The Monetary Allocation Committee

In 2013, a think tank from London proposed a new public body to decide how to spend the money central banks create. The New Economics Foundation1 called it the Monetary Allocation Committee in a report titled Strategic Quantitative Easing2.

It would sit alongside the Bank of England’s Monetary Policy Committee but with a different job: while the MPC decided how much money to create, the Monetary Allocation Committee would decide where it went.

The report came out eighteen months before Mark Carney’s ‘Tragedy of the Horizon’ speech3, two years before the Paris Agreement4, and four years before the Network for Greening the Financial System was founded5. The body to direct centrally created money was designed before the ‘voluntary’ rules that would eventually make that direction compulsory.

That framework’s now largely built. The question’s how, and by whom.

Executive Summary

In 2013, the New Economics Foundation proposed a Monetary Allocation Committee — a public body that’d decide where money created by central banks flows. The proposal was built to accept any purpose, and the ‘green’ objective was attached four years later. The coordination body was proposed under four names — the Monetary Allocation Committee (2013), the Green Finance Action Taskforce6 (2021), the Economic Policy Coordination Committee7 (2023), and the European Economic Coordination Council8 — scaling from UK domestic to continental, each time structurally identical.

One author, Frank van Lerven9, connects all three UK proposals through documented co-authorship: the monetary creation reform10 (Positive Money, 2018), the integrated green finance programme with its coordination body11 (NEF/Positive Money, 2021), and the formal fiscal-monetary coordination proposal12 (Fabian Society, 2023). Between 2016 and 2023, van Lerven published across every functional layer of UK central bank and coordination policy — sovereign money, capital requirements, credit guidance, collateral framework, fiscal rules, tiered reserves, and the coordination body itself13. By 2022, the ECB had begun implementing the collateral framework reform his INSPIRE-funded paper specified14.

The domestic programme was built in parallel with an international enforcement architecture — specified at seven private forums at the Rothschild family estate between 2014 and 201815, funded by the Rothschild and Generation Foundations, producing the TCFD and NGFS before either publicly existed1617. The same foundation network that funded the science (ICSU, SCOPE), the models (IIASA), the forums (Waddesdon), the academic papers (NEF, UCL, INSPIRE), and the advocacy programme (Positive Money, NEF, Fabian Society) also funds the civil society organisations that define the ‘social good’ the content-agnostic mechanism is supplied.

The programme’s documented end point is the centralisation of credit in an operationally independent central bank, allocated by a coordination body whose objectives originate with a foundation-funded advocacy network, conditioned on compliance with criteria the same network defined, settled on programmable rails, and withdrawn from anything a scenario model designates as non-compliant.

The elected government’s role is to transmit those objectives through remit letters it didn’t draft. The conditional infrastructure already exists — the Financial Action Task Force has in effect attached conditions to money since 198918. What the programme adds is the expansion of those conditions from criminal compliance to climate compliance, and from climate to biodiversity, social impact, and whatever comes next1920.

Simply put: a small network of think tanks and foundations designed the mechanism that directs where money flows. The mechanism was built to accept any ‘ethical’ purpose; the purpose was supplied by the same foundations that funded its design. The enforcement runs through banking regulations no parliament voted on, scenario models no borrower can challenge, and programmable settlement rails that check compliance before a transaction clears.

The elected government’s role in this architecture is to sign the paperwork.

The Educational Base

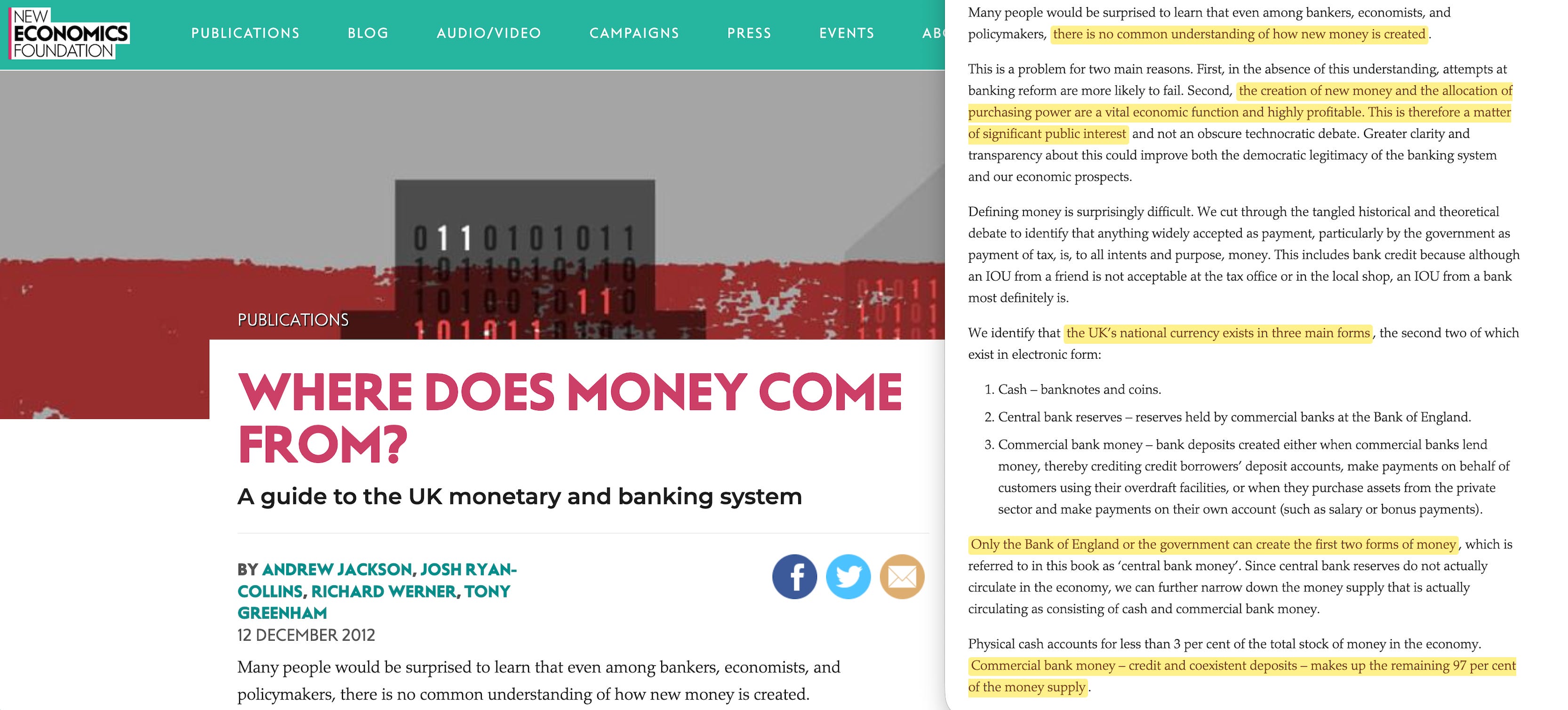

The story begins with a textbook. In 2011, Josh Ryan-Collins and three co-authors published Where Does Money Come From?21 through NEF. The book made a claim most economics graduates had never heard: commercial banks create most of the money supply when they lend, and the Bank of England’s role is far smaller than people think.

The Bank of England confirmed this in its 2014 Q1 Quarterly Bulletin22, using the same explanation23. But the NEF book had already been out for three years, and by then it had become the key text for a separate campaign. Positive Money, a not-for-profit group founded in 201024, used its arguments to push for ‘sovereign money’ — a system where the central bank, not commercial banks, would be the only creator of money.

The practical implication was simple: if the central bank controlled money creation directly, someone would have to decide what that money was for.

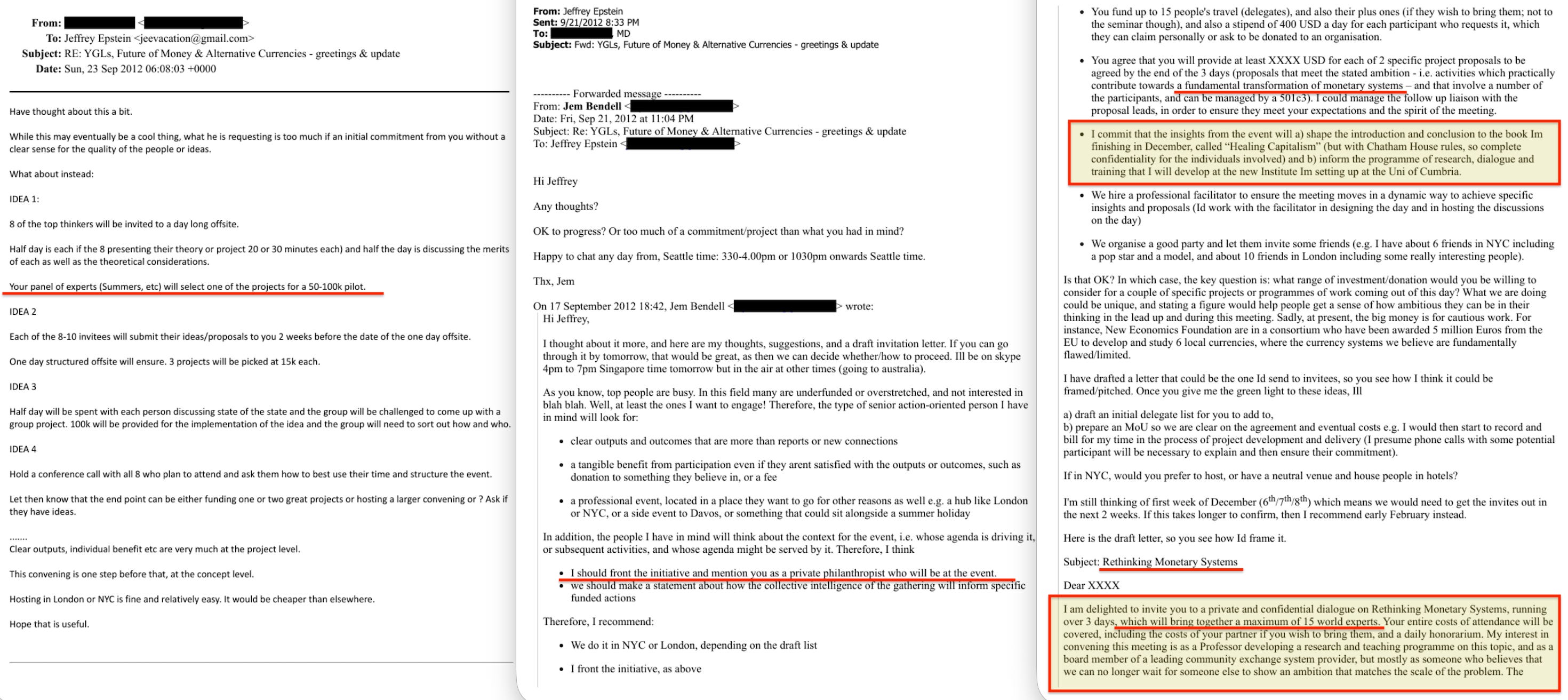

The currency innovation network also had a less visible channel. In September 2012, Jem Bendell — a Professor of Sustainability Leadership25 who the World Economic Forum had just named a Young Global Leader for his work on currency innovation26 — was approached by Jeffrey Epstein to run a private initiative on alternative currencies27. Bendell’s plan proposed fifteen ‘world experts’ meeting under Chatham House rules, with Bendell offering to ‘front the initiative’ and describe Epstein only as ‘a private philanthropist’.

Bendell has said the initiative didn’t reach agreement28. Regardless of whether it did, the institutional connections are documented: Bendell founded his Institute for Leadership and Sustainability (IFLAS) at the University of Cumbria that same year29, and IFLAS later supervised doctoral research on complementary currencies30 managed through NEF’s Community Currencies in Action programme31 — placing currency innovation research inside the network that would produce the Monetary Allocation Committee the following year.

Bendell later advised the Labour Party leadership during the 2017 general election32, and in 2021 published a paper through IFLAS arguing that monetary reform was the only viable response to pandemic-era public debt33.

The Green Precursor

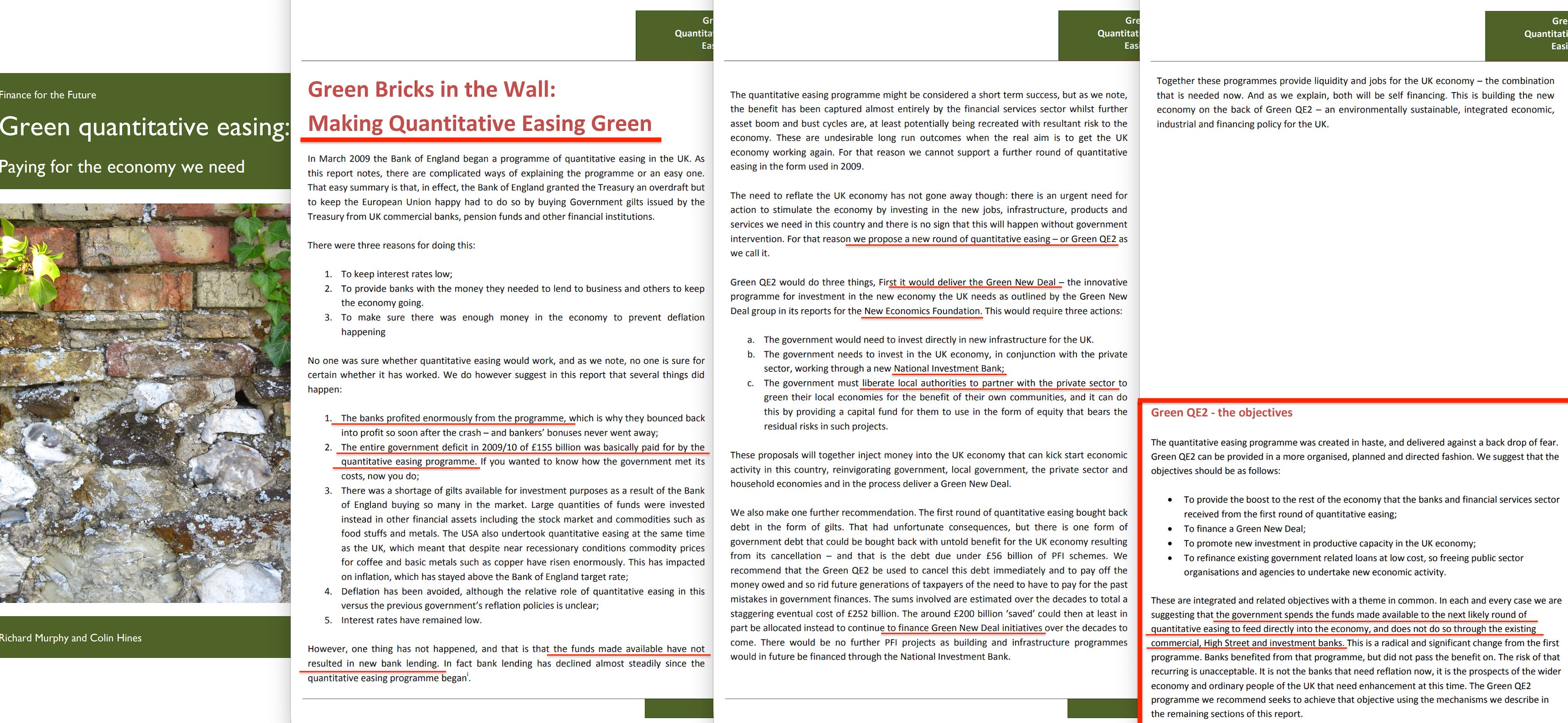

A year before Where Does Money Come From?34, Richard Murphy and Colin Hines published Green Quantitative Easing: Paying for the economy we need35 through their Finance for the Future partnership36. Their paper argued that if the Bank of England could create hundreds of billions to buy government bonds under ordinary QE, that same power could fund green infrastructure instead.

Murphy and Hines were in the Green New Deal group37, which had published its founding report through NEF in 2008. Green QE38 was the financing mechanism — the part that made the programme fundable. But it lacked allocation governance. It said the money should go to green investment without saying who’d decide what qualified, or how the boundary between monetary and fiscal policy would work.

Ryan-Collins filled that gap in 2013.

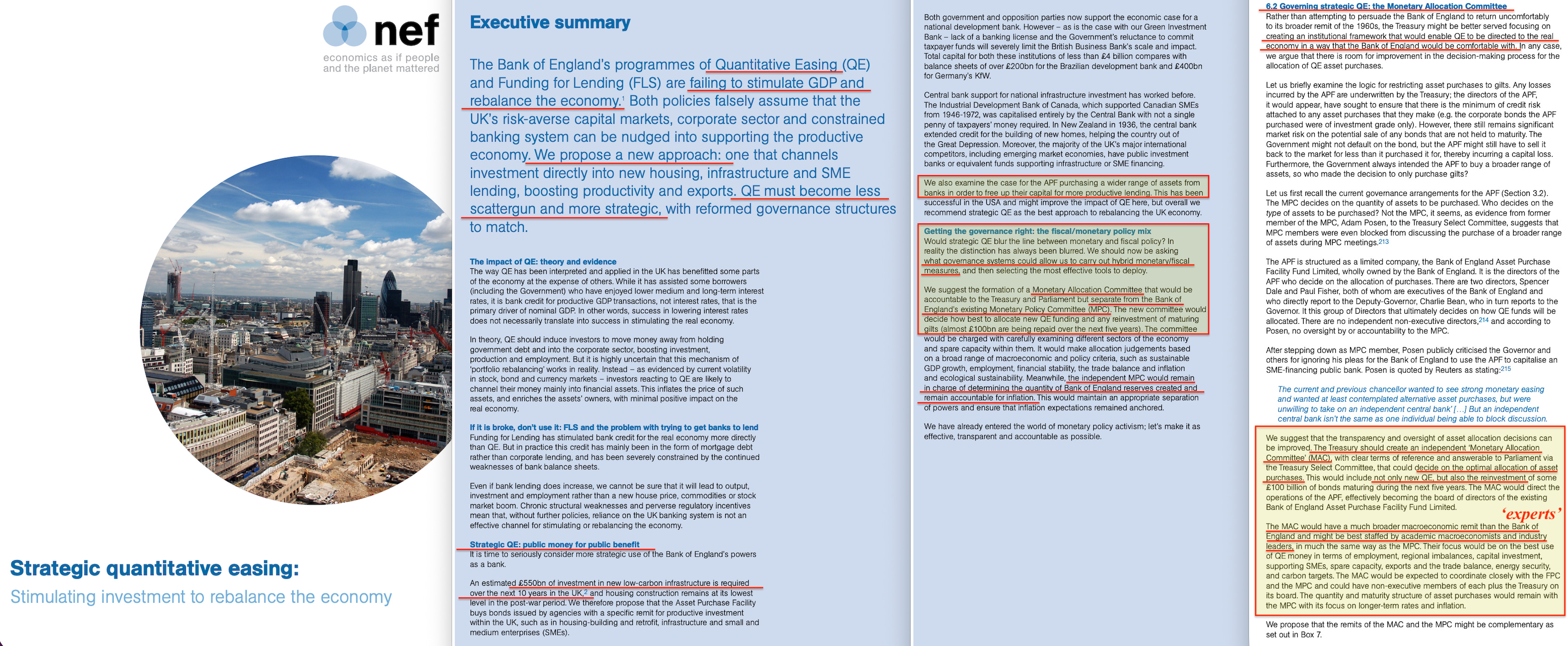

The Mechanism

The Strategic Quantitative Easing39 report said the Bank of England’s Asset Purchase Facility should buy bonds from agencies tasked with productive investment — housing, infrastructure, and lending to small and medium enterprises. The money would flow through public intermediaries like a national development bank, instead of going through commercial banks.

The new governance idea was the Monetary Allocation Committee. Ryan-Collins suggested splitting monetary policy in two: the Monetary Policy Committee40 (MPC) would still control how much money was created, while the new committee would decide where it went. This committee would answer to the Treasury and Parliament, stay separate from the MPC, and make allocation decisions based on macroeconomic criteria including ‘sustainable GDP growth, employment, financial stability, the trade balance and inflation and ecological sustainability’41.

The allocation body was meant to be content-agnostic. Its initial job was ‘economic rebalancing’, not decarbonisation. The green objective was just one criterion among several, not the committee’s whole reason for existing.

The split between who decides the quantity and who decides the allocation matched exactly the distinction between ‘goal independence’ and ‘instrument independence’ that already shapes central bank governance under the 1998 Bank of England Act42. The government formally sets the Bank’s objectives through the Chancellor’s remit letter; the Bank decides how to hit them. Ryan-Collins was proposing to formalise a second body on the allocation side of a distinction that existing legislation already made. But the documented sequence goes back a step further: the objectives in the remit letter are themselves shaped by the advocacy programme — the open letters, policy reports, and forum recommendations — that the foundation-funded network produces.

The government transmits; it rarely originates.

The distinction between transmission and independent evaluation falls apart on inspection, because the network funded the entire knowledge infrastructure a government would use when forming an independent view: the scenarios (NGFS, built on IIASA-lineage models43), the disclosure frameworks (TCFD, specified at Waddesdon44), the academic literature (co-authored by the same researchers through NEF and UCL IIPP), the risk assessments (Basel, incorporating NGFS scenarios45), and the scientific base itself (ICSU and SCOPE, funded by the same foundations46).

A Treasury official ‘independently evaluating’ the case for green mandate reform would read papers written by the network, assess risks modelled by the network, and apply frameworks designed by the network.

The well from which the government drinks was dug by the people who proposed the plumbing. And the same foundations that funded the knowledge infrastructure also fund the civil society organisations that define what counts as ‘social good’ — the ethic that the content-agnostic mechanism is supplied with. The Rockefeller Foundation, for instance, has funded ICSU and SCOPE (the science), IIASA (the models), Bellagio (impact investing), and the SDG Philanthropy Platform (the objectives). The funders that built the mechanism also supply the purpose the mechanism serves.

The Parallel Architecture

While NEF was designing the domestic allocation mechanism, a separate but overlapping network was building the international enforcement infrastructure that would eventually make directed allocation compulsory.

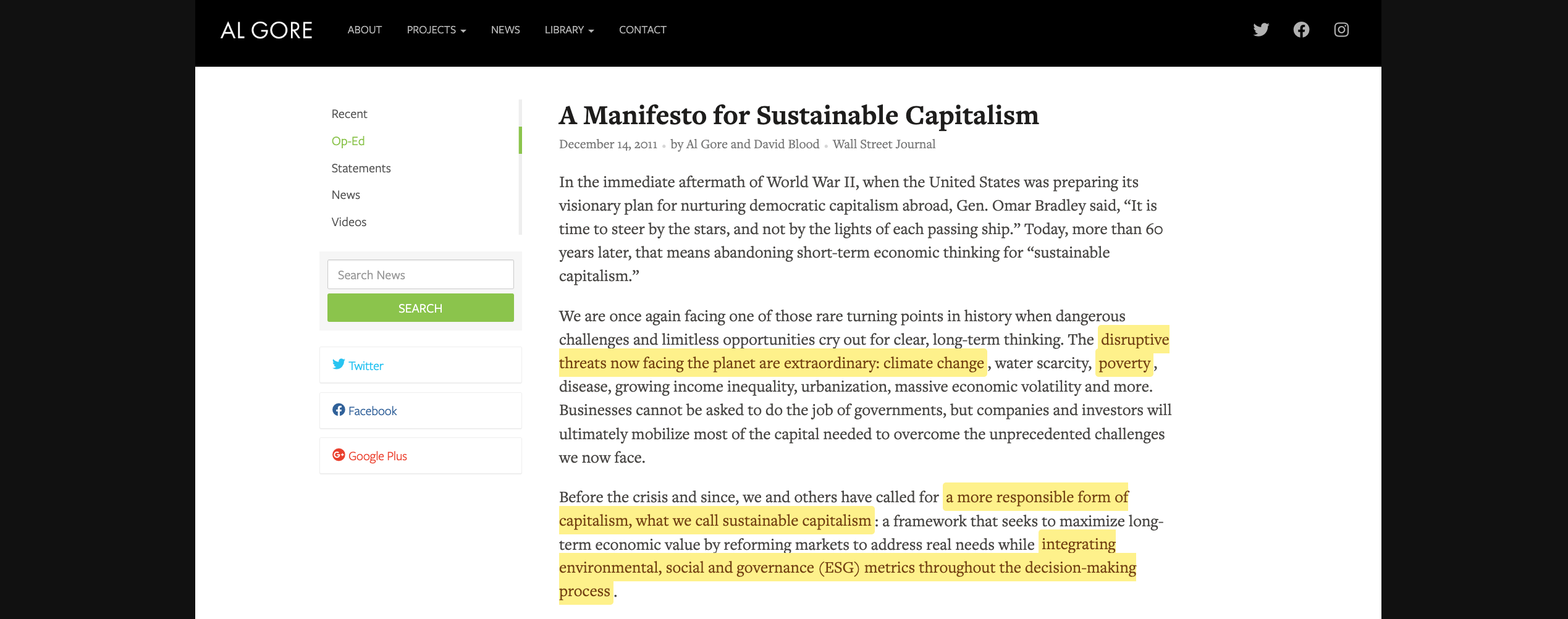

The stranded assets argument47 — that fossil fuel reserves on company balance sheets would have to be written off if governments enforced their climate commitments — came from Nick Robins and Mark Campanale at Henderson Global Investors in the early 2000s48. In 2011, Campanale founded Carbon Tracker and published Unburnable Carbon. That same year, Gore and Blood published A Manifesto for Sustainable Capitalism49 in the Wall Street Journal, and their Generation Foundation50 co-funded the Oxford Smith School’s Stranded Assets Programme alongside the Rothschild Foundation.

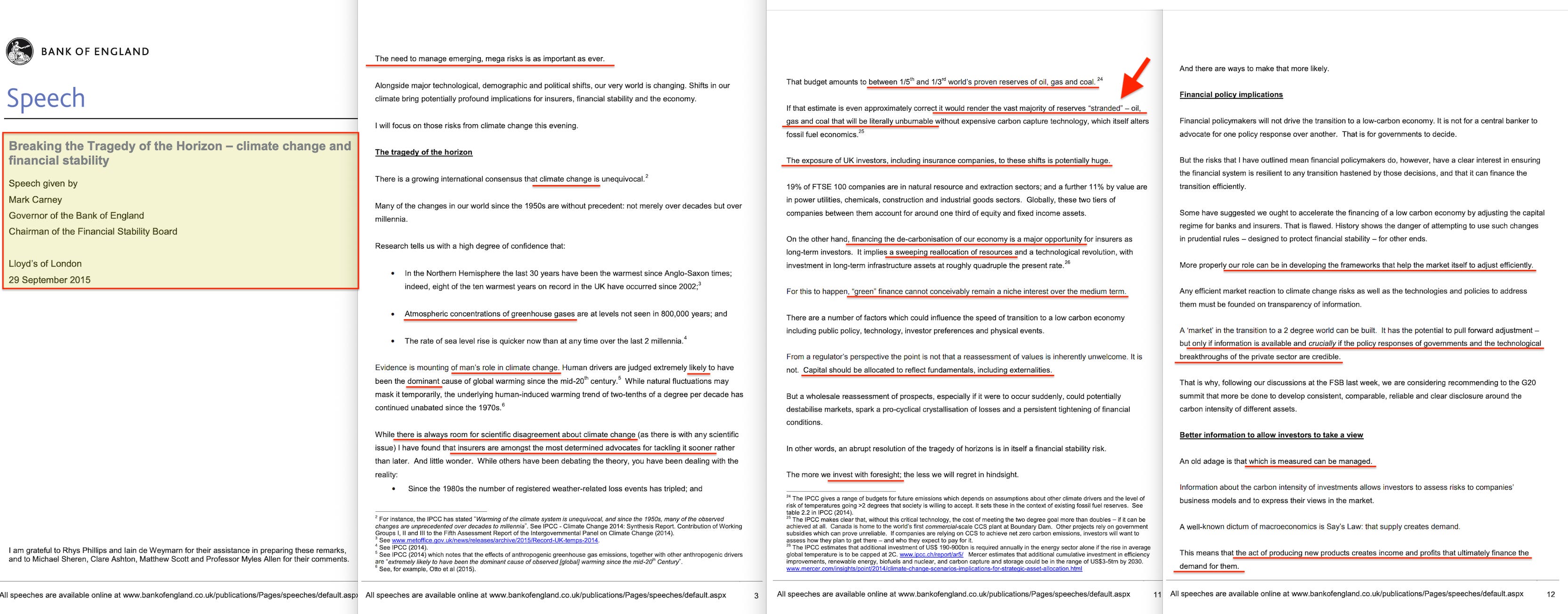

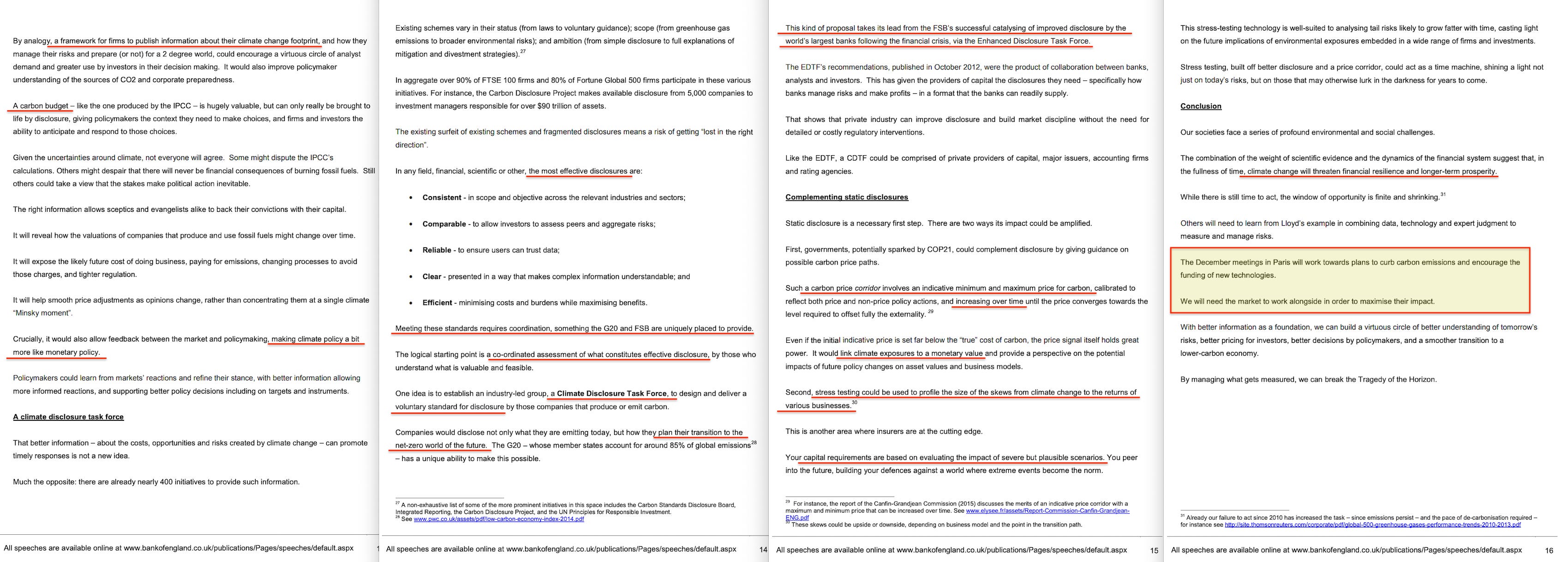

Between 2014 and 2018, the Smith School held seven private forums at Waddesdon Manor, the Rothschild family estate. The proceedings show how the regulatory framework for climate-related financial risk was built — from identifying ‘First Mover Disadvantage’ and specifying stress-testing tools (Forum 1, March 201451), through weaponising fiduciary duty (Forum 2, September 201452), to bringing central bankers and regulators into the room (Forum 4, October 201553).

The science behind these forums had its own funding trail. The International Council for Science (ISC)54, which defines what counts as ‘the best available science’ for policymakers, and its programme SCOPE55, which quantified the biogeochemical cycles — carbon, nitrogen, water, phosphorus — that the climate scenarios model, were both funded by the Rockefeller Foundation. The same foundation network that paid to measure the problem also paid for the forums that specified the regulatory response.

The Smith School’s July 2014 working paper had already laid out the three channels of climate risk — physical, transition, and liability56 — that Carney’s ‘Tragedy of the Horizon’ speech would introduce at Lloyd’s of London fourteen months later, in September 2015. The TCFD launched in December 2015; the NGFS launched in December 2017. Both were specified at Waddesdon before they existed.

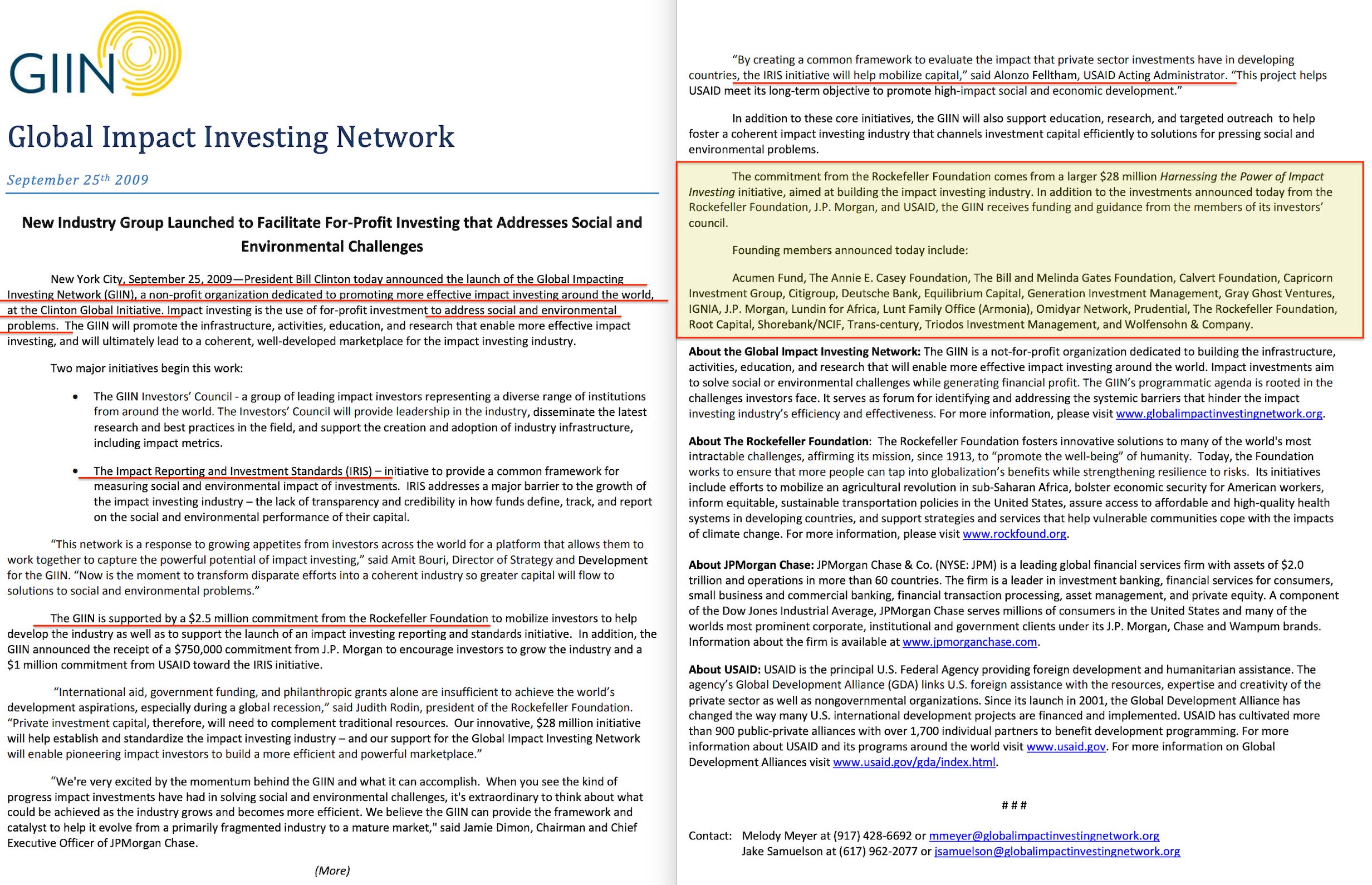

‘Impact investing’ was coined at the Rockefeller Foundation’s Bellagio Center in October 200757. The framework was published in 2009 through the Global Impact Investing Network at the Clinton Global Initiative, backed by JPMorgan, the Rockefeller Foundation, and USAID58. In May 2014, the Conference on Inclusive Capitalism met at the Mansion House, co-hosted by the City of London Corporation and E.L. Rothschild59. Mark Carney, Christine Lagarde, and Bill Clinton were among the speakers — central bankers, the IMF, and the political establishment sharing a platform on purposive capital under the Rothschild banner60. In December 2020, the Council for Inclusive Capitalism with the Vatican launched, adding papal authority to the framework61.

In Britain, the same architecture appeared under a Conservative label: Cameron’s Big Society62 (2010), Big Society Capital63 (2012), the Social Value Act64 (2012), and the G8 Social Impact Investment Taskforce65 (2013). Documents released by the US Department of Justice show Epstein tracking this infrastructure in real time. A March 2013 memo to Boris Nikolic — Bill Gates’s chief science and technology adviser — listed the UK’s pioneering social impact bonds alongside ‘govt approved special gates bonds’ as a proposed instrument66.

Social investment, impact investing, and blended finance are different labels for the same underlying arrangement — purpose-directed capital with a public-sector risk backstop and a foundation-funded civil society body specifying the purpose.

The label changed with each government, but the arrangement remained the same.

The Specification

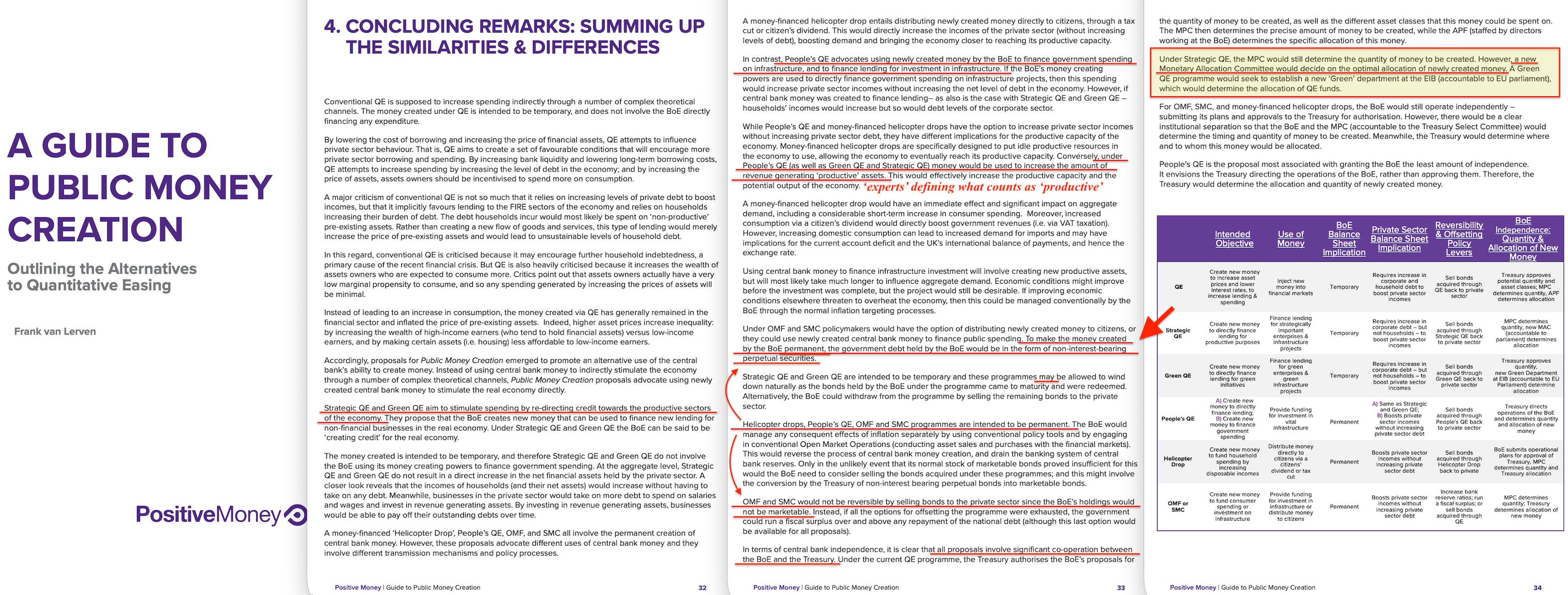

In 2016, Frank van Lerven published A Guide to Public Money Creation67 through Positive Money. He’d joined the organisation as a Research and Policy Analyst after working at the United Nations Development Programme68, and the report was the most comprehensive survey of public money creation proposals to date.

It assessed five proposals — Strategic QE, Green QE, Helicopter Drops, People’s QE, and Sovereign Money Creation — against a seven-aspect framework. The seventh aspect, ‘Impact on Central Bank Independence,’ split into two questions:

Who determines the quantity of new money to be created?

Who determines how the new money is allocated?

Van Lerven formalised the Ryan-Collins governance split as the organising principle of the entire field, with every variant of public money creation differing mainly in how it answered these two questions.

That same year, van Lerven co-authored a peer-reviewed paper in the Cambridge Journal of Economics with Ben Dyson and Graham Hodgson — ‘A response to critiques of full reserve banking’69 — defending the sovereign money system where banks are stripped of money creation power. Under sovereign money, all money is created by the central bank, so the allocation question becomes mandatory — someone must decide where it goes.

Sovereign money is the theoretical basis for central bank digital currencies70: a digital pound issued by the Bank of England, replacing the money creation function currently performed by commercial banks, would implement the proposal on programmable digital rails. Positive Money has since submitted formal responses to the Bank of England’s digital pound consultation, advocating for a publicly issued digital currency operated through Digital Cash Accounts71. In June 2023, the Bank for International Settlements published its blueprint for the future monetary system72 — a unified ledger combining tokenised central bank money, commercial bank deposits, and assets on a shared programmable platform.

The BIS described money and assets as ‘executable objects’ whose settlement could be made conditional on centrally defined criteria, noting that programmability could ‘enable arrangements that are currently not practicable, thereby expanding the universe of possible economic outcomes’. The programmable money rails and the allocation mechanism converge where the money itself becomes conditional.

The structural endgame of combining the proposals from this network is visible in the same 2016 document. Van Lerven’s guide assessed sovereign money creation — where the central bank is the sole creator of all money — alongside the perpetual securities mechanism, where money created by the BoE is made permanent through non-interest-bearing bonds that never mature and cannot be sold. Under current QE, bonds mature and the money can be withdrawn. Perpetual securities never mature. There is no buyer for a zero-coupon perpetual. The money cannot be withdrawn — not by the BoE, not by the Treasury, not by any market mechanism. Combine sovereign money (only the central bank creates money) with perpetual securities (the money created is permanent) and the allocation body (the EPCC directs where it goes), and the trajectory is one-directional: with each cycle, old commercial-bank-created money is retired as loans are repaid and replaced by centrally created permanent money directed by the coordination body.

Over time, the proportion of the economy funded by centrally allocated, irreversible money approaches the whole. The central bank doesn’t influence the economy. It progressively absorbs it.

The Green Layer

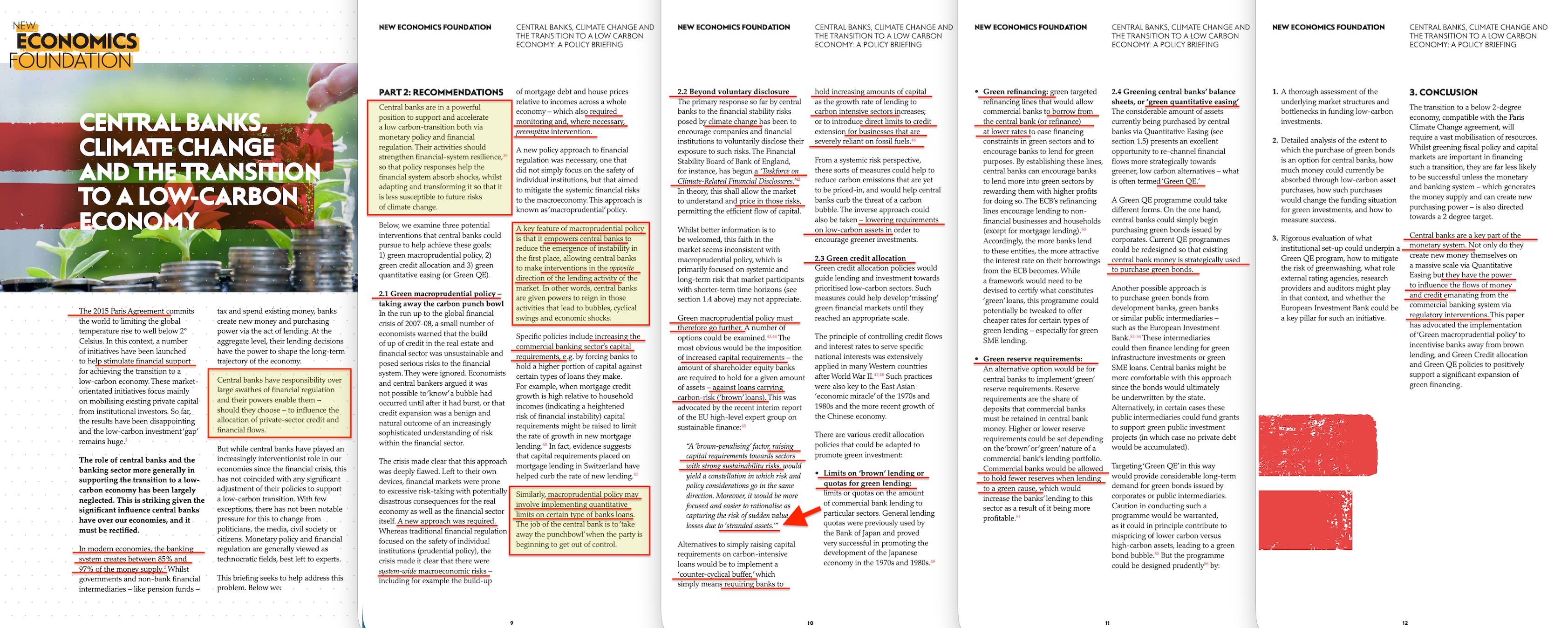

In 2017, van Lerven and Ryan-Collins wrote a NEF policy briefing called Central Banks, Climate Change and the Transition to a Low-Carbon Economy73. It proposed three interventions: green macroprudential policy (adjusting capital requirements to penalise carbon-intensive lending), green credit allocation (directing bank lending toward green sectors through quotas, refinancing lines, and reserve requirements), and greening central bank balance sheets (Green QE).

This was the 2013 mechanism with the green objective attached. Where the Monetary Allocation Committee had been proposed for economic rebalancing with ecological sustainability as one criterion among several, the 2017 briefing reorganised the same toolkit around a single purpose: aligning the monetary and banking system with the Paris Agreement.

The report cited Carney’s ‘Tragedy of the Horizon’ speech74, the TCFD, and the growing consensus among central bankers that climate risk was financial risk. But the domestic allocation mechanism it described was designed four years before any of those existed.

The Programme

Between 2017 and 2023, van Lerven published across every layer of UK central bank and coordination policy, building a complete programme from the mechanism and the objective.

The Positive Money report A Green Bank of England75 (2018), by Rob Macquarie, proposed reforming the MPC’s mandate to include environmental sustainability — the goals set by Parliament through the Chancellor’s remit. Van Lerven was acknowledged for ‘useful comments and feedback’. The report framed the changes as open political reforms to a public mandate, explicitly stating that goal-setting was ‘fundamentally a political question’.

By this point Ryan-Collins had moved from NEF to UCL’s Institute for Innovation and Public Purpose76 — the bridge between the think tank and the academic institute where the programme’s technical papers would be co-authored. Together at UCL IIPP, van Lerven and Ryan-Collins wrote Adjusting Banks’ Capital Requirements in Line with Sustainable Finance Objectives77 (2018) — the risk-weighting reform that would translate climate exposure into lending costs. With Bezemer, Ryan-Collins, and Zhang, van Lerven also co-authored Credit Where It’s Due78 (2018) — a historical review showing that directed credit guidance was standard practice in post-war France, Japan, South Korea, and across Western economies until the deregulation wave of the 1980s.

A third paper from the same year, Bringing the Helicopter to Ground79 (Ryan-Collins & van Lerven, UCL IIPP, 2018), reviewed the history of fiscal-monetary coordination itself — showing that the separation of fiscal and monetary policy into independent silos was the historical exception, not the rule, and that coordination between treasuries and central banks had been standard practice throughout the post-war period. This was the intellectual groundwork for the EPCC proposal that would follow five years later.

In January 2020, the Bank for International Settlements published The Green Swan: Central Banking and Financial Stability in the Age of Climate Change80. It introduced a distinction between green swans and black swans: climate-related financial crises were certain to occur, with only the timing uncertain. At the same time, it acknowledged ‘radical uncertainty’ about form and magnitude — certainty of occurrence combined with uncertainty of detail, creating the conditions for present-day regulatory action against future modelled risk.

The practical consequence of this machinery is already visible. IIASA — the International Institute for Applied Systems Analysis, founded in 1972 as an East-West systems-analysis bridge — officially hosts the NGFS Scenario Explorer81 and provides the transition scenarios through its Integrated Assessment Models82. The Potsdam Institute for Climate Impact Research provides the damage functions83. Together they form the academic consortium that produces the scenarios central banks use worldwide, funded by Bloomberg Philanthropies84 and the ClimateWorks Foundation85.

IIASA ‘black box’ modelling feeds into NGFS scenarios, which feed into central bank stress tests, which feed into Basel risk weights86, which determine how much capital a bank must hold against a given loan, and the capital requirement determines the cost of lending.

A house on a modelled flood plain becomes harder to mortgage — not because it has flooded, but because a scenario model designates it as at risk and the risk weight raises the bank’s cost of carrying the loan. A farm in a modelled water-stress zone becomes harder to insure. A business dependent on fossil fuel supply chains finds its line of credit repriced on the basis of modelled future impact, not present performance.

The formulas that already price every mortgage, car loan, and business overdraft in the country are being extended to include climate and ecosystem variables87. No legislation was required. The adjustment happens inside the capital adequacy framework, invisible to the borrower, largely unappealable.

In April 2019, the NGFS had already issued what amounted to an activation order: an open letter from Carney, Villeroy de Galhau, and NGFS Chair Frank Elderson88 stating that companies and industries that failed to adjust to the low-carbon transition ‘will fail to exist’89. Supervisors were instructed to integrate climate monitoring into ‘day-to-day supervisory work’.

In November 2020, NEF and Positive Money convened a joint open letter to the incoming Bank of England Governor90, signed by more than 125 economists, calling on the Bank to use its powers to address the climate crisis. Four months later, in March 2021, Chancellor Rishi Sunak — a Conservative — updated the remit letters for the MPC, the FPC, and the PRA to include environmental sustainability as a consideration91.

The mandate reform that the Positive Money 2018 report had called for was delivered by a Conservative Chancellor.

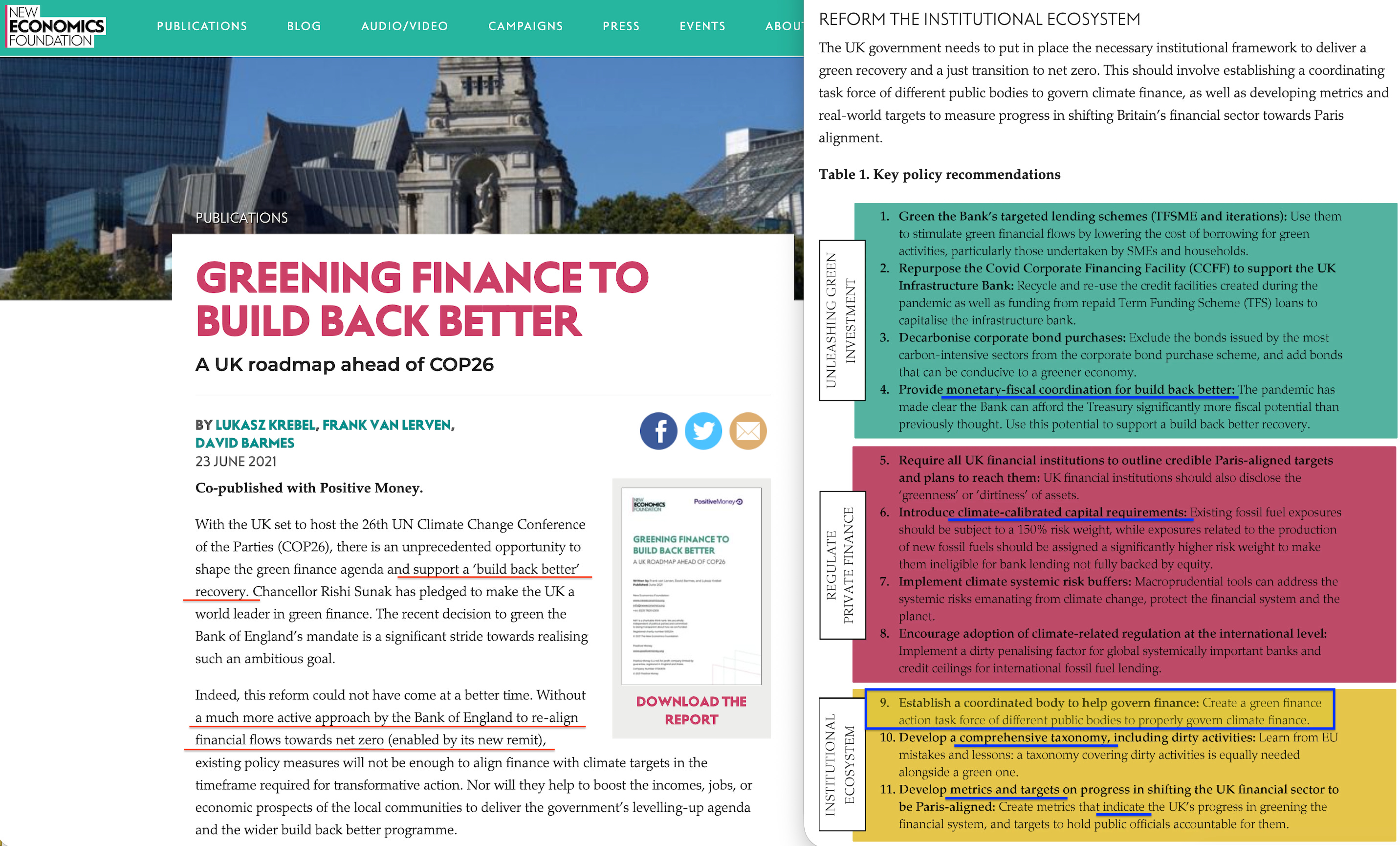

Against this backdrop, van Lerven’s programme kept building. In 2021, he lead-authored Greening Finance to Build Back Better92, a joint NEF and Positive Money report. Recommendation 9 proposed a Green Finance Action Taskforce — a standing body that’d monitor the green finance gap, coordinate policy across the Treasury, the Bank of England, and the financial regulators, run public consultations, and report to a parliamentary committee. The GFAT was the Monetary Allocation Committee under a new name, with a ‘green’ mandate and a specific institutional design. The report was funded by the Sunrise Project and the Laudes Foundation, and acknowledged a ‘Network for Greening the Bank of England’ alongside collaborators across NEF, Positive Money, UCL IIPP, and the Council on Economic Policies.

That same year, van Lerven co-authored Greening the Eurosystem Collateral Framework93 — specifying how to rewrite the ECB’s rules for accepting bonds as collateral. The collateral framework determines what the central bank accepts as backing when it lends to commercial banks, which in turn determines what flows through the financial system and what doesn’t.

The paper was funded by INSPIRE94 — the International Network for Sustainable Financial Policy Insights, Research and Exchange — a research network co-founded by the Grantham Research Institute at LSE95 (chaired by Nicholas Stern96) as the NGFS’s research stakeholder. INSPIRE connects the NGFS’s international scenario-setting to national policy implementation through funded academic research, and van Lerven’s paper sits at that junction.

By 2025, the ECB had acted on it97 — tilting corporate bond reinvestment toward issuers with stronger climate scores (announced July 202298) and adjusting collateral haircuts along climate criteria (implemented July 202599), directly implementing the mechanism the paper had specified. The ECB’s own strategy review acknowledged it was ‘responding to pressure from civil society’100 — the foundation-funded civil society organisations whose recommendations it was adopting.

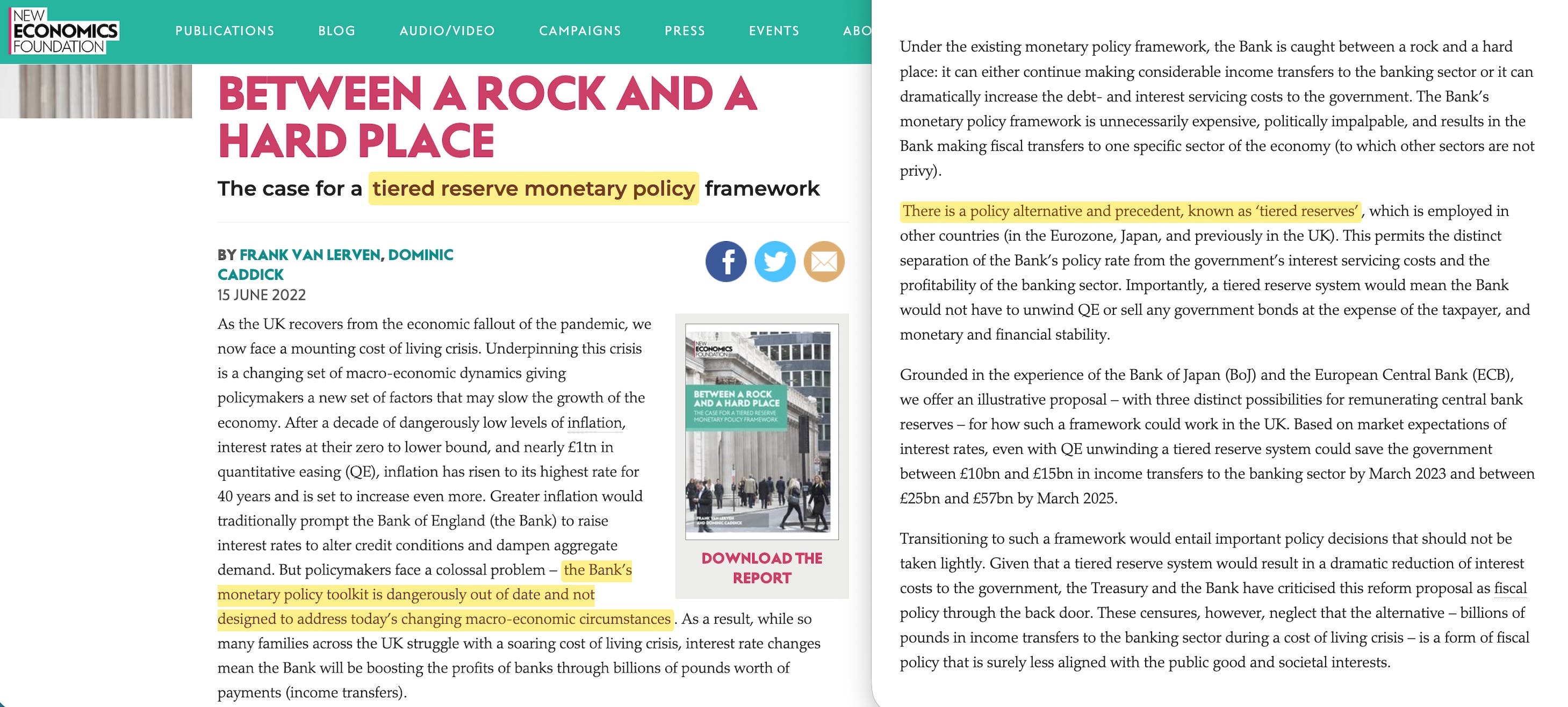

Van Lerven also co-authored Calling Time: Replacing the Fiscal Rules with Fiscal Referees101 in 2021 — proposing independent monitoring bodies to replace fixed fiscal rules. He published Green Credit Guidance102 in 2022, specifying the mechanism for translating a green mandate into interest rate differentials and lending conditions, and Between a Rock and a Hard Place103 the same year, on tiered reserve requirements — the structure of the monetary base itself.

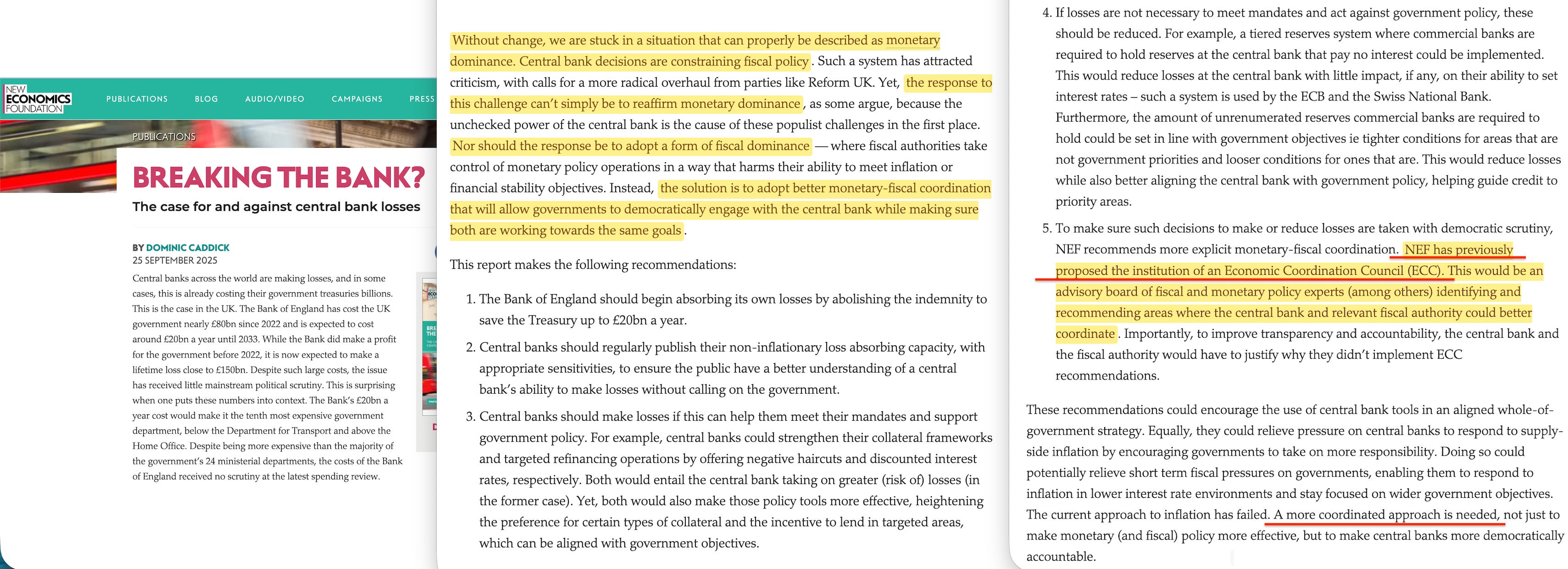

In November 2025, NEF published a briefing proposing that the Treasury renegotiate the Osborne-era indemnity under which it covers the Bank’s QE losses104 so that the Bank absorbs its own losses, as the Fed and ECB do105. The proposal frees £4.8 billion in fiscal headroom for the Chancellor while removing the Treasury’s financial leverage over the Bank, deepening the central bank’s operational independence.

The full NEF report, Breaking the Bank?106, frames the current system as ‘monetary dominance’ — the central bank’s decisions constraining fiscal policy — and prescribes ‘better monetary-fiscal coordination’ as the democratic cure. The coordination body it describes is the EPCC. The report diagnoses a real problem (the BoE’s losses genuinely constrain the Chancellor), then prescribes the advocacy network’s own architecture as the solution.

In October 2022, the Bank of England and the PRA hosted a Climate and Capital conference107 to discuss adjusting the capital framework for climate-related financial risk. Van Lerven spoke, arguing that ‘every part of the system’ needed to move ‘in the same direction’. Nick Robins — who co-invented the stranded assets concept two decades earlier — argued that misalignment with net zero was itself grounds for regulatory action108. Nicholas Stern delivered the welcome address109. Researchers from the Oxford Sustainable Finance Group (the current Smith School’s Stranded Assets Programme) presented. Pierre Monnin attended from the Council on Economic Policies110 — listed as a collaborator in van Lerven’s 2021 report alongside NEF, Positive Money, and UCL IIPP. HSBC, which had co-funded the original Smith School programme, sent its global head of stress testing.

The people who’d written the proposals, invented the concept, run the forums, and co-founded the research network were at the Bank of England discussing how to implement the policy the programme had specified four years earlier.

In Tandem

In 2023, van Lerven co-authored In Tandem: The Case for Coordinated Economic Policymaking111 through the Fabian Society with Michael Jacobs, Robert Calvert Jump, and Jo Michell. The report proposed an Economic Policy Coordination Committee — a standing trisectoral body with representatives from the Treasury, the Bank of England, the Climate Change Committee, the Office for Budget Responsibility, a proposed National Investment Bank, devolved governments, business associations, and trade unions.

The EPCC would meet twice yearly before the Budget, with ongoing official-level engagement, and would set the economic objectives for fiscal and monetary policy. It would use an asymmetric pressure mechanism — giving formal standing to growth, employment, inequality, and decarbonisation objectives alongside existing inflation and fiscal targets — plus statutory pre-budget footing, meaning the government would have to respond formally to the EPCC’s recommendations before setting fiscal policy.

The proposal’s formal accountability structures — published minutes, parliamentary reporting — are presented as democratic safeguards. In practice, they’re a dilution of authority: under the current system, the Chancellor writes the remit letter alone. Under the EPCC, that authority’s shared with a trisectoral body whose composition and mandate were designed by the advocacy network that proposed it. The democratically elected Chancellor goes from sole author of the Bank’s objectives to one voice at a table specified by the people who built it. The Fabian report states that the meetings should be placed on ‘a statutory footing, so they could not be bypassed by the government of the day without new legislation’ — meaning a future Chancellor who wanted to govern alone would need an Act of Parliament to stop attending. The Kwarteng episode, documented below, shows what happens when a Chancellor tries to govern outside this consensus.

The EPCC is the Monetary Allocation Committee a decade later — and the answer to the second of van Lerven’s two questions. The MPC determines the quantity; the EPCC determines the allocation. The scope expanded from QE allocation to full fiscal-monetary coordination, and the design evolved from a committee accountable to Treasury into a standing body with statutory standing. But the structural position — sitting between deciding what the money is for and the actual money creation — hasn’t changed since 2013. And as the documented sequence shows, the objectives the EPCC would prescribe don’t come from the elected government. They come from the foundation-funded advocacy network — through open letters, policy reports, forum recommendations, and INSPIRE-funded research — and the EPCC feeds them into the money creation process.

The 2021 Greening Finance to Build Back Better112 report (covered above) links the two proposals. Van Lerven lead-authored it, proposing the GFAT — structurally identical to the EPCC — two years before the Fabian report gave it statutory standing under a new name. One author connects the monetary creation reform (Positive Money, 2018), the integrated green finance programme with its coordination body (NEF/PM, 2021), and the formal fiscal-monetary coordination proposal (Fabians, 2023).

The 2024 election returned a Labour government — the Fabian Society’s natural partner — but the EPCC hasn’t yet been adopted in its statutory form. Its coordination functions are slowly being absorbed by existing bodies: the OBR, the Climate Change Committee113, and the National Wealth Fund114.

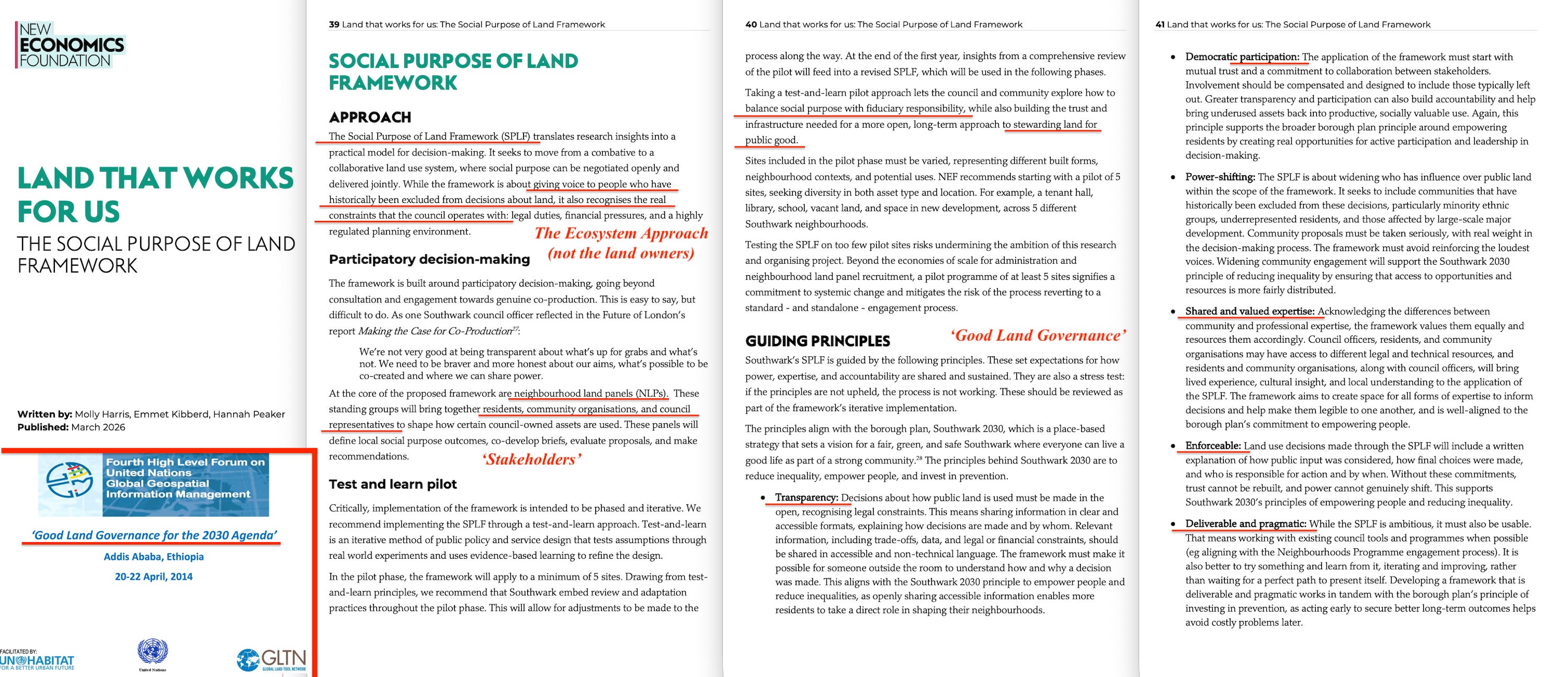

What has arrived is the other side of the architecture. Late in 2025, HM Treasury published recommendations from the Social Impact Investment Advisory Group to create a permanent Office for the Impact Economy115 inside Whitehall — a director-led hub embedding the blended finance model across every department, procurement decision, and local authority. The settlement side got its Whitehall office before the allocation side did. In March 2026, NEF published its ‘Social Purpose of Land Framework’116 — Neighbourhood Land Panels directing how public land is used, phased from pilot sites to universal application, drawing on the Convention on Biological Diversity’s Ecosystem Approach117 and the UN-Habitat ‘Good Land Governance’ framework118, and using the same trisectoral participatory model the EPCC applies to monetary policy. The same institution runs the same governance architecture across money and land.

Meanwhile, NEF and Positive Money Europe have proposed the same coordination body at the European level — an ‘Economic Coordination Council’ — using the same argument119: that monetary-fiscal separation constitutes ‘monetary dominance’, and that the democratic alternative is the coordination architecture the advocacy network designed.

The Monetary Allocation Committee (2013), the GFAT (2021), the EPCC (2023), and the ECC are the same body under four names, scaling from UK domestic to continental.

What Happened Next

The architecture had already shown it could enforce before the voluntary layer collapsed.

On 23 September 2022, Chancellor Kwasi Kwarteng announced £45 billion in unfunded tax cuts120. Within six weeks, both he and Liz Truss were gone121. The story at the time was that reckless fiscal policy caused a market panic. What actually triggered it was a pre-existing vulnerability in the pension system: roughly £1.5 trillion in Liability-Driven Investment positions, built up over a decade of near-zero interest rates, where pension funds used gilts as collateral to borrow money to buy more gilts. When Kwarteng’s announcement moved gilt yields sharply, the margin calls cascaded.

The Bank of England — directly responsible for this kind of systemic risk since the Prudential Regulation Authority was created in 2013122 — had watched the £1.5 trillion LDI vulnerability build for a decade without acting. When Kwarteng’s announcement triggered the cascade, the Bank refused to call an emergency rate meeting, the standard tool for a financial crisis, while its own announced gilt-selling programme was pushing prices further down. It intervened on 28 September only when pension funds were hours from collapse, spent £65 billion on the rescue — more than the tax cuts it was supposedly responding to — and set a hard deadline that left the Prime Minister no room to move.

The political consequence was removing a government that had tried to govern outside the institutional consensus.

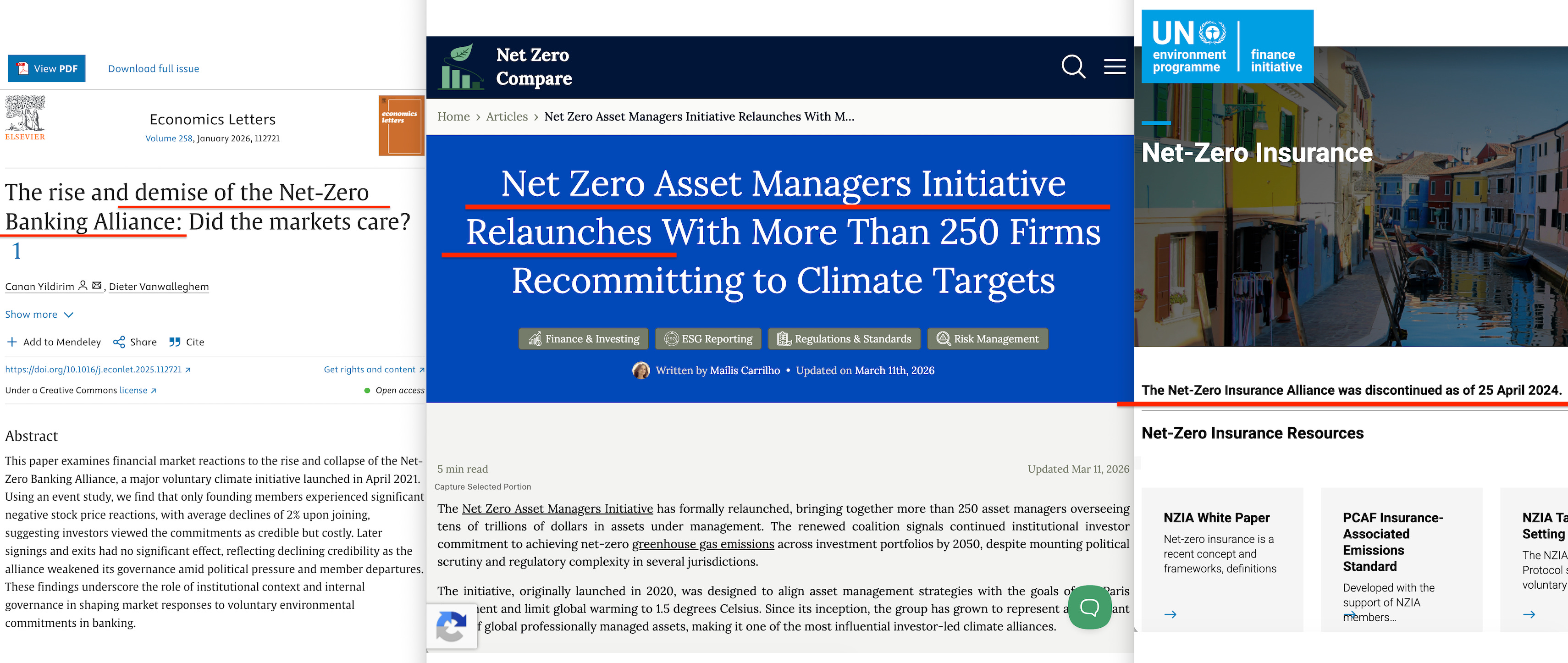

In 2025, the voluntary layer collapsed123. The Net-Zero Banking Alliance shut down124, the Net Zero Asset Managers initiative relaunched without its 2050 commitment125, and the Net-Zero Insurance Alliance had already been discontinued126. US institutions withdrew from climate finance coalitions under political pressure and sustainable fund flows reversed127.

Read through declarations, the architecture was in retreat. But the function had simply moved elsewhere. The voluntary alliances had never propped up the mandatory regimes: the EU’s Corporate Sustainability Reporting Directive128 remained in force with phase-in adjustments, and the ISSB standards were adopted or being adopted across more than twenty jurisdictions representing a majority of global GDP129.

The voluntary ESG wrapper was shed because the regulatory infrastructure underneath it had already hardened into law — the CSRD and CBAM in Europe, the ISSB standards across twenty-plus jurisdictions, Basel requirements worldwide.

The most striking example was monetary. The United States passed the Anti-CBDC Surveillance State Act130, banning a public central bank digital currency. The same legislative session passed the GENIUS Act131, establishing federal oversight of private stablecoins — with freeze and seizure capacity, supervisory authority, and programmable compliance requirements with features similar to a public CBDC’s. The ban only applied to the label. The capability — programmable, surveillable, supervisable digital settlement — simply moved to private rails.

The sovereign money architecture that van Lerven specified in 2016 arrived under a different name in the United States.

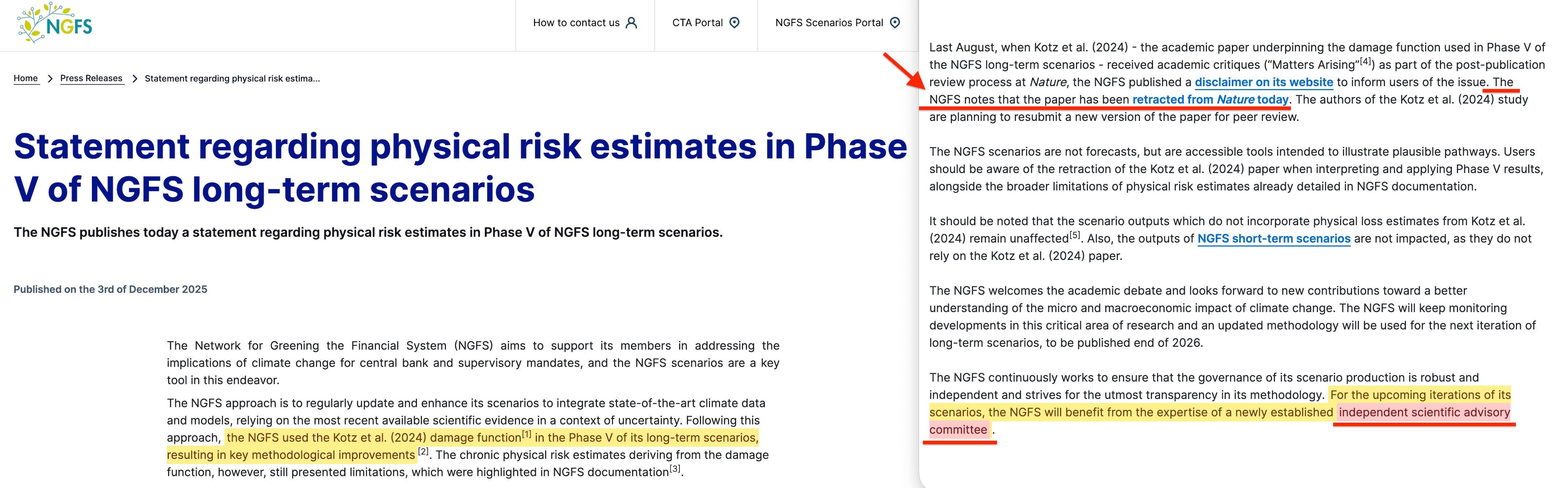

In December 2025, Nature retracted the study by Maximilian Kotz and colleagues at the Potsdam Institute for Climate Impact Research that underpinned the NGFS Phase V climate scenarios132. The paper projected that climate change would reduce global income by nineteen per cent by 2050, a figure the NGFS translated into scenario ranges of seven to fifteen per cent GDP loss. Banks and regulators across the world had already built these figures into their stress tests and capital requirement calculations. The retraction notice stated the results were ‘found to be sensitive to the removal of one country, Uzbekistan, where inaccuracies were noted in the underlying economic data for the period 1995–1999’. Uzbekistan’s GDP in the dataset showed a ninety per cent drop with no relation to World Bank figures. The error was caught not by internal review but by external auditors.

The NGFS announced a new ‘independent scientific advisory committee’ to oversee future scenario production133. The scenarios kept operating with disclaimers attached. No institution accepted responsibility or changed the capital requirements that were set using retracted figures.

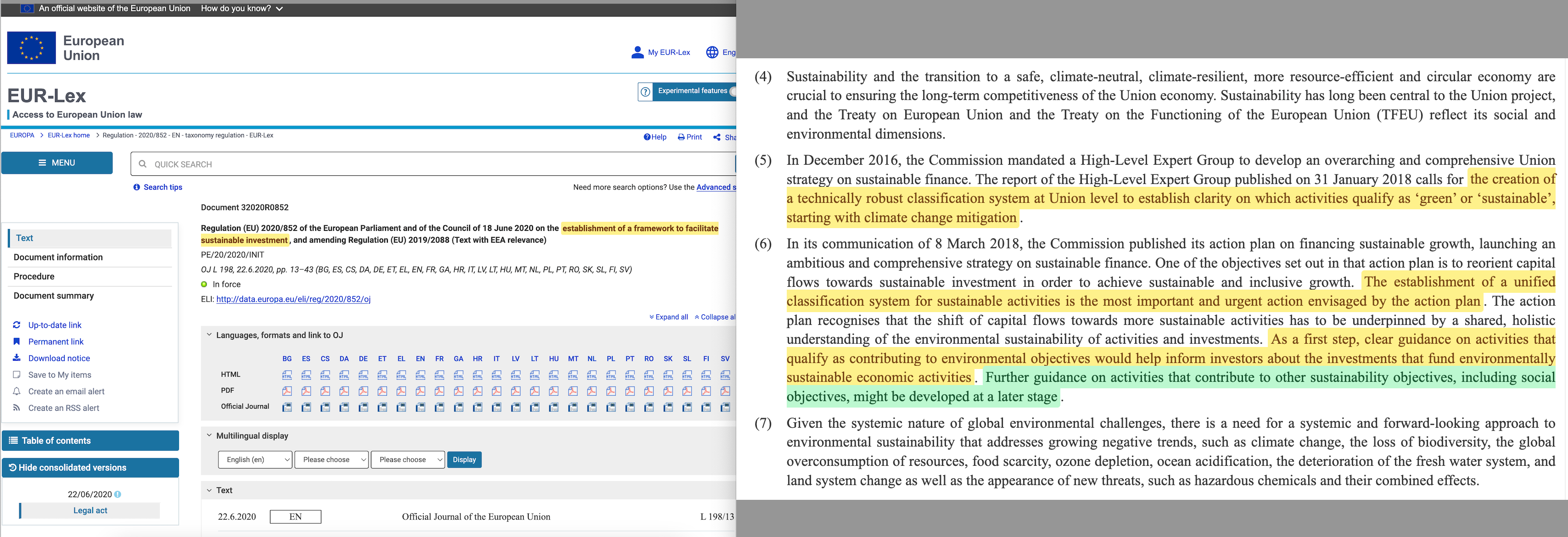

The EU Taxonomy Regulation’s Article 26134 notes that further guidance on activities contributing to ‘other sustainability objectives, including social objectives’, may come later. That expansion is already under way. The HM Treasury-commissioned Dasgupta Review on the Economics of Biodiversity135 (February 2021) called for natural capital to be priced into economic decisions through ‘inclusive wealth’ accounting.

In September 2023, the Taskforce on Nature-related Financial Disclosures136 launched recommendations modelled directly on the TCFD structure137 — governance, strategy, risk management, metrics — extending the disclosure architecture from carbon to biodiversity. In April 2025, the PRA updated its supervisory statement SS3/19 to require mortgage lenders to scrutinise physical climate risks138 — flooding, subsidence, coastal erosion — in their real estate portfolios, making mortgage repricing on modelled risk a live supervisory requirement.

The infrastructure built for climate works for expansion beyond climate too.

The mechanism that prices carbon risk into a mortgage can price biodiversity risk, water-stress risk, social-impact risk, or any other variable that a future scenario model designates as material.

What the Timeline Shows

The complete sequence runs:

2007: Rockefeller Bellagio Center — ‘impact investing’ coined139

2008: Green New Deal group report (NEF/Hines) — the concept140

2009: GIIN launched at Clinton Global Initiative — impact investing framework141

2010: Green QE (Murphy & Hines) — the money creation mechanism142

2011: Where Does Money Come From? (Ryan-Collins et al., NEF) — the theoretical base143

2011: Carbon Tracker Unburnable Carbon (Campanale) — the stranded assets thesis144

2011: Gore & Blood Manifesto for Sustainable Capitalism (WSJ) — the public specification145

2012: Big Society Capital launched (Cameron government) — UK social investment wholesaler146

2012: Epstein approaches Bendell147; IFLAS founded at University of Cumbria — currency innovation network148

2013: Strategic QE and the Monetary Allocation Committee (Ryan-Collins, NEF) — the allocation body149

2014: Conference on Inclusive Capitalism (Mansion House / E.L. Rothschild) — Carney, Lagarde, Clinton150

2014–2018: Waddesdon forums (Smith School / Rothschild Foundation) — the enforcement architecture151

2014: Smith School Financial Dynamics of the Environment — three-channel climate risk framework152

2015: Carney ‘Tragedy of the Horizon’ speech — central bank acknowledgement153154

2015: TCFD launched — the disclosure framework155

2016: A Guide to Public Money Creation (van Lerven, Positive Money) — the unified specification156

2016: Full reserve banking defence (Dyson, Hodgson & van Lerven, CJE) — the CBDC theoretical base157

2017: NGFS launched — the central bank network158

2017: Green central banking briefing (van Lerven & Ryan-Collins, NEF) — green conditionality attached159

2018: A Green Bank of England (Positive Money; van Lerven acknowledged) — mandate reform160

2018: Capital requirements reform (van Lerven & Ryan-Collins, UCL IIPP) — risk weighting161

2018: Bringing the Helicopter to Ground (Ryan-Collins & van Lerven, UCL IIPP) — fiscal-monetary coordination precedent162

2019: NGFS open letter — ‘will fail to exist’163

2020: BIS The Green Swan — certain occurrence, radical uncertainty164

2020: Council for Inclusive Capitalism with the Vatican launched — papal authority added165

2020: Joint NEF/PM open letter — 125+ economists call for green BoE166

2021: Sunak remit update — Conservative Chancellor adds environmental sustainability to MPC/FPC/PRA remits167

2021: ISSB created at COP26 — TCFD consolidated into global mandatory disclosure baseline168

2021: Dasgupta Review (HM Treasury) — natural capital priced into economic decision-making169

2021: Greening Finance to Build Back Better (van Lerven, NEF/PM) — the GFAT170

2021: Eurosystem collateral framework (van Lerven et al., INSPIRE-funded) — ECB clearing reform171

2022: Green credit guidance (van Lerven, NEF) — the compilation mechanism172

2022: BoE Climate and Capital conference — the programme’s authors at the Bank discussing implementation173

2022: ECB announces climate-tilted corporate bond reinvestment — van Lerven’s collateral paper begins implementation174

2022: Kwarteng mini-budget and Truss removal — the architecture enforces175

2023: In Tandem and the EPCC (van Lerven et al., Fabian Society) — statutory coordination body176

2023: BIS unified ledger blueprint — programmable settlement infrastructure specified177

2023: TNFD recommendations launched — biodiversity disclosure modelled on TCFD178

2025: Net-zero alliance collapses — voluntary layer shed, mandatory layer continues179

2025: GENIUS Act — public CBDC prohibited, private programmable settlement authorised180

2025: PRA SS3/19 update — mortgage lenders required to scrutinise physical climate risks181

2025: Office for the Impact Economy recommended — blended finance formally embedded in Whitehall182

2025: Kotz retraction — NGFS scenario foundation retracted, scenarios continue operating183

The allocation mechanism was proposed before the policy objective was attached. The domestic coordination body was designed before the international enforcement architecture was publicly specified. The monetary architecture specification preceded the green conditionality layer, which preceded the formal coordination proposal. Every step was published openly, with authors and funders named.

One institutional network — centred on NEF and extending through Positive Money, UCL IIPP, INSPIRE, the Fabian Society, and the Grantham Research Institute — produced a complete monetary governance programme over fifteen years. NEF’s reach extends beyond the domestic: in November 2025, it co-authored an assessment of the G20’s international financial architecture with think tanks across four continents, funded by the Ford Foundation and the Open Society Foundations, applying the same ‘economic justice’ framework at the global level184.

A parallel network — centred on the Smith School, the Generation Foundation, the Rothschild Foundation, and the Financial Stability Board — built the international enforcement infrastructure during the same period. They overlap through documented institutional relationships: INSPIRE connects the Grantham Institute to the NGFS; van Lerven’s INSPIRE-funded research connects the international scenario framework to national policy proposals; Ryan-Collins connects NEF to UCL IIPP; and the same personnel recur across both networks.

The investment side of the architecture — impact investing, blended finance, social investment — was built simultaneously by a third overlapping network, running from the Rockefeller Foundation’s SDG programmes through the Global Impact Economy Forum to Cameron’s Big Society and its successors. Impact investing supplies the purpose, stranded assets supply the enforcement, and blended finance supplies the settlement mechanism. Each label changed with each government and jurisdiction while the underlying arrangement remained the same.

The documents don’t settle whether this is a coordinated programme. Then again, such a link, if located, would be devastating to the institutions it connected. What they do establish beyond dispute is that the complete architecture — the monetary base, the allocation mechanism, the green conditionality, the coordination body, the enforcement framework, the programmable settlement infrastructure, and the connections between them — was specified in public by a traceable and overlapping network of authors before the regulatory infrastructure it now connects to was built.

The mechanism came before the objective, the allocation body before the enforcement architecture, and the financial infrastructure before the treaties it claims to implement.

None of this depends on motives. The architecture works the same way whether its builders are idealists responding to a legitimate crisis or engineers building a control system. The structural concern — that a content-agnostic allocation mechanism, once built, accepts whatever objective is supplied to it, by whoever controls the supply — is the same either way.

The conditional infrastructure itself isn’t new. The Financial Action Task Force has attached KYC requirements, transaction monitoring, suspicious activity reporting, greylisting of non-compliant jurisdictions to money since 1989185. Every bank in the international system already operates under this framework. What the programme above adds isn’t the mechanism of conditionality but the expansion of its criteria — from money laundering to carbon, from criminal compliance to climate compliance, using the same rails.

And the programme’s end point, stated plainly, is the centralisation of credit in the hands of an operationally independent central bank — allocated by a coordination body, conditioned on compliance with objectives originated by a foundation-funded advocacy network, settled on programmable rails, and withdrawn from anything a scenario model designates as non-compliant. The elected government’s role is to transmit those objectives through remit letters it didn’t draft.

Money is unconditional — you hold it, you spend it, no one asks why. Credit is conditional, extended by an authority, subject to criteria, revocable. Attach conditions to money and it becomes credit, however it’s branded. The authors of the Communist Manifesto listed the centralisation of credit through a national bank with an exclusive monopoly as their fifth plank in 1848 — but they at least envisioned the state directing it. The documented programme places the direction with unelected institutions and the state beneath them. The delivery mechanism isn’t revolution but remit letters, not expropriation but risk weights, not seizure of the means of production but gradual administrative capture of the means of exchange.

The programme consequently produces two unelected committees: the Monetary Allocation Committee directs where centrally created money flows, and the NGFS Scientific Advisory Committee determines what the scenario models designate as non-compliant — together controlling both the allocation and the withdrawal, with the elected government holding neither pen.

The ethical justification gradually changes. Presently, it’s the Sustainable Development Goals, but soon, that ethic will migrate at a foundation-funded convening outside public limelight.

The destination — conditional money, administered by unelected institutions — won’t.

My heaven sir/madam, do you sleep? Your work is superior. The details is astonishing. Thank you.

This says it all:

"economics 𝗮𝘀 𝗶𝗳 people and the planet mattered".