Ponzi Scheme

SpaceX went public on Thursday. By Monday evening, after-hours trading had pushed its market capitalisation past $3 trillion, surpassing Microsoft1.

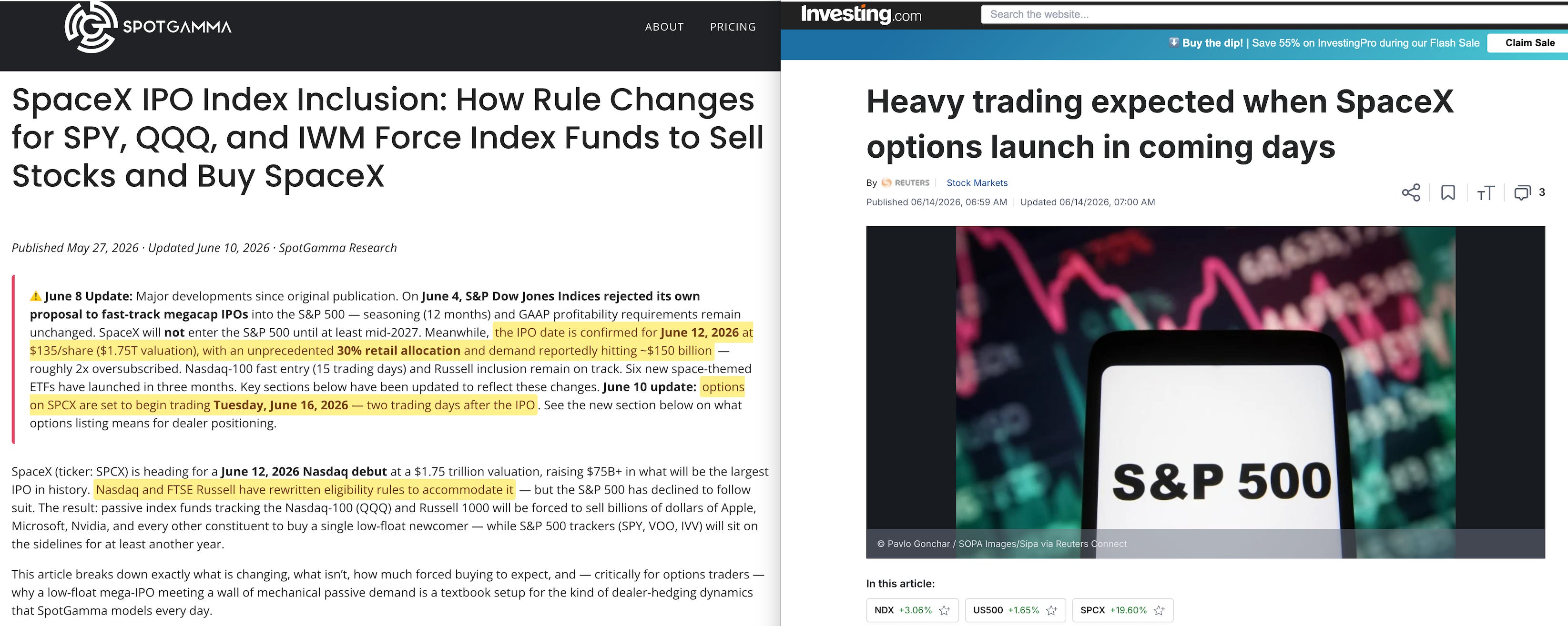

Options trading begins today, though the company lost $4.9 billion last year2.

Make sure you take that in.

First, the technicals. You can skip this if you prefer, it’s primarily there to establish how absurd the valuation is. It’s dot-com on steroids, if you will.

Revenue in 2025 was $18.7 billion, while the net loss was $4.9 billion3. Long-term debt stands at $29.1 billion, with an accumulated deficit of $41.3 billion4, and free cash flow in the first quarter of 2026 was negative $9.1 billion5. Starlink is the only profitable segment, making $4.4 billion in operating profit from $11.4 billion in revenue6. The xAI division — which includes X, formerly Twitter — lost $6.4 billion, while the space launch business roughly breaks even7.

At $3 trillion, the market values SpaceX at about 160 times its annual revenue. For context, Cisco at the peak of the dot-com bubble traded at around 30 times revenue8. SpaceX is valued at more than five times that multiple, yet the company has never turned a profit. Morningstar's most optimistic fair value estimate is roughly $780 billion9 — about a quarter of the current market cap10.

The S-1 filing describes the company’s total addressable market as $28.5 trillion11 — ‘the largest actionable total addressable market in human history’.

That’s a bold claim for a company burning through $9 billion a quarter.

The Options Chain

What happened on Monday evening was a gamma squeeze12. Market makers who’d sold call options had to buy the underlying stock to hedge their exposure. That pushed the price higher, which forced more hedging, which pushed the price higher still — a mechanical feedback loop with no connection to the company’s fundamentals.

Options trading opens today, creating leveraged exposure far beyond the $85 billion raised through the IPO13. A gamma squeeze on the stock alone is bad enough. Add options into the mix and everything gets amplified, because each layer of bets is built on top of the last. If the share price drops 50%, the losses don't stop at 50% — they multiply through the chain.

And the leverage isn’t the end of the story. If SpaceX eventually achieves S&P 500 inclusion — which requires twelve months of trading and GAAP profitability — index fund mechanics could trigger roughly $400 billion in passive buying. In the meantime, Nasdaq-100 and Russell inclusion alone would force an estimated $22–27 billion14.

Nobody chose to buy this. The money flows automatically because SpaceX ticked the boxes for index inclusion. The person whose pension is now invested in a loss-making company at 160 times revenue didn't make that decision, wasn't asked, and probably has no idea it's happened.

The Pension Fund Problem

This structure feels uncomfortably familiar in two ways. The valuation mirrors the dot-com bubble: companies with no earnings and endless ‘addressable markets’ kept afloat by incoming capital until the music stopped. But the end buyer has changed.

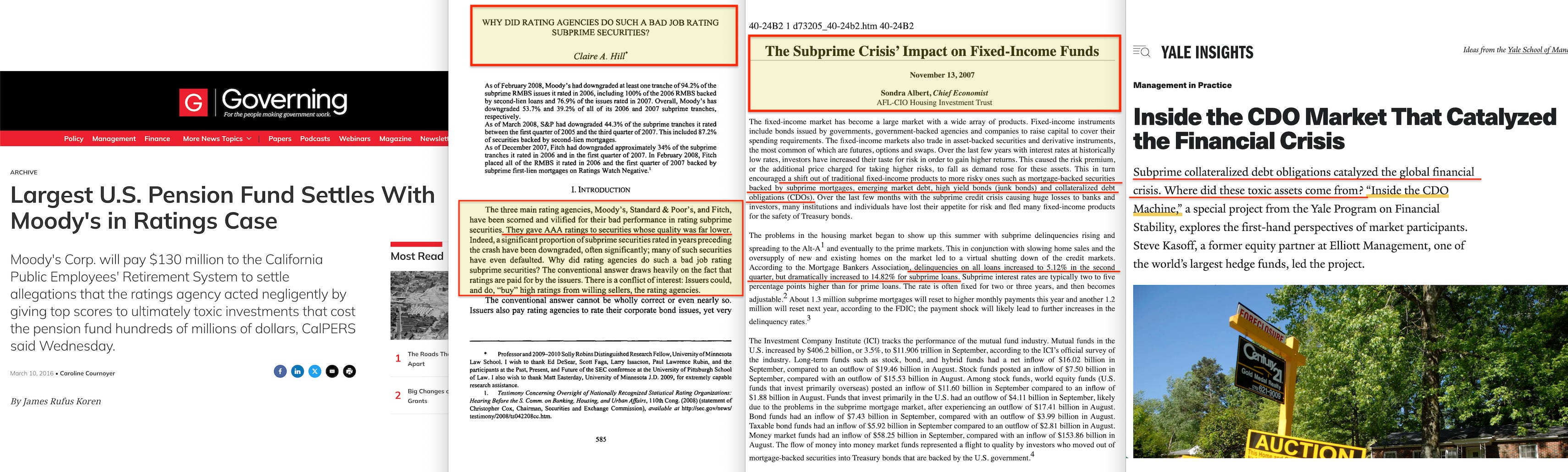

In 2007, a different piece of financial engineering — packaging subprime mortgages into products that got the highest possible safety rating — ended up in the same place SpaceX is heading now: pension funds. CalPERS, teachers’ retirement systems, municipal workers’ funds15 — all institutions legally bound to invest only in assets meeting certain ratings thresholds. The ratings agencies went along with it. The top slices of subprime mortgage pools got triple-A ratings, so pension funds could buy them, which meant more subprime mortgages could be originated, packaged, sliced, and sold16. The fresh money paid returns to those already invested. The rating was the green light, and the pension fund was where everything settled17.

SpaceX isn’t a CDO, but the pattern is similar18. The IPO creates the market. Options multiply the bets. The gamma squeeze — where hedging forces more buying, which forces more hedging — pumps the price. And index inclusion means pension funds and tracker funds have to buy it, regardless of whether the company makes money, simply because it meets the entry criteria. The early investors who bought in cheaply before the IPO are the ones whose holdings are now worth multiples of what they paid — not because the company became profitable, but because new money keeps arriving.

In a Ponzi scheme, existing investors get paid from new investors’ money rather than from the business’s actual profits19. SpaceX’s business lost $4.9 billion last year. The ‘returns’ being generated exist only in the share price, propped up by fresh capital flowing in through the IPO, the options chain, and — if inclusion happens — the index funds. Fresh money coming in pays the people already in, and the price stays high because of how the system is built — not because the company is worth what the market says it is.

What Happened Last Time

In 2008, the CDO market collapsed and subprime losses cascaded through the derivatives chain20. Pension funds took the hit, and ordinary people whose retirement savings had been put into triple-A-rated subprime products — without their knowledge or consent, through automatic investment rules and ratings thresholds — bore the losses.

But the crisis didn’t just destroy wealth — it built new architecture. Within three years, the institutional infrastructure of global finance — the Bank for International Settlements, the Basel Committee, the central bank supervisory network, the IMF conditionality framework — had been repurposed for a new regulatory agenda. The Network for Greening the Financial System was founded in 201721. The EU sustainability taxonomy was legislated in 202022. Macroprudential regulation — which barely existed before 2008 — became the dominant framework for financial oversight23.

But 2008 wasn't a one-off. It was the biggest in a pattern that's been repeating for over thirty years.

The Ratchet

Each crisis is treated as a one-off rather than part of a pattern — which is precisely why most people don’t notice the sequence.

The 1992–93 ERM crisis24 — when Soros broke the Bank of England25 — didn’t push countries back to floating exchange rates. It sped up monetary union. The Maastricht Treaty was already signed, and the crisis showed that partial integration was the problem. The answer was more integration.

The 1997 Asian financial crisis handed the IMF broader powers across East Asia26. Thailand, Indonesia, and South Korea had to privatise, open their capital accounts, and restructure their banks as conditions for emergency loans.

The 1998 collapse of Long-Term Capital Management set the template for the next decade27. Alan Greenspan’s Federal Reserve organised a private bailout, getting fourteen banks to pump $3.6 billion into a single hedge fund to stop systemic contagion. The precedent — that the central bank would step in to manage private sector failure — made the 2008 bailouts almost inevitable.

The dot-com crash28 and the Enron29 and WorldCom30 scandals produced Sarbanes-Oxley31, which didn’t just expand reporting rules but built ethical compliance into financial law — CEO and CFO certification, whistleblower protections, and a new oversight body, the Public Company Accounting Oversight Board32. Meanwhile, Greenspan cut rates from 6.5% to 1% to manage the dot-com fallout, which directly inflated the housing bubble that caused 2008 — a bubble Krugman had openly called for33. The regulatory response expanded oversight. The monetary response set up the next crisis.

The 2008 financial crisis created the Financial Stability Board34 — a new institution at the 2009 G20 London Summit with more power than the Financial Stability Forum it replaced — alongside Basel III, which tightened capital requirements and introduced new liquidity ratios across global banking. It also brought quantitative easing, near-zero interest rates, and a massive expansion of central bank balance sheets that was never reversed. The Bank of England’s gilt market holdings surged to 25% within months35. The Fed’s balance sheet grew from under $1 trillion to over $4 trillion by 201336. These were called emergency measures and became permanent.

The 2010–12 eurozone sovereign debt crisis created the Fiscal Compact37, the European Stability Mechanism38, the Banking Union39, the Single Supervisory Mechanism40, the Single Resolution Mechanism41, and ECB bond-buying programmes42 — six new layers of institutional control over national fiscal and banking policy, none of them directly accountable to voters.

The 2020 COVID crisis brought zero reserve requirements, direct fiscal monetisation on a scale that would’ve been unthinkable two years earlier, and faster digital payment infrastructure4344. Across the developed world, central banks funded government spending directly — a practical merger of monetary and fiscal policy without any formal institutional change.

No power was ever returned, no balance sheet normalised, and no emergency measure withdrawn. For over thirty years the direction’s been consistent: more conditions, more institutional authority, more domains covered. There’s never been less, never a return to the simpler system that existed before the crisis.

The 2022 UK gilt crisis showed the ratchet operating in real time. A decade of the Bank of England’s near-zero rates had forced pension funds into leveraged LDI strategies45 — £1.5 trillion in positions that depended on gilt prices not falling too fast. The vulnerability built up under the Bank of England’s own supervisory authority — its Financial Policy Committee existed specifically to spot exactly this kind of systemic risk. When Kwarteng’s mini-budget sent gilt yields spiking, the Bank simultaneously pushed gilt prices down through announced quantitative tightening sales, refused to call an emergency rate meeting, set a hard deadline on its rescue programme, and gave the Prime Minister three days.

The emergency intervention cost £65 billion — more than the £45 billion in tax cuts that were blamed for the crisis. Within six weeks, both the Chancellor and the Prime Minister had been removed from office — by a crisis Mark Carney and Andrew Bailey’s Bank of England had created and later escalated. The Fabian Society's proposal for monetary-fiscal coordination cites the episode six times46 — without assigning blame to the BoE47.

The crisis became the justification for ensuring fiscal policy could never diverge from monetary policy again, a course of action which in net effect transferred power over fiscal policy to the Bank of England.

What’s Waiting

In November 2023, the Fabian Society published ‘In Tandem: The Case for Coordinated Economic Policymaking’, written by Michael Jacobs, Robert Calvert Jump, Jo Michell, and Frank van Lerven of the New Economics Foundation48. The report proposes an Economic Policy Coordination Committee — an EPCC — that would formally merge monetary and fiscal policy, coordinating decisions between the Treasury and the Bank of England.

Business organisations, the Climate Change Committee, and various stakeholder bodies would take part. A ‘third way’, so to speak.

This would remove the last structural separation in economic governance. Since the postwar period, monetary policy has been run by independent central banks beyond electoral reach, while fiscal policy — taxing and spending — has stayed, at least nominally, under democratic control. The EPCC would coordinate both through a single technocratic framework, justified by the need to manage decarbonisation and financial stability at the same time.

The intellectual framework has been developed through NEF publications over the past decade: interest rates alone can’t manage inflation, fund the green transition, or maintain financial stability. What’s missing is the political mandate. And political mandates, historically, are produced by crises.

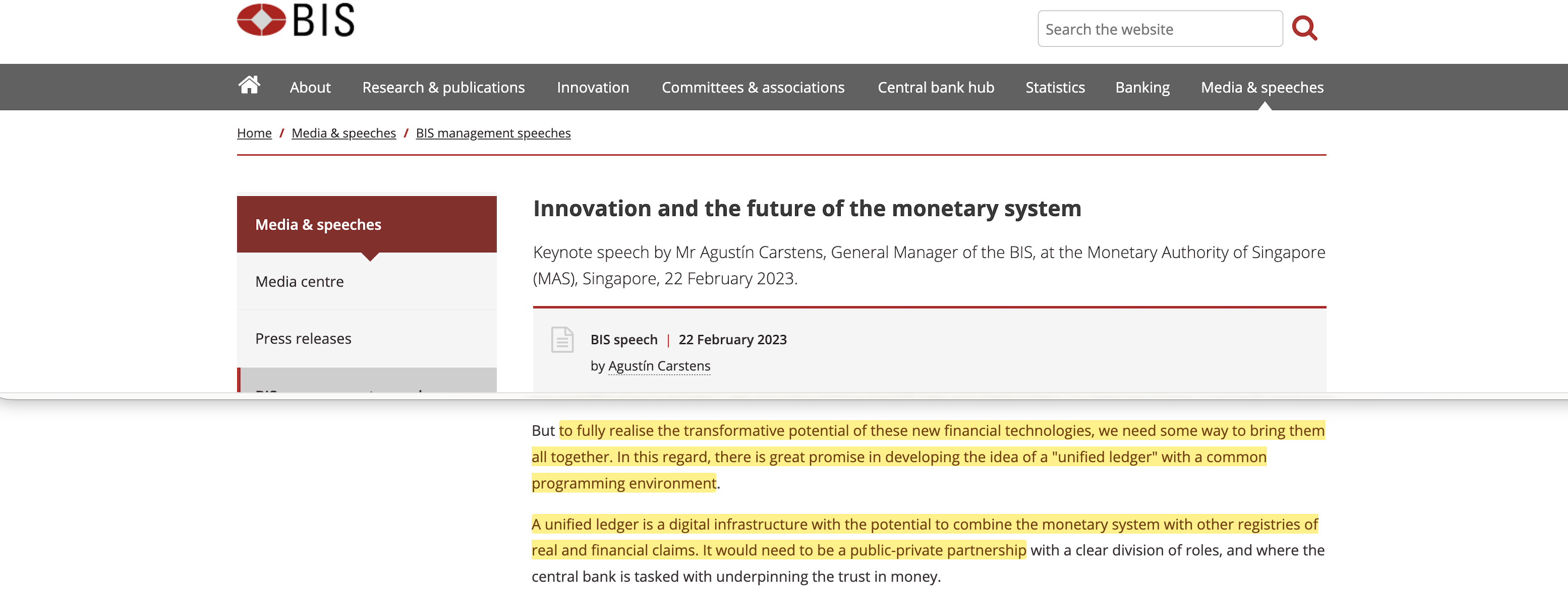

The institutional design isn’t the only thing already in place. Thomas Piketty’s programme — a global wealth registry, total financial visibility, and central bank accounts for every citizen — provides the intellectual justification that would become politically irresistible after a severe enough crash. Billionaires cashing out while pensions are wiped out is the inequality narrative that demands transparency, and transparency at that scale needs the very infrastructure the BIS has already blueprinted through its Innovation Hub — mBridge for programmable settlement, Helvetia for tokenised capital markets, Genesis for automated compliance, and Nexus for retail integration. The branding’s already chosen: ‘Inclusive Capitalism’.

The opacity of the current settlement system — where pension fund capital can be put into a loss-making company at 160 times revenue through mechanical index buying, without the pension holder’s knowledge — is exactly the problem the BIS’s unified ledger is designed to solve: all assets tokenised, all transactions recorded, all compliance verified in the code itself.

BIS General Manager Agustín Carstens has stated explicitly that the Innovation Hub projects need 'some way to bring them all together' — the unified ledger is that integration layer49.

But tokenisation doesn’t just make settlement transparent. It makes the legal gap between ownership and entitlement programmable. Your bank deposit’s already a loan to the bank, not your property. Your brokerage holdings are ‘security entitlements’, not assets you own. When a bank fails, derivatives counterparties get paid first under safe harbour provisions, before ordinary depositors even enter the queue. On a tokenised ledger, that resolution would settle in a microsecond — instant, irreversible, and complete before anyone could react.

A financial crash severe enough to wipe out pension fund holdings, destabilise the derivatives market, and show that the existing separation between monetary and fiscal authority is ‘inadequate’ would create exactly the conditions where coordinated economic policymaking becomes not just attractive but apparently necessary.

‘This must never happen again’ is the sentence that installs the architecture.

Zero Reserves

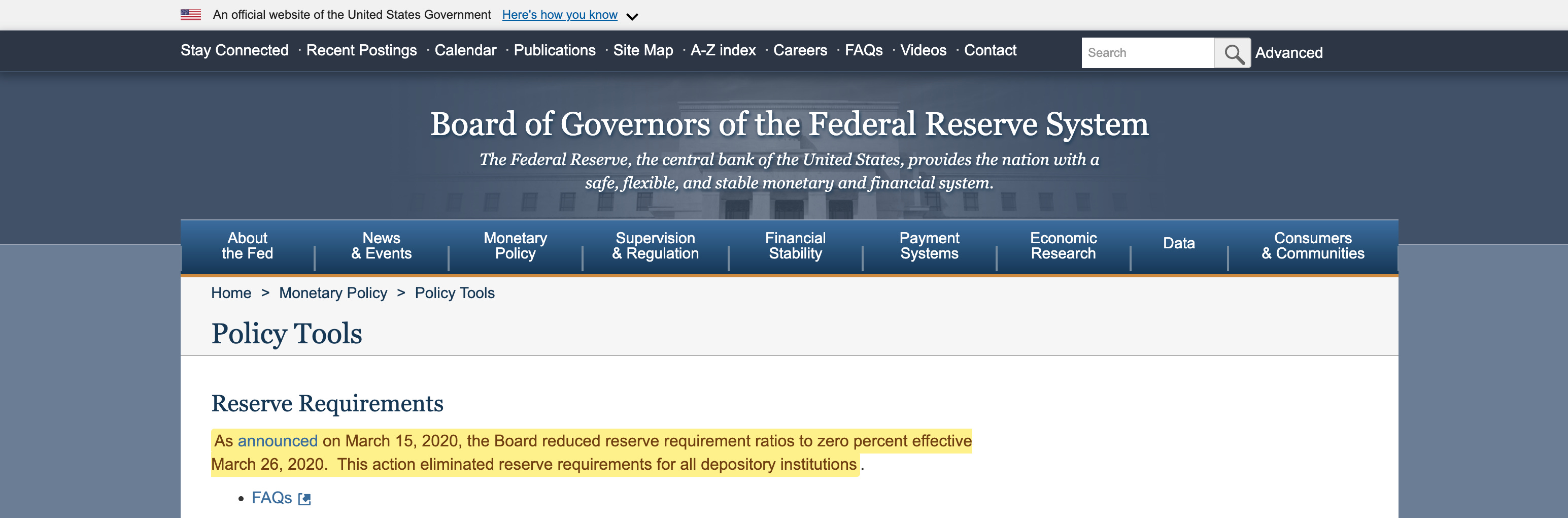

One detail rarely gets mentioned in financial commentary because of the implications. On 26 March 2020, the Federal Reserve cut reserve requirements for all depository institutions to zero per cent50, and they’re still at zero today.

American banks aren’t required to keep any fraction of deposits in reserve. With no reserve ratio, there’s no mathematical limit on credit creation through lending — the money multiplier is effectively infinite51. Capital requirements and liquidity ratios are practical constraints, but the reserve constraint has been removed entirely.

A $3 trillion valuation on a loss-making company, sustained through leveraged derivatives and mechanical index buying, wouldn’t be possible in a system with meaningful reserve constraints. It’s an artefact of an architecture running with no reserves, no friction, and no limit on how much credit the system can generate against how little collateral. When the bubble pops, the absence of reserves means there’s nothing to absorb the losses, which makes the crisis deeper, the call for central bank intervention louder, and the political mandate for the next layer of architecture stronger. The constraint was removed during a crisis in 2020 and was never restored.

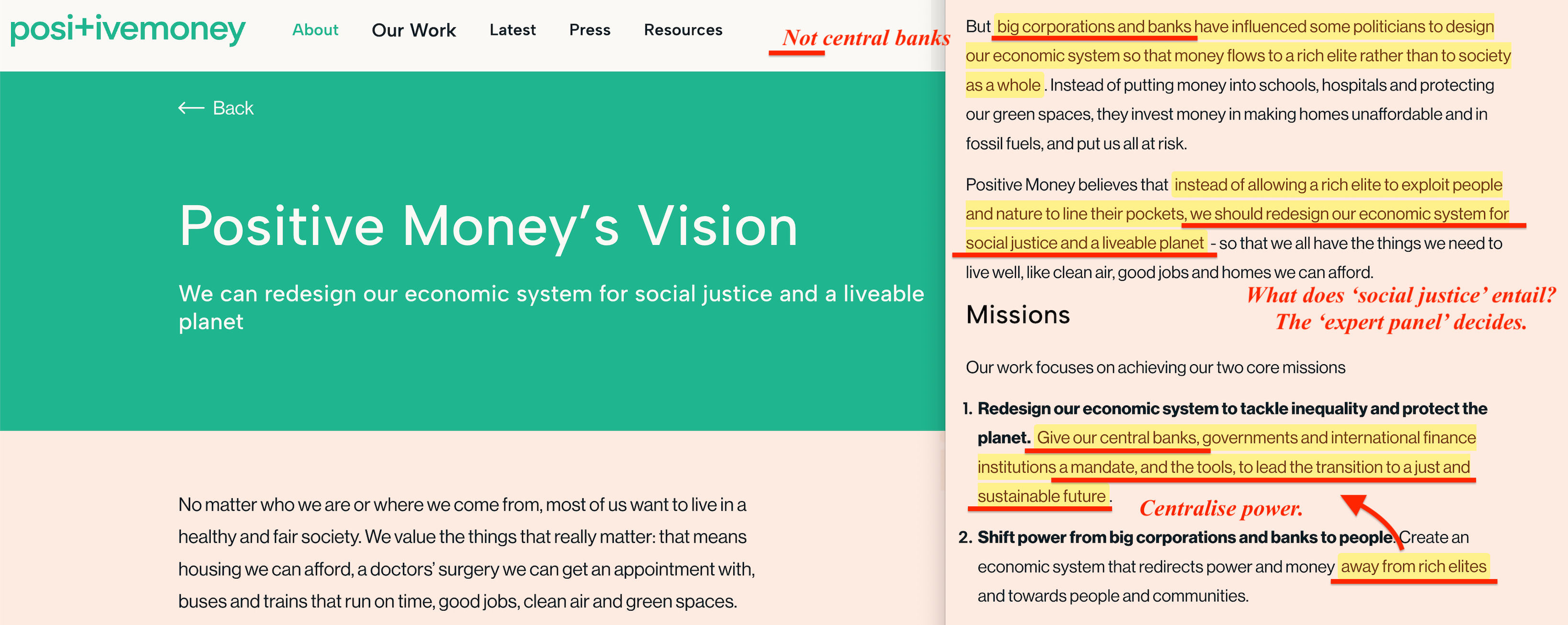

The narrative that follows the next crash is already clear: the banks were irresponsible, they were creating money from nothing, they had no reserves. The solution, when it arrives, will be to centralise money creation with the central bank — precisely the programme that organisations like Positive Money have been advocating for years52.

It sounds progressive, but its structural outcome is a central bank monopoly on money issuance, placing total control of the money supply with the same institutions that lowered the reserve ratios to zero in the first place. The ratchet turns in one direction — remove the constraint, inflate the bubble, let it pop, blame the banks, and centralise further, while the central banks shoulder no responsibility for the problem they caused — exactly as we saw when Truss and Kwarteng were removed.

The Pattern

SpaceX at $3 trillion while losing money is a familiar pattern: inflated valuations kept going by automatic inflows, leveraged through derivatives, with pension funds as the end buyer and the public left holding the bag. The last time this pattern collapsed, it produced a decade of institutional expansion that put financial governance further beyond democratic reach than at any point since the postwar settlement.

The company’s own S-1 filing accidentally confirms the absurdity53. $28.5 trillion in ‘total addressable market’54. Revenue of $18.7 billion. A net loss of $4.9 billion. And a valuation that exceeds the GDP of every country on earth except the United States and China.

The conditions are set, the options chain is built, and the index inclusion criteria will determine what up to $400 billion in pension fund capital buys next. The ordinary investor doesn’t notice any of this until they check their pension.

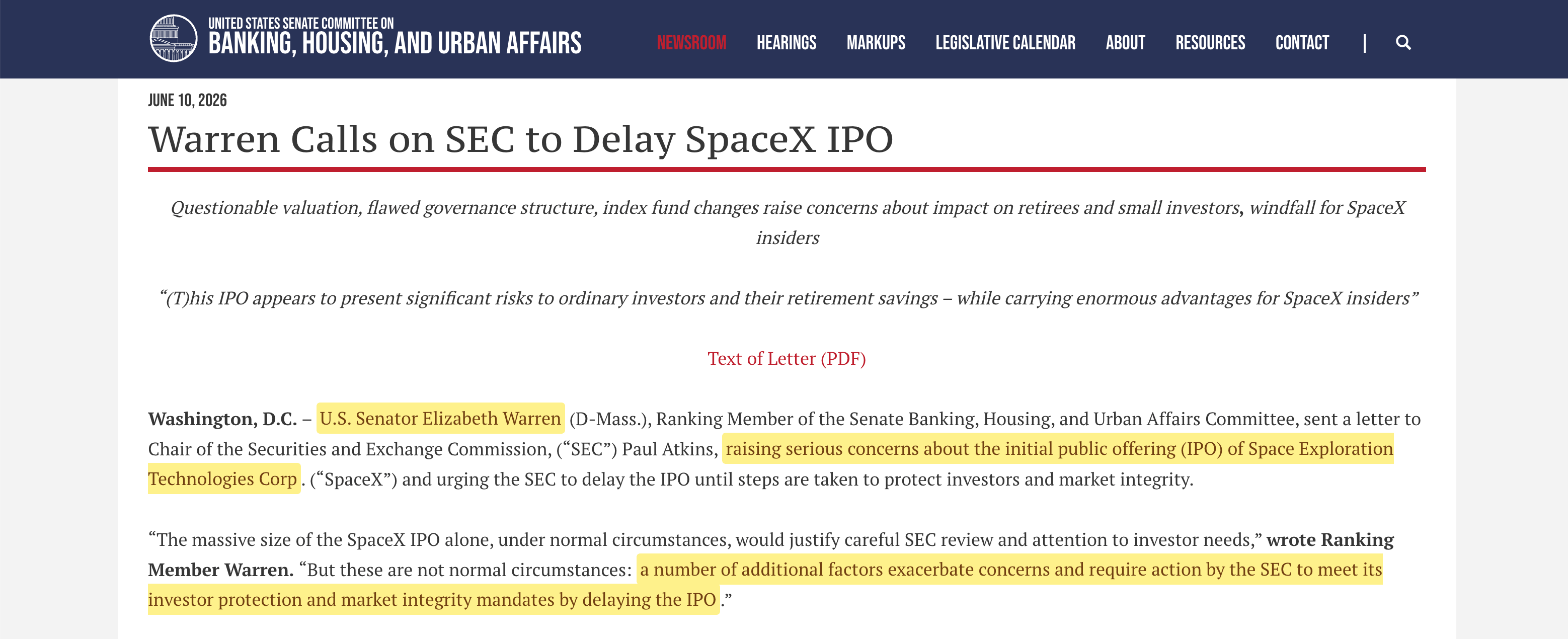

Senator Elizabeth Warren — whatever one might otherwise think of her55 — has already written to the SEC flagging exactly this concern56 — the dual-class structure, the valuation, and the forced buying through index funds. Nasdaq and FTSE Russell reportedly rewrote their index inclusion rules to fast-track the process57.

At least one European pension fund has already blacklisted SpaceX entirely58, concluding that its value ‘cannot reasonably exceed USD 1 trillion’ under any scenario. The fact that a pension fund must actively opt out to avoid being forced in is proof of the mechanism.

After the crash, every component’s already in place:

A central bank monopoly on money creation (Positive Money)

Formal integration of monetary and fiscal policy (In Tandem; EPCC)

A unified ledger with every asset tokenised (Maxwell; BIS/Joi Ito/Epstein)

Programmable settlement with compliance verified in the code (Project Rosalind)

A global wealth registry (Thomas Piketty)

Bail-in powers that execute at the speed of code (Beyond Great Taking)

Digital identity tied to every transaction (Clare Sullivan)

An ethic no one can reasonably challenge (Any Old Ethic Will Do)

Together, they create a financial system where every economic activity sits on the ledger, every transaction needs approval, and no one can appeal the terms. The same unelected body coordinates both monetary and fiscal policy — a closed system of total economic governance beyond democratic reach, operated through a clearinghouse, enforced in the name of whatever ethic is installed at the time, be it planetary stewardship, social justice, racial purity, or even Silly Hat Thursdays59.

The intellectual justification’s published, the institutional design’s specified, the technical infrastructure’s built, and the branding’s chosen — Inclusive Capitalism60.

Any politician who dares to stand up to the architecture can suffer the same fate as Truss and Kwarteng in a heartbeat. All that’s missing is the mandate — and a crisis provides exactly that.

Find my Telegram channel over here.

Latest archive update. Includes all essays through 06-22-2026, Full and Lite versions, full-text search. Start with README. https://transfer.it/t/IYW0vfoXzRLC

SpaceX ≈ Vaporware.

This essay actually contains a mini crash course 'finance & investment for dummies', if you also read the links in the footnotes.

What ESC highlights briefly below: https://escapekey.substack.com/i/202242881/what-happened-last-time, is something I have experienced firsthand.

My neighbour's partner - a mathematician, worked at the largest bank in my country as a developer of (complex) investment products, which were forced down the throats of wealthy private clients. As a result of the financial (banking) crisis, countless private clients lost their pension pots. This cost the aforementioned partner his relationship, because his then-girlfriend could not live with someone who actively contributed to the exploitation of unsuspecting private individuals.

During that same period, I worked as a project manager at a corporate DFS provider. Clients consisted mainly of insurance companies, mortgage lenders, and similar financial institutions. Consequently, I also had to deal with the then-new Basel III regulatory framework.

Have a laugh: https://digitalfinance.worldbank.org/topics/dfs-overview

"A financial crash severe enough to wipe out pension fund holdings, destabilise the derivatives market, and show that the existing separation between monetary and fiscal authority is ‘inadequate’ would create exactly the conditions where coordinated economic policymaking becomes not just attractive but apparently necessary.

‘This must never happen again’ is the sentence that installs the architecture."

There's your '𝗢𝗿𝗱𝗼 𝗮𝗯 𝗰𝗵𝗮𝗼 (𝗰𝗿𝗲𝗮𝘁𝘂𝘀)'.