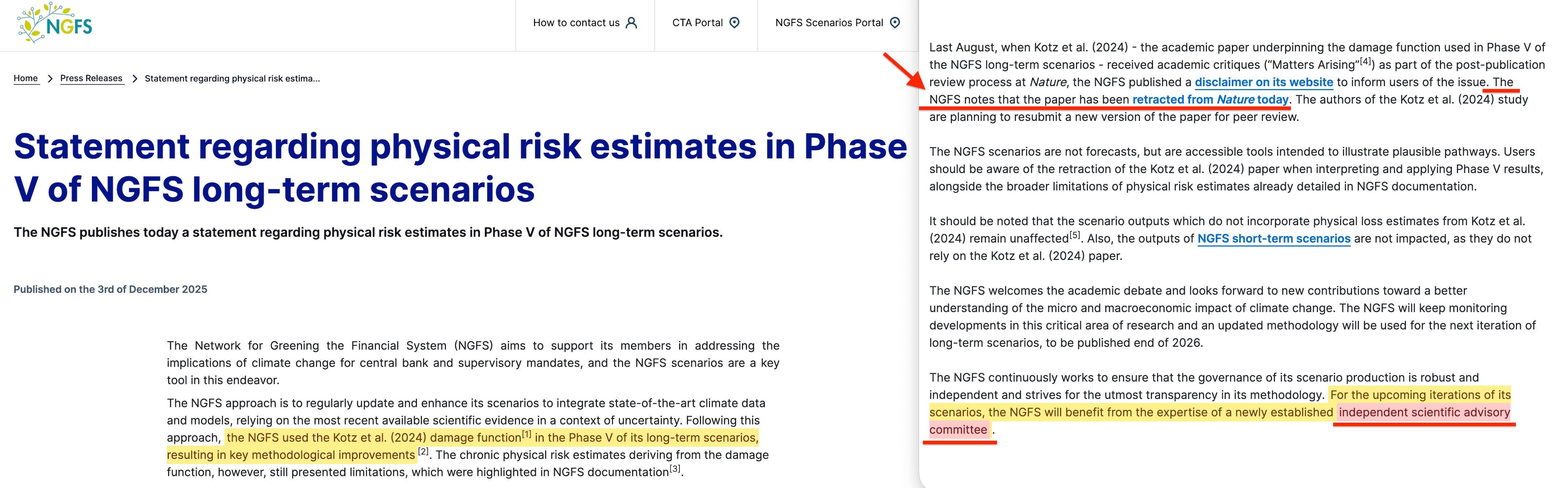

For climate, the NGFS scenarios rest on integrated assessment models from the IIASA-Potsdam consortium. When the Kotz paper was retracted71, the damage estimates fell by two-thirds. The scenarios continued operating. The principle established in January 2014 holds: accurate quantitative projections do not exist for most factors, but data points are required for the financial bureaucracy to function.

For nature, the measurement challenge is greater. Ecosystem services resist quantification more than carbon emissions — the models will be less precise, the confidence intervals wider, the disclaimers more numerous.

The TNFD’s LEAP framework72 (Locate, Evaluate, Assess, Prepare) acknowledges this complexity but does not resolve it. When a financial institution classifies a borrower as ‘nature-negative’ on the basis of modelled ecosystem impact data, the borrower’s ability to contest that classification is materially weaker than in the carbon case, because the underlying measurement is less certain and the methodological choices less transparent.

For social objectives, the measurement challenge is greater still. Labour practices, gender equity, and community impact cannot be observed from satellite imagery. They depend on narrative disclosures, third-party reports, determinants, and AI classification of qualitative text.

The Platform on Sustainable Finance’s recommendation to allow ‘estimates and proxies’ with legal ‘safe harbours’ would institutionalise the use of synthetic assessments as the basis for financial consequences, while shielding the assessor from legal challenge.

At each stage of extension — from carbon to biodiversity to social objectives — the certainty of the inputs decreases while the consequences of the outputs remain automatic. An entity classified as non-compliant faces higher capital costs whether the classification is accurate or not — and no appeal mechanism exists, because the liability shield protects the classifier.

Project Noor’s explainable AI provides a reasoning chain, not an error correction process. The system can articulate why it flagged an entity. It cannot acknowledge that it was a mistake.

The machine operates on the principle that operational functionality, rather than accuracy, is the binding constraint. The further the architecture extends from physically measurable environmental variables into qualitative social territory, the wider the gap between the certainty of the input and the automaticity of the consequence.

An entity governed by this system is governed by classifications that grow progressively less verifiable, enforced through mechanisms that remain uniformly unappealable.

The Emergency Protocol

The architecture described so far operates incrementally — adjusting capital requirements, conditioning lending terms, stranding assets through repricing. The UN Emergency Platform73, adopted in the September 2024 Pact for the Future74, provides the mechanism for switching to emergency mode.

The Platform grants the Secretary-General standing authority to declare a ‘complex global shock’ and convene governments, financial institutions, and private sector actors into coordinated response. The listed triggers include ‘large-scale climatic or environmental events’, ‘major disruptions to global flows of goods, people, or finance’, and ‘events leading to large-scale impact across multiple sectors’.

The definition is deliberately broad: a ‘complex global shock’ is characterised not by objective severity but by cascading consequences across multiple domains75.

The Emergency Platform operates through multiple enforcement rails, one of which is explicitly financial: capital routing based on compliance through NGFS climate scenarios, ESG scoring, and prudential standards. The Innovation Hub projects described in this essay and its companion — the unified ledger, the programmable settlement, the AI classification, the capital conditioning — constitute this financial rail.

Under normal operation, these tools adjust behaviour gradually through the cost of capital. Under emergency activation, the same infrastructure could freeze capital, redirect investment, or suspend normal market functions — not through new mechanisms, but through accelerated application of existing ones.

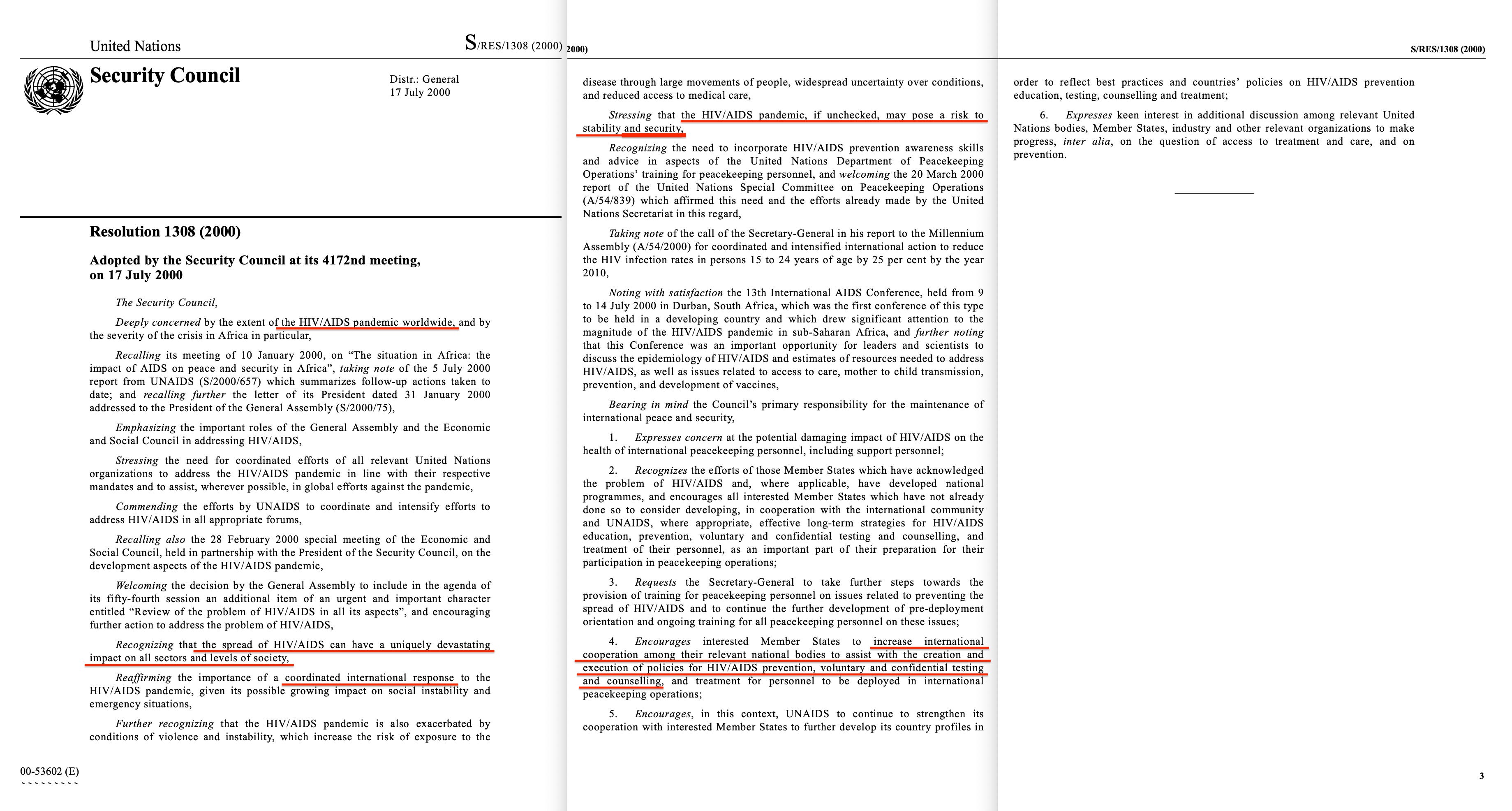

The institutional precedent for this escalation has been established incrementally. Resolution 47/6076 (1992) expanded ‘peace and security’ to encompass socio-economic factors. Resolution 130877 (2000) declared HIV/AIDS a global security risk — creating, through PEPFAR, a metrics-based health surveillance architecture that became interoperable with ESG-style measurement frameworks.

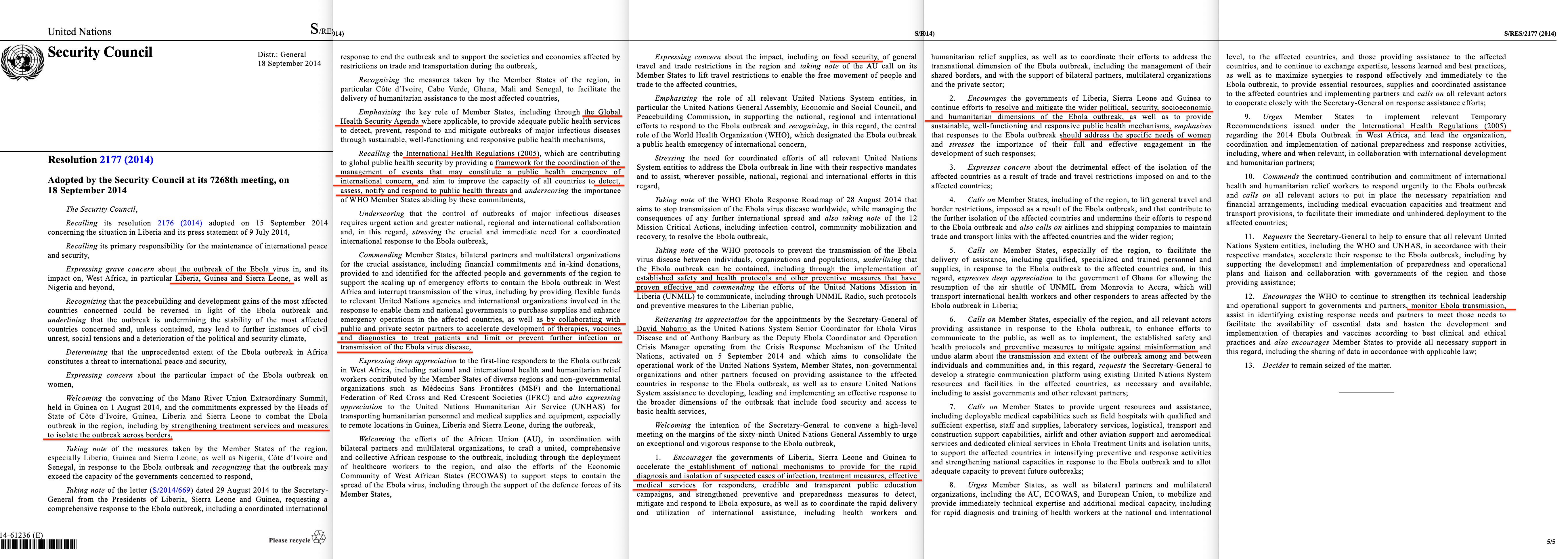

Resolution 217778 (2014) invoked Chapter VII binding authority for the Ebola outbreak, treating a virus with the same enforcement powers previously reserved for acts of war. Each resolution widened what qualifies as a security threat requiring binding international response. The Emergency Platform codifies this trajectory into permanent operating doctrine rather than episodic exception.

The determinants logic provides the cross-domain trigger mechanism. Once health, environment, inequality, and digital systems are defined as interdependent determinants of security — as Resolution 47/60 established and Our Common Agenda79 (2021) reinforced — the surveillance data generated by any single domain can qualify events for emergency declaration across all domains simultaneously.

Climate TRACE data showing accelerated emissions does not merely inform climate enforcement; it can contribute to a declaration of ‘complex global shock’ that activates financial, credential, procurement, and audit enforcement rails in parallel.

The domains do not merely share architecture — they provide mutual trigger conditions. Normal operation adjusts capital requirements incrementally; emergency operation activates the architecture as an enforcement mechanism under crisis authority.

The institutional genealogy of how this activation logic was constructed — from London clearing houses through Guild Socialist functionalism to the UN’s dual-layer constitutional architecture — is treated at length in prior essays.

Conclusion

The BIS Innovation Hub built a general-purpose control architecture and applied it first to climate. The pattern is now replicating across environmental domains — biodiversity, water, ecosystems — and preparing for social domains.

The BIS Finternet paper extends the architecture from institutions to individuals through digital identity. The June 2025 Annual Economic Report provides the integrating vision: a unified ledger hosting all forms of money, all forms of assets, and the programmable logic that governs their transfer.

The components are modular. Keystone standardises data across the system. AISE classifies any disclosure against any criteria. Rio monitors markets in real time. Aurora links institutional vision into a single analytical brain. Mandala compiles any rule into payment protocol. Rosalind enforces any condition through programmable locks. Nexus connects existing payment rails. Genesis and Dynamo collapse the entire chain into individual financial instruments. Pine places monetary policy on the ledger. Leap ensures the system survives quantum computing.

Climate was the proof of concept.

The seventeen Sustainable Development Goals constitute the full palette.

Each goal can acquire…

… scenarios that specify acceptable futures.

… taxonomies that classify compliant activities.

… disclosure frameworks that force reporting.

… AI systems that automate classification.

… surveillance that measures the gap.

… capital requirements that condition behaviour.

… programmable enforcement that executes compliance.

The architecture does not care what it optimises for. It requires only objectives that can be specified, data — synthetic or not — that can be collected, classifications that can be assigned, and consequences that can be encoded.

Seventeen goals. Seventeen modules.

One SDG machine.

...incredible details, escapekey... every word in their endless documents points to one simple concept... criminality!... 🙏➕🙏... ps too late at 03:26 to read much...

I got my drivers license renewed yesterday in Washington State. I do not have RealID and was keen not to have them give it to me ‘by default’ in the renewal process, never trusting the government in such matters. During the renewal process there was no mention of RealID, either verbally or in the paperwork, and unlike my renewal 6 years ago there were no propaganda posters on the wall. So I brought the topic up late in the process but before applying my signature, informing the Licensing agent that I did not want RealID. Her response was something like “oh no that’s not anything that’s included, it’s not required and is not mandated”. Compared to my last renewal it was as if RealID had been removed from the process(at least in my very Blue state). I was happy about that, and unlike last time I was able to get an optional 8 years ago license renewal(👍)

Just say No to Digital ID in all forms wherever and whenever possible